Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010X Exercise 12

(i) In the model with one endogenous explanatory variable, one exogenous explanatory variable, and one extra exogenous variable, take the reduced form for y2,

, and plug it into the structural equation

. This gives the reduced form for y1:

y1 = ?0 + ?1Z1 + ?2Z2 + V

Find the ?j. in terms of the ?j and the ?j.

(ii) Find the reduced form error, v1, in terms of u1, v2, and the parameters.

(iii) How would you consistently estimate the aj?

Step-by-step solution Verified

Verified

Step 1 of 3

(i)

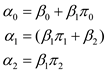

Consider the model with one endogenous explanatory variable and one exogenous explanatory variable

Now consider the reduced form of

On plugging  in

in , the result is:

, the result is:

On comparing with

Step 2 of 3

Step 3 of 3

Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255