Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010X Exercise 11

Use the data in FERTIL3.RAW for this exercise.

(i) Regress gfrt on t and t2 and save the residuals. This gives a detrended gfrt, say

,

(ii) Regress

on all of the variables in equation (10.35), including t and t2. Compare the R-squared with that from (10.35). What do you conclude?

(iii) Reestimate equation (10.35) but add t3 to the equation. Is this additional term statistically significant?

Step-by-step solution Verified

Verified

Step 1 of 4

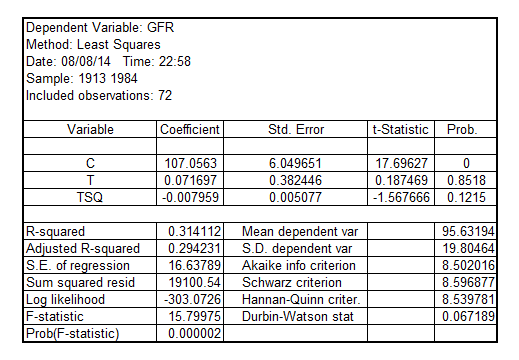

(i)

On regressing the variable  on

on  and

and  , the result is:

, the result is:

The regression equation is

Consider

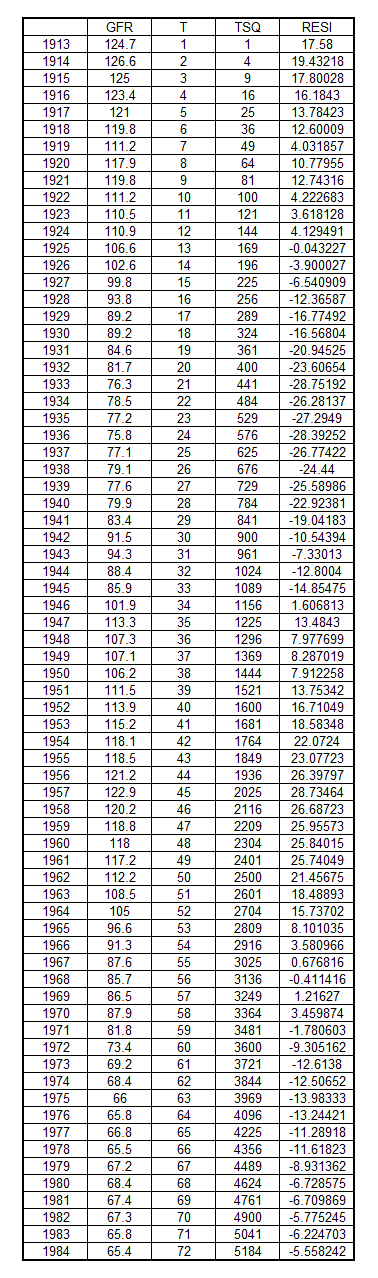

The  is the residual or detrended

is the residual or detrended and they are shown as follows:

and they are shown as follows:

Step 2 of 4

Step 3 of 4

Step 4 of 4

Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255