Essay

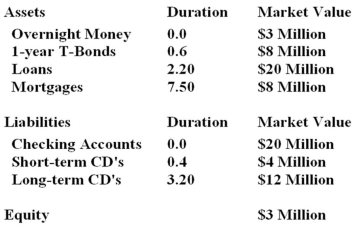

What new asset duration will immunize the balance sheet?

What new asset duration will immunize the balance sheet?

Correct Answer:

Verified

Given DL = 1.111,then...

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Related Questions

Q56: You have taken a short position in

Q57: Suppose you agree to purchase one ounce

Q58: You bought a futures contract for $2.60

Q59: If a firm sells a floor at

Q60: A mortgage banker had made loan commitments

Q61: The futures markets are labeled as pure

Q62: A bank has a $100 million mortgage

Q63: Duration is defined as the weighted average

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents