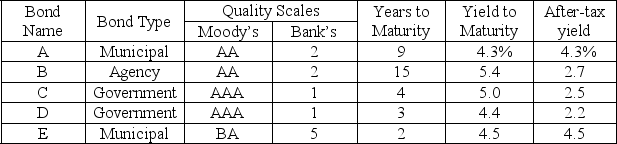

A portfolio manager in charge of a bank portfolio has $10 million to invest. The securities available for purchase, as well as their respective quality ratings, maturities, and yields, are shown in the table below:

The bank places the following policy limitations on the portfolio manager's actions:

The bank places the following policy limitations on the portfolio manager's actions:

1. Government and agency bonds must total at least $4 million.

2. The average quality of the portfolio cannot exceed 1.4 on the bank's quality scale. (Note that a low number on this scale means a high-quality bond.)

"3. The average years to maturity of the portfolio must not exceed 5 years.

Assuming that the objective of the portfolio manager is to maximize after-tax earnings and that the tax rate is 50%, formulate a linear program that can be used to determine how much money to invest in each type of bond."

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q91: Describe guidelines for spreadsheet model development.

Q93: A constraint in Excel Solver consists of

Q104: When is a Linear Program unbounded?

Q107: The Village Butcher Shop traditionally makes its

Q114: Formulate the following as a linear program.

Joe's

Q117: A caterer must prepare from five fruit

Q118: Car Phones, Inc. (CP), sells two models

Q127: Solver's Changing Cells corresponds to the _

Q129: In Solver, the _ is the cell

Q130: It is good practice to _ the

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents