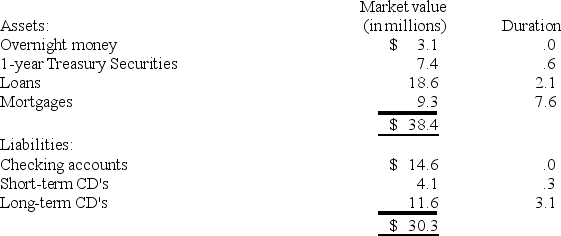

You have gathered the following market value and duration information on the Eastern Bank:  Calculate the duration of the bank's assets and of its liabilities.

Calculate the duration of the bank's assets and of its liabilities.

A) 2.86 years; 1.23 years

B) 2.97 years; 1.06 years

C) 2.86 years; 1.06 years

D) 2.48 years; 1.06 years

E) 2.97 years; 1.23 years

Correct Answer:

Verified

Q44: Calculate the duration of a $1,000 face

Q45: Which one of the following is true

Q46: Assume the futures contracts on silver are

Q47: Assume you write a futures contract on

Q48: Last week,you sold a futures contract on

Q50: Today,you purchased two natural gas futures contracts

Q51: Assume a futures contract on gold is

Q52: There are always at least _ counterparties

Q53: Credit default swaps are most like:

A)inverse floaters.

B)call

Q54: Today,you purchased a futures contract obligating you

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents