Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in CRIME1 to answer this question.

(i) For the OLS estimates reported in Table 17.5, find the heteroskedasticity-robust standard errors. In terms of statistical significance of the coefficients, are there any notable changes?

(ii) Obtain the fully robust standard errors—that is, those that do not even require assumption (17.35)—for the Poisson regression estimates in the second column. (This requires that you have a statistical package that computes the fully robust standard errors.) Compare the fully robust 95% confidence interval for ?pcnv with that obtained using the standard error in Table 17.5.

(iii) Compute the average partial effects for each variable in the Poisson regression model. Use the formula for binary explanatory variables for black, hispan, and born60. Compare the APEs for qemp86 and inc86 with the corresponding OLS coefficients.

(iv) If your statistical package reports the robust standard errors for the APEs in part (iii), compare the robust t statistic for the OLS estimate of ?pcnv with the robust t statistic for the APE of pcnv in the Poisson regression.

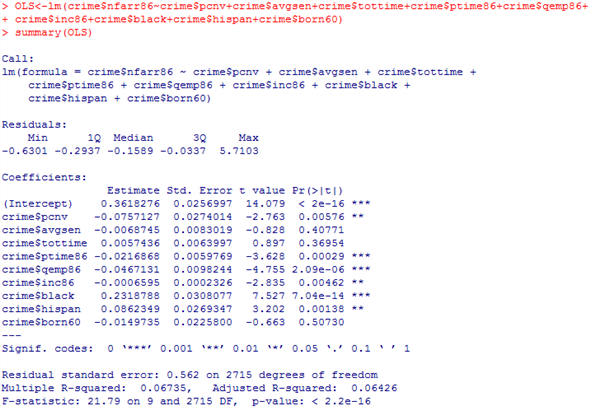

Step 1 of 4

(i)

The R command to read the data and find standard errors for OLS estimates provided in table 17.5 is as shown below:

Therefore, the standard errors for the variables in the model are as follows:

| Variables | Standard Error |

| pcnv | 0.027 |

| avgsen | 0.008 |

| tottime | 0.006 |

| ptime86 | 0.005 |

| qemp86 | 0.009 |

| inc86 | 0.0002 |

| black | 0.030 |

| hispan | 0.026 |

| born60 | 0.022 |

| constant | 0.025 |

There are no prominent changes in the significant relationship of the variables with dependent variable.

Step 2 of 4

Step 3 of 4

Step 4 of 4

Why don’t you like this exercise?

Other