Cost Management: A Strategic Emphasis 5th Edition by David Stout, Edward Blocher, Gary Cokins

Edition 5ISBN: 0073526940Cost Management: A Strategic Emphasis 5th Edition by David Stout, Edward Blocher, Gary Cokins

Edition 5ISBN: 0073526940Operation Costing

Brian Canning Co., which sells canned corn, uses an operation costing system. Cans of corn are classified as either sweet or regular, depending on the type of corn used. Both types of corn go through the separating and cleaning operations, but only regular corn goes through the creaming operation. During January, two batches of corn were canned from start to finish. Batch X consisted of 800 pounds of sweet corn and batch Y consisted of 700 pounds of regular corn. The company had no beginning or ending work-in-process inventory. The following cost information is for the month of January:

| Batch | Cost | Batch Size |

Raw sweet corn | X | $5,200 | 800 LB |

Raw regular corn | Y | 2,450* | 700 LB |

Separating department costs |

| 1,500 |

|

Cleaning department costs |

| 900 |

|

Creaming department costs |

| 210 |

|

*Includes $300 for cream.

Required

1. Compute the unit cost for sweet corn and regular corn.

2. Record appropriate journal entries.

Step 1 of 3

Operation Costing is a dual approach costing system which accumulates and assigns cost incurred using the two different approaches based on the type of cost. Operation Costing system hold good in those organization where direct material differs across multiple products or services, but common or similar (homogeneous) processes are used for conversion activities.

The following table explains the methodology used under Operation Costing:

For example:

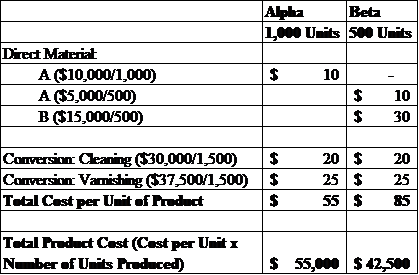

ABC Corporation manufactures two products, Alpha and Beta. Both the products starts with the same material, but beta belongs to a more premium category and required some additional materials.

Moreover, the process of cleaning and varnishing is similar across both the products. The following table provides for the quantity produced and costs incurred in the month of August 2020:

The above table clearly picturizes the differential between job costing and process costing as Direct Materials can be traced to each individual product or job whereas Conversion Costs are accumulated in total.

Therefore, we will prepare a Product Cost computation Sheet to determine the cost per unit of Alpha and Beta using Operation Costing Mechanism.

As can be seen from the above table, that Material A and B are separately identified, accumulated, and assigned to products. On the other side, Conversion cost of cleaning and varnishing are allocated between Alpha and Beta using a homogeneous approach thus conversion cost per unit remains same across both segments.

Step 2 of 3

Step 3 of 3

Why don’t you like this exercise?

Other