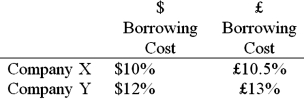

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow £5,000,000 fixed for 5 years. The exchange rate is $2 = £1 and is not expected to change over the next 5 years. Their external borrowing opportunities are:  A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap. In order for X and Y to be interested, they can face no exchange rate risk

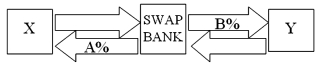

A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap. In order for X and Y to be interested, they can face no exchange rate risk  What must the values of A and B in the graph shown above be in order for the swap to be of interest to firms X and Y?

What must the values of A and B in the graph shown above be in order for the swap to be of interest to firms X and Y?

A) A = $10.50%; B = £12%.

B) A = $10%; B = £13%.

C) A = $12%; B = £13%.

D) A = £10.50%; B = $12%.

Correct Answer:

Verified

Q29: Swaps are said to offer market completeness

A)This

Q30: In the problem just previous, company X

A)is

Q31: Compute the payments due in the second

Q32: Company X wants to borrow $10,000,000 floating

Q33: When an interest-only swap is established on

Q35: Suppose ABC Investment Banker Ltd., is quoting

Q36: Company X wants to borrow $10,000,000 for

Q37: Floating for floating currency swaps

A)the reference rates

Q38: Company X wants to borrow $10,000,000 floating

Q39: Pricing a currency swap after inception involves

A)finding

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents