Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XLet ![Let <span class=sub>0</span> and <span class=sub>l</span> be the OLS intercept and slope estimators, respectively, and let u be the sample average of the errors (not the residuals!). <blockquote> (i) Show that B1 can be written as&= B1 + V. . w.u. where w. = d./SST and d. = x. — x. ==1 w . = 0, to show that B1 and u are uncorrelated. [Hint: You are being asked to show that E[(fi1 — B1) . u] = 0.] (iii) Show that B0 can be written as .w<span class=sub>i</span>u<span class=sub>i</span> where w<span class=sub>i</span>=d<span class=sub>i</span>/SST<span class=sub>X</span> and d<span class=sub>i</span>= x<span class=sub>i</span> - (iv) Use parts (i) along with to show that <span class=sub>1</span> and are uncorrelated. [Hint: You are being asked to show that (iii) show that <span class=sub>0</span> can be written as (iv). Use parts (ii) and (iii) to show that (v) Do the algebra to simplify the expression in part (iv) to equation (2.58). [Hint: </blockquote>](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/322bfacd_bd37_4070_b067_c593fadb7be1_SMCC2709_11.jpg) 0 and

0 and ![Let <span class=sub>0</span> and <span class=sub>l</span> be the OLS intercept and slope estimators, respectively, and let u be the sample average of the errors (not the residuals!). <blockquote> (i) Show that B1 can be written as&= B1 + V. . w.u. where w. = d./SST and d. = x. — x. ==1 w . = 0, to show that B1 and u are uncorrelated. [Hint: You are being asked to show that E[(fi1 — B1) . u] = 0.] (iii) Show that B0 can be written as .w<span class=sub>i</span>u<span class=sub>i</span> where w<span class=sub>i</span>=d<span class=sub>i</span>/SST<span class=sub>X</span> and d<span class=sub>i</span>= x<span class=sub>i</span> - (iv) Use parts (i) along with to show that <span class=sub>1</span> and are uncorrelated. [Hint: You are being asked to show that (iii) show that <span class=sub>0</span> can be written as (iv). Use parts (ii) and (iii) to show that (v) Do the algebra to simplify the expression in part (iv) to equation (2.58). [Hint: </blockquote>](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/3c0ce1cc_3ca8_4b2e_a1f1_df95b81a2c6f_SMCC2709_11.jpg) l be the OLS intercept and slope estimators, respectively, and let u be the sample average of the errors (not the residuals!).

l be the OLS intercept and slope estimators, respectively, and let u be the sample average of the errors (not the residuals!).

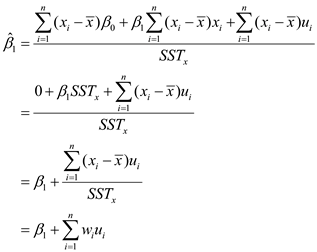

(i) Show that B1 can be written as&= B1 + V. . w.u. where w. = d./SST and d. = x. — x.

==1 w . = 0, to show that B1 and u are uncorrelated. [Hint: You are being asked to show that E[(fi1 — B1) . u] = 0.]

(iii) Show that B0 can be written as

.wiui where wi=di/SSTX and di= xi -

(iv) Use parts (i) along with

to show that

1 and

are uncorrelated. [Hint: You are being asked to show that

(iii) show that

0 can be written as

(iv). Use parts (ii) and (iii) to show that

(v) Do the algebra to simplify the expression in part (iv) to equation (2.58). [Hint:

![Let <span class=sub>0</span> and <span class=sub>l</span> be the OLS intercept and slope estimators, respectively, and let u be the sample average of the errors (not the residuals!). <blockquote> (i) Show that B1 can be written as&= B1 + V. . w.u. where w. = d./SST and d. = x. — x. ==1 w . = 0, to show that B1 and u are uncorrelated. [Hint: You are being asked to show that E[(fi1 — B1) . u] = 0.] (iii) Show that B0 can be written as .w<span class=sub>i</span>u<span class=sub>i</span> where w<span class=sub>i</span>=d<span class=sub>i</span>/SST<span class=sub>X</span> and d<span class=sub>i</span>= x<span class=sub>i</span> - (iv) Use parts (i) along with to show that <span class=sub>1</span> and are uncorrelated. [Hint: You are being asked to show that (iii) show that <span class=sub>0</span> can be written as (iv). Use parts (ii) and (iii) to show that (v) Do the algebra to simplify the expression in part (iv) to equation (2.58). [Hint: </blockquote>](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/5b7fa201_46f1_4dc6_8e2a_a4675a3fd158_SMCC2709_11.jpg)

