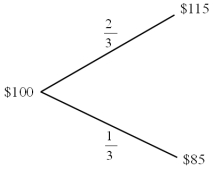

Find the value of a call option written on €100 with a strike price of $1.00 = €1.00.In one period there are two possibilities: the exchange rate will move up by 15% or down by 15% .The U.S.risk-free rate is 5% over the period.The risk-neutral probability of dollar depreciation is 2/3 and the risk-neutral probability of the dollar strengthening is 1/3.

A) $9.5238

B) $0.0952

C) $0

D) $3.1746

Correct Answer:

Verified

Q23: A European option is different from an

Q27: The volume of OTC currency options trading

Q29: Most exchange traded currency options

A)mature every month,with

Q33: The current spot exchange rate is $1.55

Q38: From the perspective of the writer of

Q42: For an American call option,A and B

Q44: Draw the tree for a call option

Q46: Find the hedge ratio for a call

Q46: Draw the tree for a put option

Q53: Use the binomial option pricing model to

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents