Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XWith a single explanatory variable, the equation used to obtain the between estimator is

![With a single explanatory variable, the equation used to obtain the between estimator is where the overbar represents the average over time. We can assume that E(ai) = 0 because we have included an intercept in the equation. Suppose that ?i. is uncorrelated with but Cov(xit, ai) = ?xa for all t (and i because of random sampling in the cross section). <blockquote> (i) Letting be the between estimator, that is, the OLS estimator using the time aver¬ages, show that where the probability limit is defined as N ? ?. [Hint: See equations] (ii) Assume further that the xit, for all t = 1, 2,T, are uncorrelated with constant variance a2. Show that plim = ?1 + T (?xa?2x). (iii) If the explanatory variables are not very highly correlated across time, what does part (ii) suggest about whether the inconsistency in the between estimator is smaller when there are more time periods? </blockquote> Equation](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/616187e6_46ff_4d60_9d68_773157a86156_SMCC2709_11.jpg)

where the overbar represents the average over time. We can assume that E(ai) = 0 because we have included an intercept in the equation. Suppose that ?i. is uncorrelated with ![With a single explanatory variable, the equation used to obtain the between estimator is where the overbar represents the average over time. We can assume that E(ai) = 0 because we have included an intercept in the equation. Suppose that ?i. is uncorrelated with but Cov(xit, ai) = ?xa for all t (and i because of random sampling in the cross section). <blockquote> (i) Letting be the between estimator, that is, the OLS estimator using the time aver¬ages, show that where the probability limit is defined as N ? ?. [Hint: See equations] (ii) Assume further that the xit, for all t = 1, 2,T, are uncorrelated with constant variance a2. Show that plim = ?1 + T (?xa?2x). (iii) If the explanatory variables are not very highly correlated across time, what does part (ii) suggest about whether the inconsistency in the between estimator is smaller when there are more time periods? </blockquote> Equation](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/6c32b02c_97e4_4519_b638_af11d96990d8_SMCC2709_11.jpg) but Cov(xit, ai) = ?xa for all t (and i because of random sampling in the cross section).

but Cov(xit, ai) = ?xa for all t (and i because of random sampling in the cross section).

(i) Letting

be the between estimator, that is, the OLS estimator using the time aver¬ages, show that

where the probability limit is defined as N ? ?. [Hint: See equations]

(ii) Assume further that the xit, for all t = 1, 2,T, are uncorrelated with constant variance a2. Show that plim

= ?1 + T (?xa?2x).

(iii) If the explanatory variables are not very highly correlated across time, what does part (ii) suggest about whether the inconsistency in the between estimator is smaller when there are more time periods?

![With a single explanatory variable, the equation used to obtain the between estimator is where the overbar represents the average over time. We can assume that E(ai) = 0 because we have included an intercept in the equation. Suppose that ?i. is uncorrelated with but Cov(xit, ai) = ?xa for all t (and i because of random sampling in the cross section). <blockquote> (i) Letting be the between estimator, that is, the OLS estimator using the time aver¬ages, show that where the probability limit is defined as N ? ?. [Hint: See equations] (ii) Assume further that the xit, for all t = 1, 2,T, are uncorrelated with constant variance a2. Show that plim = ?1 + T (?xa?2x). (iii) If the explanatory variables are not very highly correlated across time, what does part (ii) suggest about whether the inconsistency in the between estimator is smaller when there are more time periods? </blockquote> Equation](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/93ec9097_23a4_4ed7_94e9_2050fa2bbf5d_SMCC2709_11.jpg)

Equation

![With a single explanatory variable, the equation used to obtain the between estimator is where the overbar represents the average over time. We can assume that E(ai) = 0 because we have included an intercept in the equation. Suppose that ?i. is uncorrelated with but Cov(xit, ai) = ?xa for all t (and i because of random sampling in the cross section). <blockquote> (i) Letting be the between estimator, that is, the OLS estimator using the time aver¬ages, show that where the probability limit is defined as N ? ?. [Hint: See equations] (ii) Assume further that the xit, for all t = 1, 2,T, are uncorrelated with constant variance a2. Show that plim = ?1 + T (?xa?2x). (iii) If the explanatory variables are not very highly correlated across time, what does part (ii) suggest about whether the inconsistency in the between estimator is smaller when there are more time periods? </blockquote> Equation](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/f93141ec_82b5_4b3e_868e_9c263831da2e_SMCC2709_11.jpg)

![With a single explanatory variable, the equation used to obtain the between estimator is where the overbar represents the average over time. We can assume that E(ai) = 0 because we have included an intercept in the equation. Suppose that ?i. is uncorrelated with but Cov(xit, ai) = ?xa for all t (and i because of random sampling in the cross section). <blockquote> (i) Letting be the between estimator, that is, the OLS estimator using the time aver¬ages, show that where the probability limit is defined as N ? ?. [Hint: See equations] (ii) Assume further that the xit, for all t = 1, 2,T, are uncorrelated with constant variance a2. Show that plim = ?1 + T (?xa?2x). (iii) If the explanatory variables are not very highly correlated across time, what does part (ii) suggest about whether the inconsistency in the between estimator is smaller when there are more time periods? </blockquote> Equation](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/0c87e4f1_6a8c_4538_93f4_5d9395cc932a_SMCC2709_11.jpg)

Step 1 of 3

Consider the single explanatory variable

The equation to obtain the between estimator is:

The overbar in the equation represents the average over time

Assume and consider that

and consider that  is uncorrelated with

is uncorrelated with

Also consider  for all

for all

Thus, it can be concluded that:

(i)

Given that  is the between estimator

is the between estimator

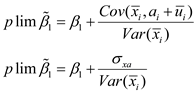

In the simple regression case, the inconsistency in  (also called asymptotic bias) is given by:

(also called asymptotic bias) is given by:

Since,

This implies

Hence,

Step 2 of 3

Step 3 of 3

Why don’t you like this exercise?

Other