Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XConsider the version of Fair's model in Example 10.6. Now, rather than predicting the proportion of the two-party vote received by the Democrat, estimate a linear probability model for whether or not the Democrat wins.

(i) Use the binary variable demwins in place of demvote in (10.23) and report the results in standard form. Which factors affect the probability of winning? Use the data only through 1992.

(ii) How many fitted values are less than zero? How many are greater than one?

(iii) Use the following prediction rule: if

you predict the Democrat wins; otherwise, the Republican wins. Using this rule, determine how many of the 20 elections are correctly predicted by the model.

(iv) Plug in the values of the explanatory variables for 1996. What is the predicted probability that Clinton would win the election? Clinton did win; did you get the correct prediction?

(v) Use a heteroskedasticity-robust t test for AR(1) serial correlation in the errors. What do you find?

(vi) Obtain the heteroskedasticity-robust standard errors for the estimates in part (i). Are there notable changes in any t statistics?

Step 1 of 8

(i)

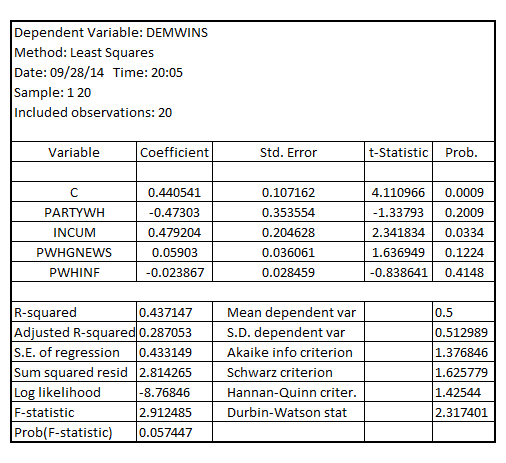

Estimating the linear probability model that regress  on

on , the result is:

, the result is:

It shall be noted that the coefficient of  is with the p-value 0.0334 which is less than the critical p-value of 0.05 at 5% level of significance, indicating that

is with the p-value 0.0334 which is less than the critical p-value of 0.05 at 5% level of significance, indicating that  is the statistically significant variable at 5% level of significance that affect the probability of winning

is the statistically significant variable at 5% level of significance that affect the probability of winning

Step 2 of 8

Step 3 of 8

Step 4 of 8

Step 5 of 8

Step 6 of 8

Step 7 of 8

Step 8 of 8

Why don’t you like this exercise?

Other