Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XLet invent be the real value inventories in the United States during year t, let GDPt denote real gross domestic product, and let r3t denote the (ex post) real interest rate on three-month T-bills. The ex post real interest rate is (approximately) r3t =i3t – inft, where i3t is the rate on three-month T-bills and inft is the annual inflation rate [see Mankiw (1994, Section)]. The change in inventories, ?invent, is the inventory investment for the year. The accelerator model of inventory investment is

?invent = ?0 + ?1?GDPt + ut, where ?1 ? 0. [See, for example, Mankiw (1994), Chapter 17.]

(i) Use the data in INVEN.RAW to estimate the accelerator model. Report the results in the usual form and interpret the equation. Is

statistically greater than zero?

(ii) If the real interest rate rises, then the opportunity cost of holding inventories rises, and so an increase in the real interest rate should decrease inventories. Add

the real interest rate to the accelerator model and discuss the results.

(iii) Does the level of the real interest rate work better than the first difference, ?r3t?

Step 1 of 4

(i)

The accelerator model is given by:

Where,

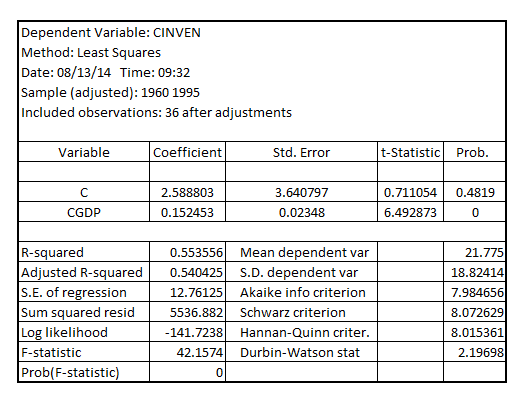

On executing this regression model, the result obtained is as follows:

The accelerator model in the standard form is given by:

Given this regression model, a $ 1bn change in  brings in $ 152.4 mn increased in inventories investment. The coefficient of

brings in $ 152.4 mn increased in inventories investment. The coefficient of  is 0.1524 with the p-value 0.0000 which is less than the critical p-value of 0.05 at 5% level of significance. From this, it can be concluded that the coefficient of

is 0.1524 with the p-value 0.0000 which is less than the critical p-value of 0.05 at 5% level of significance. From this, it can be concluded that the coefficient of  is significant.

is significant.

Step 2 of 4

Step 3 of 4

Step 4 of 4

Why don’t you like this exercise?

Other