Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010X(i) Use NYSE.RAW to estimate equation. Let ?t. be the fitted values from this equation (the estimates of the conditional variance). How many ?t are negative?

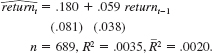

(ii) Add return1 1 to (12.48) and again compute the fitted values, ?t . Are any ?t t negative?

(iii) Use the ?t from part (ii) to estimate (12.47) by weighted least squares (as in Section 8.4). Compare your estimate of ?t with that in equation. Test H0: ?t = 0 and compare the outcome when OLS is used.

(iv) Now, estimate (12.47) by WLS, using the estimated ARCH model in (12.51) to obtain the ?t . Does this change your findings from part (iii)?

Step 1 of 4

i)

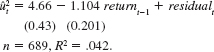

After obtaining the residuals  from equation

from equation  and then estimating the required equation, one can compute the fitted values

and then estimating the required equation, one can compute the fitted values

This is easily done in a single using command using most software packages. It turns out that 12 of 689 fitted values are negative.

Among other things, this means one cannot directly apply weighted least squares using the heteroskedasticity function in the given equation.

Step 2 of 4

Step 3 of 4

Step 4 of 4

Why don’t you like this exercise?

Other