Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in VOLAT.RAW for this exercise.

(i) Estimate an AR(3) model for pcip. Now, add a fourth lag and verify that it is very insignificant.

(ii) To the AR(3) model from part (i), add three lags of pcsp to test whether pcsp Granger causes pcip. Carefully, state your conclusion.

(iii) To the model in part (ii), add three lags of the change in i3, the three-month T-bill rate. Does pcsp Granger cause pcip conditional on past ?i3?

Step 1 of 5

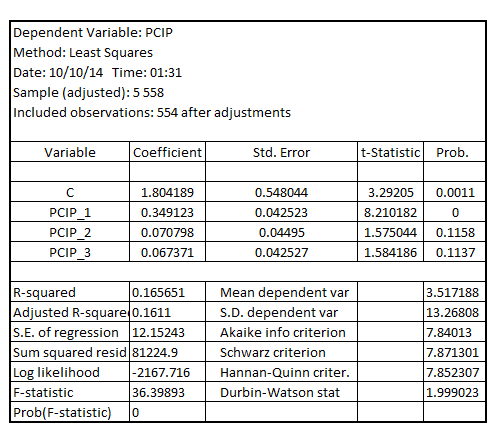

(i)

Estimating AR (3) model for , the result is:

, the result is:

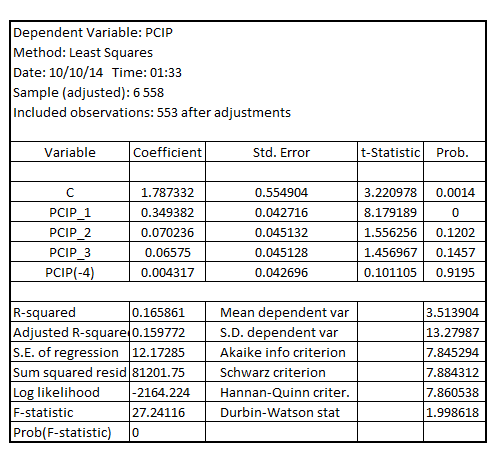

On adding the fourth lag for , the result is:

, the result is:

The p-value of the coefficient of the fourth lag for , that is of

, that is of is 0.9195 which is greater than the critical p-value of 0.05 at 5% level of significance. This indicates that the fourth lag of

is 0.9195 which is greater than the critical p-value of 0.05 at 5% level of significance. This indicates that the fourth lag of is very insignificant

is very insignificant

Step 2 of 5

Step 3 of 5

Step 4 of 5

Step 5 of 5

Why don’t you like this exercise?

Other