Multiple Choice

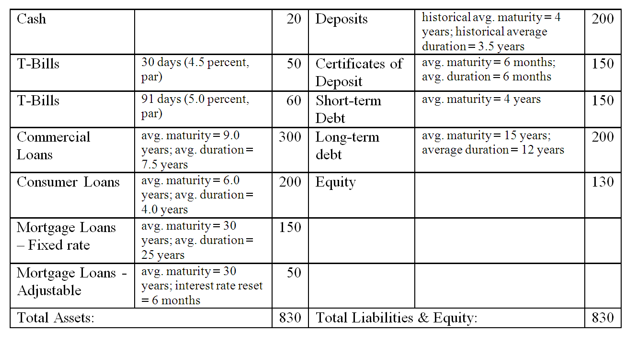

-What is this bank's interest rate risk exposure, if any?

A) The bank is exposed to decreasing interest rates because it has a negative duration gap of -0.21 years.

B) The bank is exposed to increasing interest rates because it has a negative duration gap of -0.21 years.

C) The bank is exposed to increasing interest rates because it has a positive duration gap of +0.21 years.

D) The bank is exposed to decreasing interest rates because it has a positive duration gap of +0.21 years.

E) The bank is not exposed to interest rate changes since it is running a matched book.

Correct Answer:

Verified

Related Questions

Q67: Immunization of a portfolio implies that changes

Q79: $1,000 face value, 9% annual coupon,