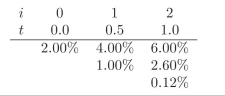

You are given the following interest rate tree. Use it when required in the

exercises.

-Using risk neutral pricing obtain the value for a put option on a 1.5 year zero coupon bond with K = 97.40, maturity at t = 1. Assume that p? = 0.7038 is constant over time.

Correct Answer:

Verified

Q1: Compute the spot rate duration for a

Q2: In order to compute the spot rate

Q4: Using risk neutral pricing obtain the value

Q5: How realistic is it to speak about

Q6: You are given the following interest rate

Q7: You are given the following interest rate

Q8: How realistic is it to speak about

Q9: Which of the following prices should be

Q10: What is one major drawback from using

Q11: What is the difference between risk neutral

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents