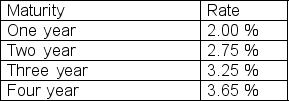

Find the one-year forward rate for year three given the following zero coupon rates:

A) 3.51%

B) 4.26%

C) 4.86%

D) 4.56%

Correct Answer:

Verified

Q27: A "fixed for floating" interest rate swap

Q38: Which of the following refers to the

Q39: Q41: Company JH enters a swap to pay Q42: In order to estimate the forward rate Q44: Find the forward price for one forward Q46: Ronald's company enters a 3-year, $10,000 plain Q48: What are the differences between forwards and Q54: Explain how derivatives led to the worst Q55: Nanci enters into a long position in![]()

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents