Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010X(i) Use the data in HPRICE1.RAW to obtain the heteroskedasticity-robust standard errors for equation. Discuss any important differences with the usual standard errors.

(ii) Repeat part (i) for equation.

(iii) What does this example suggest about heteroskedasticity and the transformation used for the dependent variable?

Equation

Equation

Step 1 of 5

(i)

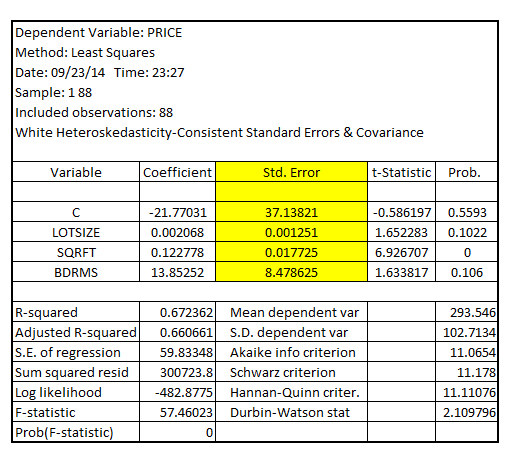

Estimating the model where  is regressed on

is regressed on such that the standard error of the coefficients of

such that the standard error of the coefficients of are heteroskedasticity-robust standard error, the result is as follows:

are heteroskedasticity-robust standard error, the result is as follows:

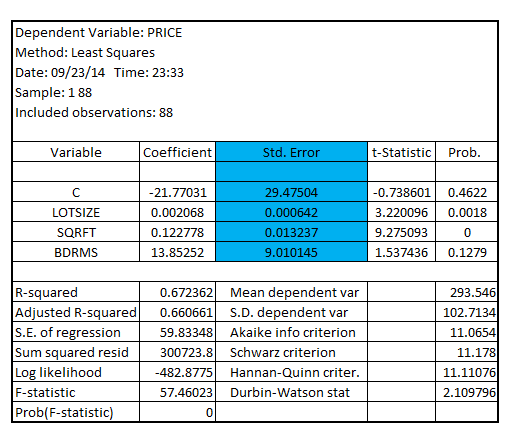

Estimate the model where  is regressed on

is regressed on such that the standard error of coefficients of

such that the standard error of coefficients of  are the usual OLS standard error, the result is as follows:

are the usual OLS standard error, the result is as follows:

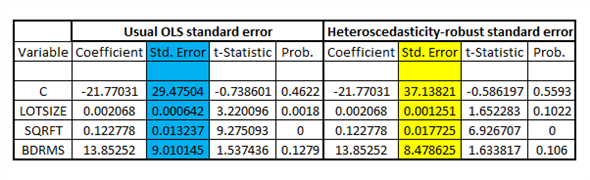

On comparing the usual OLS standard error with the heteroscedasticity-robust standard error, the result is as follows:

It shall be noted that the heteroscedasticity-robust standard error for the coefficient of  is 0.001251 whereas, the usual standard error is 0.000642. With usual standard error, the coefficient of

is 0.001251 whereas, the usual standard error is 0.000642. With usual standard error, the coefficient of  is significant with p-value 0.0018 whereas with heteroscedasticity-robust standard error, the coefficient of

is significant with p-value 0.0018 whereas with heteroscedasticity-robust standard error, the coefficient of  is insignificant at 5% level of significance

is insignificant at 5% level of significance

While the coefficient of  is with usual standard error of 0.013237, it is with heteroscedasticity-robust standard error of 0.017725

is with usual standard error of 0.013237, it is with heteroscedasticity-robust standard error of 0.017725

Similarly, the usual OLS standard error of the coefficient of  is 9.010145 which is higher than the heteroscedasticity-robust standard error at 8.478625

is 9.010145 which is higher than the heteroscedasticity-robust standard error at 8.478625

Step 2 of 5

Step 3 of 5

Step 4 of 5

Step 5 of 5

Why don’t you like this exercise?

Other