Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XC11.9 Use the data in TRAFFIC2.RAW for this exercise. Computer Exercise C10.11 previously asked for an analysis of these data.

(i) Compute the first order autocorrelation coefficient for the variable prcfat. Are you concerned that prcfat contains a unit root? Do the same for the unemployment rate.

(ii) Estimate a multiple regression model relating the first difference of prcfat, ?prcfat, to the same variables in part (vi) of Computer Exercise C10.11, except you should first difference the unemployment rate, too. Then, include a linear time trend, monthly dummy variables, the weekend variable, and the two policy variables; do not difference these. Do you find any interesting results?

(iii) Comment on the following statement: “We should always first difference any time series we suspect of having a unit root before doing multiple regression because it is the safe strategy and should give results similar to using the levels.” [In answering this, you may want to do the regression from part (vi) of Computer Exercise C10.11, if you have not already.]

Step 1 of 7

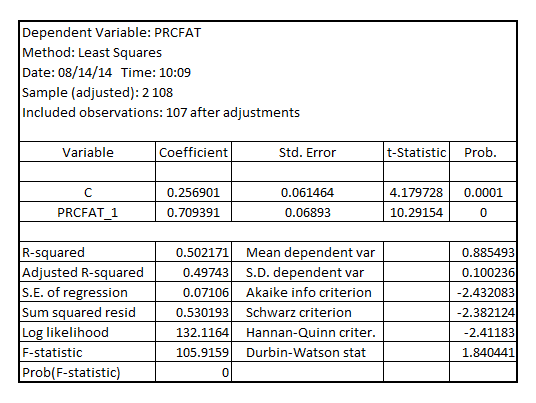

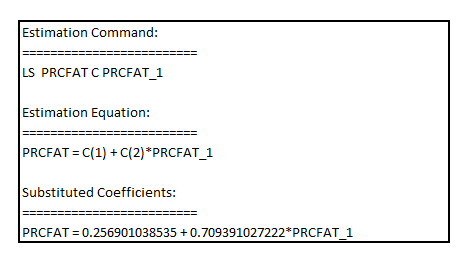

(i)

The first order autocorrelation coefficient of the variable  is obtained as the coefficient of

is obtained as the coefficient of  in the AR (1) model:

in the AR (1) model:

The result is:

Step 2 of 7

Step 3 of 7

Step 4 of 7

Step 5 of 7

Step 6 of 7

Step 7 of 7

Why don’t you like this exercise?

Other