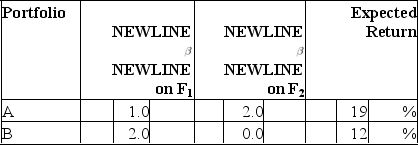

Consider the multifactor APT.There are two independent economic factors, F1andF2.The risk-free rate of return is 6%.The following information is available about two well-diversified portfolios:  Assuming no arbitrage opportunities exist, the risk premium on the factorF1portfolio should be

Assuming no arbitrage opportunities exist, the risk premium on the factorF1portfolio should be

A) 3%.

B) 4%.

C) 5%.

D) 6%.

Correct Answer:

Verified

Q22: A zero-investment portfolio with a positive expected

Q23: The APT requires a benchmark portfolio

A)that is

Q25: Which of the following factors might affect

Q25: Consider the multifactor APT.There are two independent

Q26: The factor F in the APT model

Q28: An investor will take as large a

Q29: Consider the single factor APT.Portfolios A and

Q32: In terms of the risk/return relationship in

Q34: A well-diversified portfolio is defined as

A) one

Q40: The APT differs from the CAPM because

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents