Auditing and Assurance Services 1st Edition by Iris Stuart

Edition 1ISBN: 978-0073404004Auditing and Assurance Services 1st Edition by Iris Stuart

Edition 1ISBN: 978-0073404004 Exercise 47

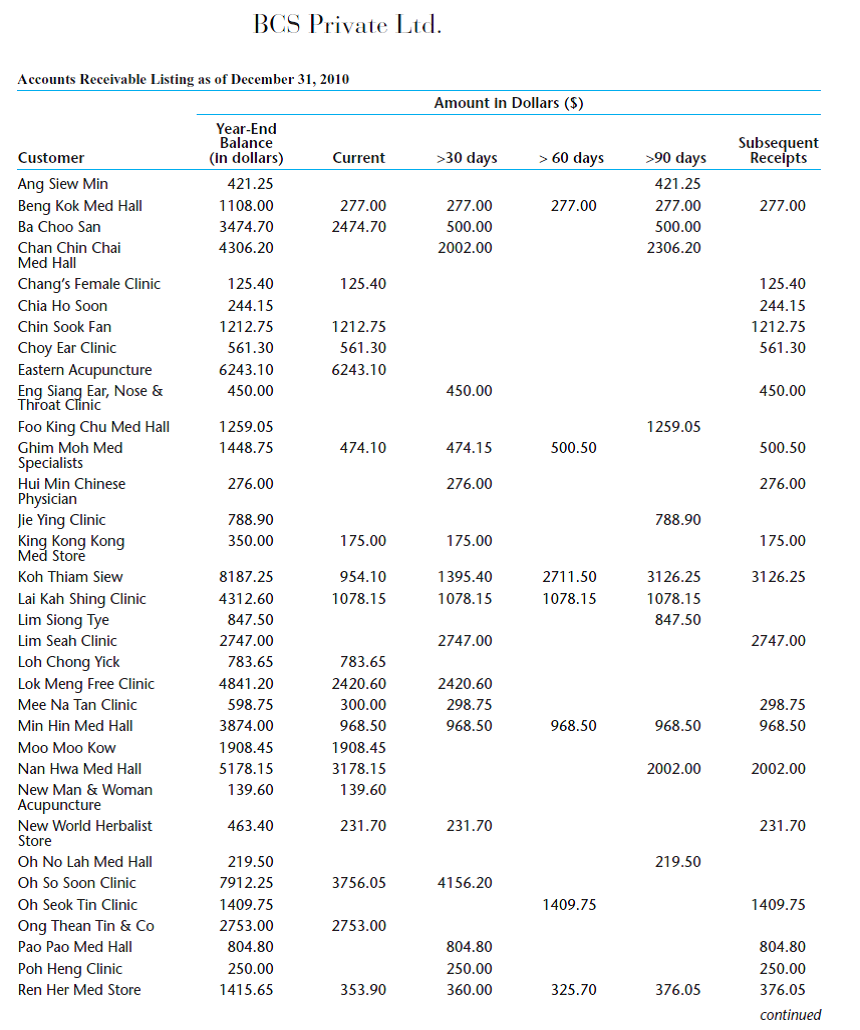

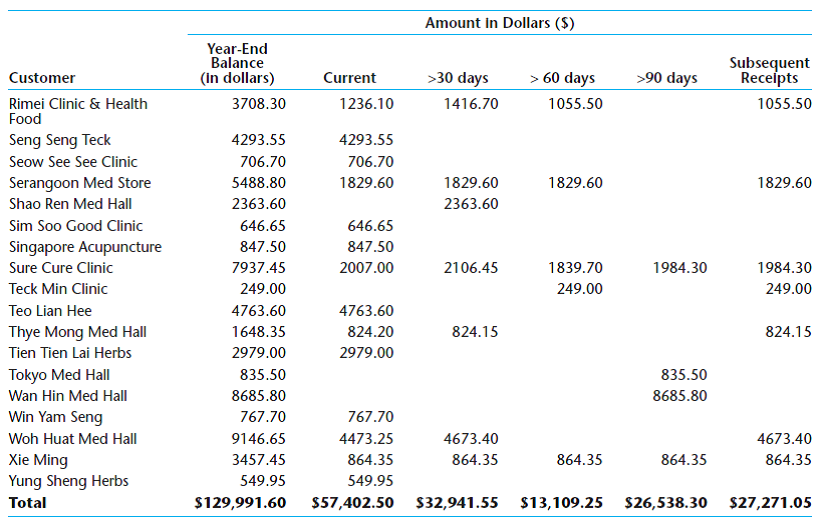

Evaluating the allowance for doubtful accounts. See Appendix B for the aged receivables trial balance for BCS. Review it and explain what the information in each column represents.

a. Use this information to calculate a bad debt provision for BCS at December 31, 2010 Last year BCS used the following percentages to calculate the bad debt provision: current accounts, .05%; 30 day accounts, 2%; 60 day accounts, 10%; 90 day accounts, 40%. First calculate the allowance using the percentages applicable in the previous year. Then, if you determine that actual write-offs last year were $20,000 more than the provision and that the economic conditions for BCS customers has worsened in the current year, explain how you could adjust the allowance.

b. Why is it necessary for BCS to estimate bad debt expense at year-end What accounting principle does BCS violate if it does not estimate bad debt

a. Use this information to calculate a bad debt provision for BCS at December 31, 2010 Last year BCS used the following percentages to calculate the bad debt provision: current accounts, .05%; 30 day accounts, 2%; 60 day accounts, 10%; 90 day accounts, 40%. First calculate the allowance using the percentages applicable in the previous year. Then, if you determine that actual write-offs last year were $20,000 more than the provision and that the economic conditions for BCS customers has worsened in the current year, explain how you could adjust the allowance.

b. Why is it necessary for BCS to estimate bad debt expense at year-end What accounting principle does BCS violate if it does not estimate bad debt

Explanation Verified

Verified

Accounts receivable:

It is the amount d...

Auditing and Assurance Services 1st Edition by Iris Stuart

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255