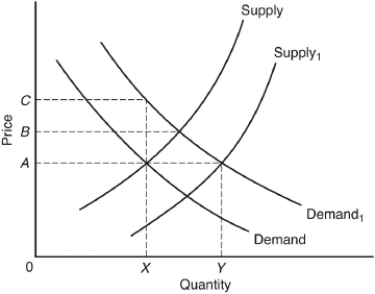

The following question are based on the following graph, showing short-run supply and demand curves for a perfectly competitive market. The initial supply curve is labeled "Supply" and the initial demand curve is labeled "Demand." Price 0A and output rate 0X represent the initial equilibrium price and output.

-For a typical producer in this market

A) marginal cost equals 0A.

B) average total cost is less than 0A.

C) average total cost is greater than 0A.

D) long-run average cost equals the supply curve.

E) average total cost equals the supply curve.

Correct Answer:

Verified

Q38: The relevant cost for making short-run production

Q39: The following question are based on the

Q40: The following question are based on the

Q41: The following question are based on the

Q42: Suppose all firms in an industry in

Q44: The following question are based on the

Q45: Compared to its initial position,a typical firm

Q46: Which of the following is a principal

Q47: In the long run,in a perfectly competitive

Q48: In the long run,perfectly competitive industries experiencing

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents