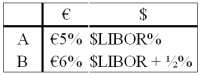

Come up with a swap (exchange of interest and principal)for parties A and B who have the following borrowing opportunities.  The current exchange rate is $1.60 = €1.00.Company "A" is in Milan,Italy and wishes to borrow $1,000,000 at a floating rate for 5 years and company "B" is a U.S.firm that wants to borrow €625,000 for 5 years at a fixed rate of interest.You are a swap dealer.Quote A and B a swap that makes money for all parties and eliminates exchange rate risk for both A and B.

The current exchange rate is $1.60 = €1.00.Company "A" is in Milan,Italy and wishes to borrow $1,000,000 at a floating rate for 5 years and company "B" is a U.S.firm that wants to borrow €625,000 for 5 years at a fixed rate of interest.You are a swap dealer.Quote A and B a swap that makes money for all parties and eliminates exchange rate risk for both A and B.

Correct Answer:

Verified

Q70: Explain how this opportunity affects which swap

Q70: Explain how this opportunity affects which swap

Q73: Suppose that the swap that you proposed

Q75: Suppose that you are a swap bank

Q75: Explain how firm A could use the

Q77: Explain how this opportunity affects which swap

Q79: Show how your proposed swap would work

Q79: Show how your proposed swap would work

Q80: Suppose that the swap that you proposed

Q81: Consider the borrowing rates for Parties A

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents