Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in INTDEF.RAW for this exercise. A simple equation relating the three-month T-bill rate to the inflation rate (constructed from the Consumer Price Index) is

i3t = ?0 + ?1inf + ut.

(i) Estimate this equation by OLS, omitting the first time period for later comparisons. Report the results in the usual form.

(ii) Some economists feel that the Consumer Price Index mismeasures the true rate of inflation, so that the OLS from part (i) suffers from measurement error bias. Reestimate the equation from part (i), using inft-1 as an IV for inft. How does the IV estimate of ?1 compare with the OLS estimate?

(iii) Now, first difference the equation:

?i3t = ?0 + ?l?inft + ?ut.

Estimate this by OLS and compare the estimate of ?1 with the previous estimates.

(iv) Can you use ?inft-1 as an IV for ?inft in the differenced equation in part (iii)? Explain. (Hint: Are ?inft and ?inft-1 sufficiently correlated?)

Step 1 of 5

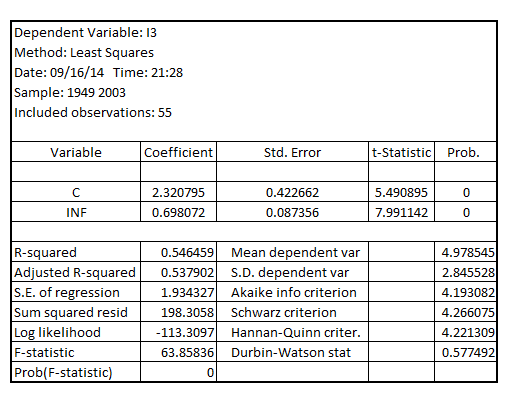

(i)

There are observations in INTDEF.RAW relating to the period 1948-2003

On omitting the first time period, that is 1948 and estimating the regression of  on

on , the result is:

, the result is:

The usual for of the result is:

Step 2 of 5

Step 3 of 5

Step 4 of 5

Step 5 of 5

Why don’t you like this exercise?

Other