Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XThe purpose of this exercise is to compare the estimates and standard errors obtained by correctly using 2SLS with those obtained using inappropriate procedures. Use the

data file WAGE2.RAW.

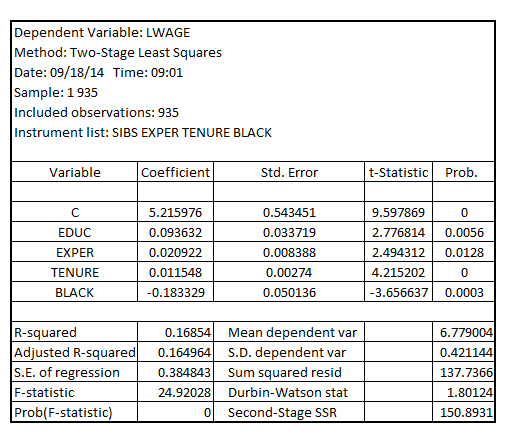

(i) Use a 2SLS routine to estimate the equation

log(wage) = ?0 + ?1educ + ?2exper + ?3tenure + ?4black + u,

where sibs is the IV for educ. Report the results in the usual form.

(ii) Now, manually carry out 2SLS. That is, first regress educi on sibsi, experi, tenurei, and blacki and obtain the fitted values, educi = 1, n. Then, run the second stage regression log(wage.) on educt, experi, tenurei, and blacki = 1, n. Verify that the

are identical to those obtained from part (i), but that the standard errors are somewhat different. The standard errors obtained from the second stage regression when manually carrying out 2SLS are generally inappropriate.

(iii) Now, use the following two-step procedure, which generally yields inconsistent parameter estimates of the ?j, and not just inconsistent standard errors. In step one, regress educi on sibsi only and obtain the fitted values, say educi. (Note that this is an incorrect first stage regression.) Then, in the second step, run the regression of log(wage) on educi, experi, tenurei, and blacki, i = 1, ...,n. How does the estimate from this incorrect, two-step procedure compare with the correct 2SLS estimate of the return to education?

Step 1 of 5

(i)

Estimating the 2SLS model given by:

Assuming  as IV for

as IV for , the result is:

, the result is:

The usual form is:

Step 2 of 5

Step 3 of 5

Step 4 of 5

Step 5 of 5

Why don’t you like this exercise?

Other