Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in FERTIL3.RAW for this exercise.

(i) Add pet-3 and pet-4 to equation (10.19). Test for joint significance of these lags.

(ii) Find the estimated long-run propensity and its standard error in the model from part (i). Compare these with those obtained from equation (10.19).

(iii) Estimate the polynomial distributed lag model from Problem 10.6. Find the estimated LRP and compare this with what is obtained from the unrestricted model.

Step 1 of 4

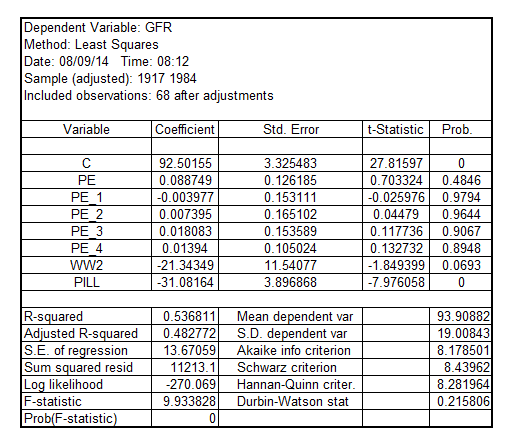

(i)

On adding  and

and , the regression equation is:

, the regression equation is:

The result is:

The regression equation is:

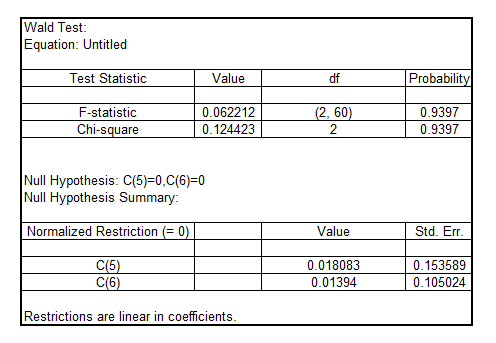

Test for the joint significance of the lagged variables  and

and using Wald test

using Wald test

and

and are not jointly significant

are not jointly significant

and

and are jointly significant

are jointly significant

Since, the p-value of the F-statistic is 0.9397 which is greater than the critical p-value of 0.05 at 5% level of significance, it is concluded that  and

and are not jointly significant

are not jointly significant

Step 2 of 4

Step 3 of 4

Step 4 of 4

Why don’t you like this exercise?

Other