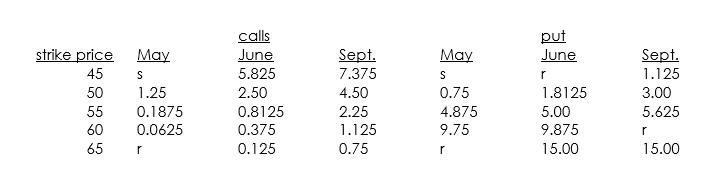

You have just learned through the grapevine that Pfizer (currently at $50.625 per share)may be a takeover candidate at $65 per share.You would like to speculate on the rumor,but you are worried that the stock will drop significantly if the rumor is false.Therefore,you have decided to use options to exploit this information.You are given the following option data for today,May 15th:

calls puts

a. Set up an option position that will best exploit the information you have, assuming that the takeover will happen by September 16 (the expiration day of the September options).

b. Assume now that the annualized standard deviation of Pfizer's stock price is 0.40 and that the six-month T-bill rate is 6%. Furthermore, assume that Pfizer pays a quarterly dividend of 50 cents and that the dividends are paid in April, July, October and January. What would your Black-Scholes estimates be for the options in the position that you have described in part a?

c. If the beta of Pfizer stock is 1.0, what is the beta of the position that you have set up in part a?

d. What are the deltas of the options that you have chosen for your position?

Correct Answer:

Verified

The investor wants to participate on ...

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q79: Assume bond returns are given by a

Q80: Consider the following spot rates: i01 =

Q81: Leland,O'Brien and Rubinstein (who invented portfolio insurance)came

Q82: Consider the following data for a stock

Q83: Assume that it is now December 2002.You

Q85: Assume that one can purchase gold bars

Q86: You are a portfolio manager who has

Q87: You are convinced that the next three

Q88: Consider a portfolio consisting of long positions

Q89: Suppose you are holding the following portfolio:

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents