Cost Management: A Strategic Emphasis 5th Edition by David Stout, Edward Blocher, Gary Cokins

Edition 5ISBN: 0073526940Cost Management: A Strategic Emphasis 5th Edition by David Stout, Edward Blocher, Gary Cokins

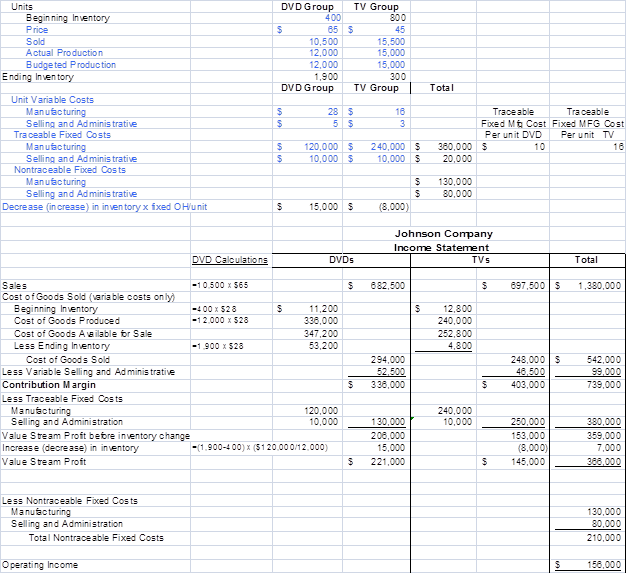

Edition 5ISBN: 0073526940Value Streams and Profit Centers Johnson Company is a manufacturer of very inexpensive DVD players and television sets. The company uses recycled parts and a highly structured manufacturing process to keep costs low so that it can sell at very low prices. The company uses lean accounting procedures to help keep costs low and to examine financial performance. Johnson uses value streams to study the profitability of its two main product groups, DVD players and TVs. Information about finished goods inventory, sales, production, and average sales price follows.

| DVD Group | TV Group |

Units |

|

|

Beginning inventory | 400 | 800 |

Price | $ 65 | $ 45 |

Sold | 10,500 | 15,500 |

Budgeted and Actual production | 12,000 | 15,000 |

Johnson’s costs for the current quarter are as follows. Note that some of the company’s manufacturing and selling costs are traceable directly to the two value streams, while other costs are not traceable. Johnson considers all fixed costs to be controllable by the manager of each group. Also, Johnson’s value stream shows operating income determined by the full cost method; the difference from the traditional full cost income statement is that the effect on income from a change in inventory is shown as a separate item on the value stream income statement.

| DVD Group | TV Group | Total |

Unit variable costs |

|

|

|

Manufacturing | $ 28 | $ 16 |

|

Selling and administrative | 5 | 3 |

|

Traceable fixed costs |

|

|

|

Manufacturing | 120,000 | 240,000 | $ 360,000 |

Selling and administrative | 10,000 | 10,000 | 20,000 |

Nontraceable fixed costs |

|

|

|

Manufacturing |

|

| 130,000 |

Selling and administrative |

|

| 80,000 |

Required

1. Consider Johnson’s two value streams as profit centers and use the contribution income statement (Exhibit 18.9) as a guide to develop a value stream income statement for the company. In your solution, replace the term controllable margin (in Exhibit 18.9) with value-stream income. Be sure to include the inventory effect on profit as a separate line item in your value stream income statement.

2. Interpret the findings of the analysis you completed in part 1.

3. What is the benefit of the use of value streams for evaluating profit centers relative to the use of the contribution income statement for individual product lines?

Step 1 of 3

Value Streams and Profit Centers (30 min)

1.? The value stream income statements for the two value streams of Johnson Company is shown below. The value stream income statement is based on a contribution type income statement (variable costing-based) to which is added the effect of a change in inventory level on profit, thereby converting the variable costing income statement to a full cost statement.

Note that the effect on value stream income of a change in inventory is displayed separately in the income statement; there is a $15,000 increase in income for the DVD group (because of an increase in inventory of DVDs; ending inventory increases from 400 to 1,900, where 1,900=400+12,000-10,500) and a decrease in value stream income for the TV group (because of the decrease in inventory of TVs, from 800 to 300, where 300=800+15,000-15,500). Note also that nontraceable fixed costs are not allocated to the value streams but are subtracted from total company profit to produce a total company operating income of $156,000.

Step 2 of 3

Step 3 of 3

Why don’t you like this exercise?

Other