Advanced Accounting 12th Edition by Joe Ben Hoyle,Thomas Schaefer , Timothy Doupnik

Edition 12ISBN: 978-0077862220Advanced Accounting 12th Edition by Joe Ben Hoyle,Thomas Schaefer , Timothy Doupnik

Edition 12ISBN: 978-0077862220 Exercise 51

On February 18, 2014, Q-Car Corporation announced its plan to acquire 90 percent of the outstanding 1,000,000 shares InstaPower Corporation's common stock in a business combination later in the year following regulatory approval. Q-Car will account for the transaction in accordance with ASC 805, "Business Combinations."

On May 1, 2014, Q-Car purchased a 90 percent controlling interest in InstaPower's outstanding voting shares. On this date, Q-Car paid $60 million in cash and issued one million shares of Q-Car common stock to the selling shareholders of InstaPower. Q-Car's share price was $20 on the announcement date and $27 on the acquisition date.

InstaPower's remaining 100,000 shares of common stock are owned by a small number of investors who do not actively trade their shares. Using other valuation techniques (comparable firms, discounted cash flow analysis, etc.), Q-Car estimated the fair value of the InstaPower's noncontrolling shares at $11,000,000.

The parties agreed that Q-Car would issue to the selling shareholders an additional one million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

InstaPower has a research and development (R D) project underway to develop a fast charging battery technology. The technology has a fair value of $14 million. Q-Car considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in InstaPower's financial records for the R D costs to date.

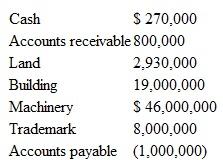

InstaPower's other assets and liabilities (at fair values) include the following:

Neither the receivables nor payables involve Q-Car.

Answer the following questions citing relevant support from the ASC and IFRS.

1. What is the total consideration transferred by Q-Car to acquire its 90 percent controlling interest in InstaPower

2. What values should Q-Car assign to identifiable intangible assets as part of the acquisition accounting

3. What is the acquisition-date value assigned to the 10 percent noncontrolling interest What are the potential noncontrolling interest valuation alternatives available under IFRS

4. Under U.S. GAAP, what amount should Q-Car recognize as goodwill from the InstaPower acquisition What alternative goodwill valuations are allowed under IFRS

On May 1, 2014, Q-Car purchased a 90 percent controlling interest in InstaPower's outstanding voting shares. On this date, Q-Car paid $60 million in cash and issued one million shares of Q-Car common stock to the selling shareholders of InstaPower. Q-Car's share price was $20 on the announcement date and $27 on the acquisition date.

InstaPower's remaining 100,000 shares of common stock are owned by a small number of investors who do not actively trade their shares. Using other valuation techniques (comparable firms, discounted cash flow analysis, etc.), Q-Car estimated the fair value of the InstaPower's noncontrolling shares at $11,000,000.

The parties agreed that Q-Car would issue to the selling shareholders an additional one million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

InstaPower has a research and development (R D) project underway to develop a fast charging battery technology. The technology has a fair value of $14 million. Q-Car considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in InstaPower's financial records for the R D costs to date.

InstaPower's other assets and liabilities (at fair values) include the following:

Neither the receivables nor payables involve Q-Car.

Answer the following questions citing relevant support from the ASC and IFRS.

1. What is the total consideration transferred by Q-Car to acquire its 90 percent controlling interest in InstaPower

2. What values should Q-Car assign to identifiable intangible assets as part of the acquisition accounting

3. What is the acquisition-date value assigned to the 10 percent noncontrolling interest What are the potential noncontrolling interest valuation alternatives available under IFRS

4. Under U.S. GAAP, what amount should Q-Car recognize as goodwill from the InstaPower acquisition What alternative goodwill valuations are allowed under IFRS

Explanation

This question doesn’t have an expert verified answer yet, let Quizplus AI Copilot help.

Advanced Accounting 12th Edition by Joe Ben Hoyle,Thomas Schaefer , Timothy Doupnik

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255