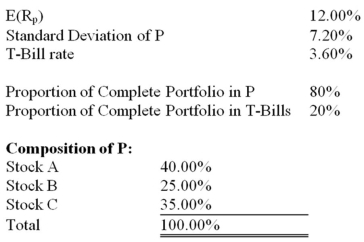

Your client, Bo Regard, holds a complete portfolio that consists of a portfolio of risky assets (P) and T-Bills.The information below refers to these assets.  What is the equation of Bo's capital allocation line

What is the equation of Bo's capital allocation line

A) E(rC) = 7.2 + 3.6 × Standard Deviation of C

B) E(rC) = 3.6 + 1.167 × Standard Deviation of C

C) E(rC) = 3.6 + 12.0 × Standard Deviation of C

D) E(rC) = 0.2 + 1.167 × Standard Deviation of C

E) E(rC) = 3.6 + 0.857 × Standard Deviation of C

Correct Answer:

Verified

Q37: Consider a T-bill with a rate of

Q39: An investor invests 30% of his wealth

Q41: Based on their relative degrees of risk

Q42: Your client, Bo Regard, holds a complete

Q45: An investor invests 30% of his wealth

Q45: You invest $100 in a risky asset

Q53: Asset allocation may involve

A) the decision as

Q55: An investor invests 35% of his wealth

Q56: You invest $1,000 in a risky asset

Q65: You invest $100 in a risky asset

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents