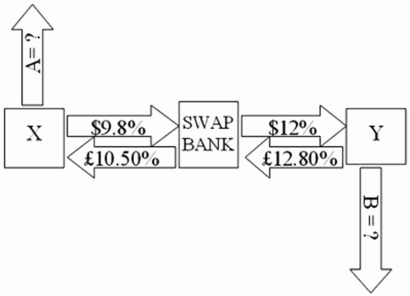

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow £5,000,000 fixed for 5 years.The exchange rate is $2 = £1 and is not expected to change over the next 5 years.Their external borrowing opportunities are: A swap bank proposes the following interest-only swap: Company X will pay the swap bank annual payments on $10,000,000 at an interest rate of $9.80 percent; in exchange the swap bank will pay to company X interest payments on £5,000,000 at a fixed rate of 10.5 percent.Y will pay the swap bank interest payments on £5,000,000 at a fixed rate of 12.80 percent and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of 12 percent.  If company X takes on the swap,what external actions should they engage in?

If company X takes on the swap,what external actions should they engage in?

A) They should borrow $10,000,000 at $10 percent.

B) They should borrow £5,000,000 at 10.50 percent interest-only for five years; translate pounds to dollars at the spot rate.

C) They should borrow £5,000,000 at £10.50 percent interest-only for five years; translate pounds to dollars at the spot rate; enter long position in a forward contract to buy £5,000,000 in five years.

D) none of the options

Correct Answer:

Verified

Q20: In the swap market,which position potentially carries

Q21: Company X wants to borrow $10,000,000

Q22: Company X wants to borrow $10,000,000

Q23: Pricing a currency swap after inception involves

A)finding

Q24: Consider the dollar- and euro-based borrowing

Q26: In a currency swap,

A)it may be the

Q27: Compute the payments due in the

Q28: Swaps are said to offer market completeness.

A)This

Q29: Company X wants to borrow $10,000,000

Q30: Floating-for-floating currency swaps

A)have different reference rates for

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents