Use the following information to answer the question(s) below.

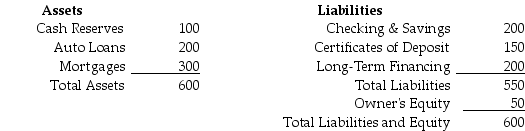

You are a risk manager for Security First Trust Savings and Loan (SFTSL) .SFTSL's balance sheet is as follows (in millions of dollars) :  The duration of the auto loans is three years and the duration of the mortgages is eight years.Both cash reserves and checking and savings have zero duration.The CDs have a duration of two years and the long-term financing has a ten-year duration.

The duration of the auto loans is three years and the duration of the mortgages is eight years.Both cash reserves and checking and savings have zero duration.The CDs have a duration of two years and the long-term financing has a ten-year duration.

-If interest rates are currently 5%,but fall to 4%,your estimate of the approximate change in SFTSL equity is closest to:

A) 8% decrease.

B) 12% decrease.

C) 8% increase.

D) 14% increase.

Correct Answer:

Verified

Q43: Which of the following statements is FALSE?

A)Interest

Q44: In December 2005,the spot exchange rate for

Q45: Luther Industries needs to borrow $50 million

Q46: The duration of a five-year bond with

Q47: Which of the following statements is FALSE?

A)As

Q48: What is the duration of a five-year

Q49: Which of the following statements is FALSE?

A)Corporations

Q50: Use the following information to answer the

Q51: The Century 22 fund has invested in

Q52: Which of the following statements is FALSE?

A)We

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents