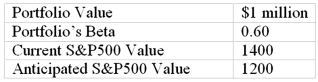

You are given the following information about a portfolio you are to manage.For the long-term you are bullish, but you think the market may fall over the next month.  For a 200-point drop in the S&P 500, by how much does the value of the futures position change

For a 200-point drop in the S&P 500, by how much does the value of the futures position change

A) $200,000

B) $50,000

C) $250,000

D) $500,000

E) $100,000

Correct Answer:

Verified

Q2: Which one of the following stock index

Q6: Suppose that the risk-free rates in the

Q14: Suppose that the risk-free rates in the

Q21: If you sold S&P 500 Index futures

Q24: The value of a futures contract for

Q24: Credit risk in the swap market

A)is extensive.

B)is

Q25: You are given the following information about

Q28: Which two indices had the lowest correlation

Q29: Hedging one commodity by using a futures

Q33: In the equation Profits = a +

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents