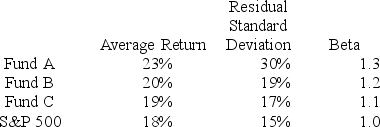

You want to evaluate three mutual funds using the Sharpe measure for performance evaluation. The risk-free return during the sample period is 5%. The average returns, standard deviations, and betas for the three funds are given below, as are the data for the S&P 500 Index.

The investment with the highest Sharpe measure is

A) Fund A.

B) Fund B.

C) Fund C.

D) the index.

E) Funds A and C (tied for highest) .

Correct Answer:

Verified

Q1: Morningstar's RAR methodI) is one of the

Q4: Hedge funds I) are appropriate as a

Q9: Suppose the risk-free return is 3%. The

Q11: Suppose two portfolios have the same average

Q18: Suppose two portfolios have the same average

Q21: Suppose a particular investment earns an arithmetic

Q24: The following data are available relating to

Q25: The following data are available relating to

Q25: Suppose you purchase one share of the

Q38: Suppose you purchase one share of the

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents