(Requires Appendix material)Your textbook states that in "the distributed lag regression model,the error term ut can be correlated with its lagged values.This autocorrelation arises,because,in time series data,the omitted factors that comprise ut can themselves be serially correlated."

(a)Give an example what the authors have in mind.

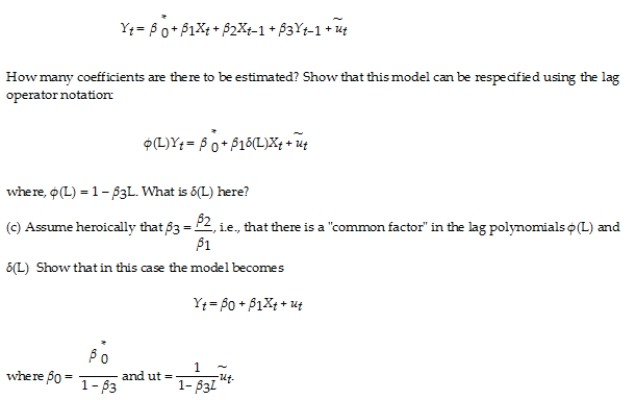

(b)Consider the ADL model,where the X's are strictly exogenous,and there is no autocorrelation (and/or heteroskedasticity)in the error term.  (d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

(d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q23: In time series data, it is useful

Q25: Money supply is linked to the monetary

Q37: The distributed lag model assumptions include all

Q38: When Xt is strictly exogenous,the following estimator(s)of

Q38: Your textbook presents as an example of

Q42: It has been argued that Canada's aggregate

Q43: The distributed lag model relating orange juice

Q44: You are hired to forecast the unemployment

Q45: There is some economic research which suggests

Q46: The distributed lag regression model requires estimation

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents