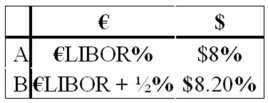

Come up with a swap (principal + interest)for two parties A and B who have the following borrowing opportunities.  The current exchange rate is $1.60 = €1.00.Company "A" wishes to borrow $1,000,000 for 5 years and "B" wants to borrow €625,000 for 5 years.You are a swap dealer.Quote A and B a swap that makes money for all parties and eliminates exchange rate risk for both A and B.Firms A and B are more concerned with what currency that they borrow in than whether the debt is fixed or floating.

The current exchange rate is $1.60 = €1.00.Company "A" wishes to borrow $1,000,000 for 5 years and "B" wants to borrow €625,000 for 5 years.You are a swap dealer.Quote A and B a swap that makes money for all parties and eliminates exchange rate risk for both A and B.Firms A and B are more concerned with what currency that they borrow in than whether the debt is fixed or floating.

Correct Answer:

Verified

Q64: Act as a swap bank and quote

Q66: Devise a direct swap for A and

Q67: What are the IRP 1-year and 2-year

Q68: With regard to a swap bank acting

Q70: Explain how this opportunity affects which swap

Q72: What would be the interest rate?

Q72: What would be the interest rate?

Q72: Suppose that you are a swap bank

Q73: Suppose that you are a swap bank

Q75: Explain how firm A could use the

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents