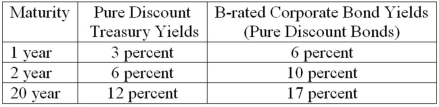

The following represents two yield curves.  What spread is expected between the one-year maturity B-rated bond and the one-year Treasury bond in one year?

What spread is expected between the one-year maturity B-rated bond and the one-year Treasury bond in one year?

A) 3.00 percent.

B) 5.06 percent.

C) 4.00 percent.

D) 5.00 percent.

E) 7.00 percent.

Correct Answer:

Verified

Q84: What does the Moody's Analytics model use

Q88: Suppose that the financial ratios of a

Q89: The following represents two yield curves.

Q90: Which of the following refers to the

Q90: Suppose that the financial ratios of a

Q91: The following information on the mortality rate

Q95: What is the essential idea behind RAROC?

A)Evaluating

Q97: Simulations by Moody's Analytics have shown which

Q100: From the lender's point of view, debt

Q103: Suppose that the financial ratios of a

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents