Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data set 401KSUBS.RAW for this exercise.

(i) Using OLS, estimate a linear probability model for e401k, using as explanatory variables inc, inc2, age, age2, and male. Obtain both the usual OLS standard errors and the heteroskedasticity-robust versions. Are there any important differences?

(ii) In the special case of the White test for heteroskedasticity, where we regress the squared OLS residuals on a quadratic in the OLS fitted values,

i = 1, ..., n, argue that the probability limit of the coefficient on ?i should be one, the probability limit of the coefficient on ?i2 should be — 1, and the probability limit of the intercept should be zero. {Hint: Remember that Var(y|x1, xk) = p(x)[1 — p(x)], where p(x) = ?0 + ?1x1 + ... + ?kxk.}

(iii) For the model estimated from part (i), obtain the White test and see if the coefficient estimates roughly correspond to the theoretical values described in part (ii).

(iv) After verifying that the fitted values from part (i) are all between zero and one, obtain the weighted least squares estimates of the linear probability model. Do they differ in important ways from the OLS estimates?

Step 1 of 7

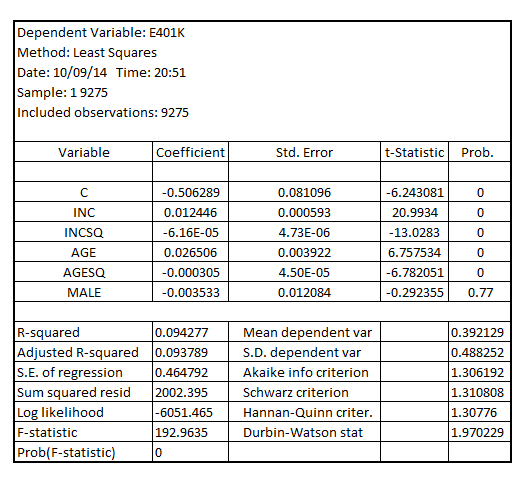

(i)

Estimating the linear probability model for  using the explanatory variables

using the explanatory variables using OLS and usual-OLS standard error, the result is:

using OLS and usual-OLS standard error, the result is:

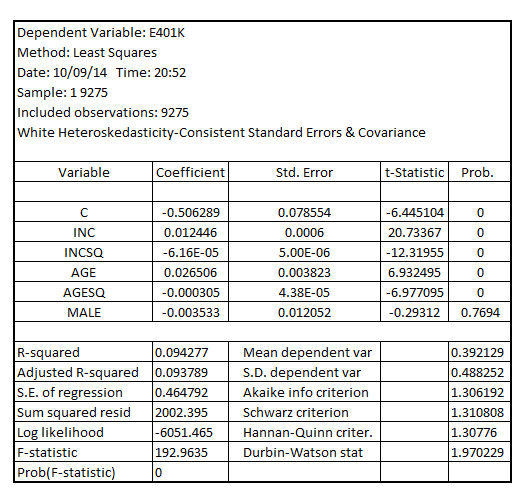

Estimating the linear probability model for  using the explanatory variables

using the explanatory variables using OLS and heteroscedasticity-robust standard error, the result is:

using OLS and heteroscedasticity-robust standard error, the result is:

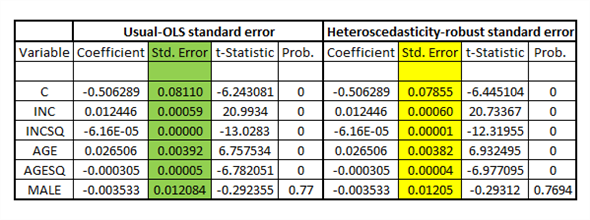

On comparing the usual-OLS standard error with heteroscedasticity-robust standard error, the result is:

The heteroscedasticity-robust standard error is lower marginally for the explanatory variables  vis-à-vis usual-OLS standard error, but the difference is not so important as the variables that were statistically significant at 5% level of significance when assuming usual-OLS standard error remained statistically significant at 5% level of significance when assuming heteroscedasticity-robust standard error

vis-à-vis usual-OLS standard error, but the difference is not so important as the variables that were statistically significant at 5% level of significance when assuming usual-OLS standard error remained statistically significant at 5% level of significance when assuming heteroscedasticity-robust standard error

Step 2 of 7

Step 3 of 7

Step 4 of 7

Step 5 of 7

Step 6 of 7

Step 7 of 7

Why don’t you like this exercise?

Other