![Let <span class=sub>0</span> and <span class=sub>l</span> be the OLS intercept and slope estimators, respectively, and let u be the sample average of the errors (not the residuals!). <blockquote> (i) Show that B1 can be written as&= B1 + V. . w.u. where w. = d./SST and d. = x. — x. ==1 w . = 0, to show that B1 and u are uncorrelated. [Hint: You are being asked to show that E[(fi1 — B1) . u] = 0.] (iii) Show that B0 can be written as .w<span class=sub>i</span>u<span class=sub>i</span> where w<span class=sub>i</span>=d<span class=sub>i</span>/SST<span class=sub>X</span> and d<span class=sub>i</span>= x<span class=sub>i</span> - (iv) Use parts (i) along with to show that <span class=sub>1</span> and are uncorrelated. [Hint: You are being asked to show that (iii) show that <span class=sub>0</span> can be written as (iv). Use parts (ii) and (iii) to show that (v) Do the algebra to simplify the expression in part (iv) to equation (2.58). [Hint: </blockquote>](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/aec66d6b_7535_4d3c_a14e_1a26a2adfe35_SMCC2709_11.jpg)

![Let <span class=sub>0</span> and <span class=sub>l</span> be the OLS intercept and slope estimators, respectively, and let u be the sample average of the errors (not the residuals!). <blockquote> (i) Show that B1 can be written as&= B1 + V. . w.u. where w. = d./SST and d. = x. — x. ==1 w . = 0, to show that B1 and u are uncorrelated. [Hint: You are being asked to show that E[(fi1 — B1) . u] = 0.] (iii) Show that B0 can be written as .w<span class=sub>i</span>u<span class=sub>i</span> where w<span class=sub>i</span>=d<span class=sub>i</span>/SST<span class=sub>X</span> and d<span class=sub>i</span>= x<span class=sub>i</span> - (iv) Use parts (i) along with to show that <span class=sub>1</span> and are uncorrelated. [Hint: You are being asked to show that (iii) show that <span class=sub>0</span> can be written as (iv). Use parts (ii) and (iii) to show that (v) Do the algebra to simplify the expression in part (iv) to equation (2.58). [Hint: </blockquote>](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/5404edbb_f9e7_4da0_8f76_99148ec7feb6_SMCC2709_11.jpg)

![Let <span class=sub>0</span> and <span class=sub>l</span> be the OLS intercept and slope estimators, respectively, and let u be the sample average of the errors (not the residuals!). <blockquote> (i) Show that B1 can be written as&= B1 + V. . w.u. where w. = d./SST and d. = x. — x. ==1 w . = 0, to show that B1 and u are uncorrelated. [Hint: You are being asked to show that E[(fi1 — B1) . u] = 0.] (iii) Show that B0 can be written as .w<span class=sub>i</span>u<span class=sub>i</span> where w<span class=sub>i</span>=d<span class=sub>i</span>/SST<span class=sub>X</span> and d<span class=sub>i</span>= x<span class=sub>i</span> - (iv) Use parts (i) along with to show that <span class=sub>1</span> and are uncorrelated. [Hint: You are being asked to show that (iii) show that <span class=sub>0</span> can be written as (iv). Use parts (ii) and (iii) to show that (v) Do the algebra to simplify the expression in part (iv) to equation (2.58). [Hint: </blockquote>](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/9360fa46_6068_4414_a97d_157a68f0d213_SMCC2709_11.jpg)

![Let <span class=sub>0</span> and <span class=sub>l</span> be the OLS intercept and slope estimators, respectively, and let u be the sample average of the errors (not the residuals!). <blockquote> (i) Show that B1 can be written as&= B1 + V. . w.u. where w. = d./SST and d. = x. — x. ==1 w . = 0, to show that B1 and u are uncorrelated. [Hint: You are being asked to show that E[(fi1 — B1) . u] = 0.] (iii) Show that B0 can be written as .w<span class=sub>i</span>u<span class=sub>i</span> where w<span class=sub>i</span>=d<span class=sub>i</span>/SST<span class=sub>X</span> and d<span class=sub>i</span>= x<span class=sub>i</span> - (iv) Use parts (i) along with to show that <span class=sub>1</span> and are uncorrelated. [Hint: You are being asked to show that (iii) show that <span class=sub>0</span> can be written as (iv). Use parts (ii) and (iii) to show that (v) Do the algebra to simplify the expression in part (iv) to equation (2.58). [Hint: </blockquote>](https://d2lvgg3v3hfg70.cloudfront.net/SMCC2709/909a51e5_07fa_4b04_b895_97c7b9a895e3_SMCC2709_11.jpg)

Step 1 of 7

Consider  are the OLS intercept and slope estimators respectively

are the OLS intercept and slope estimators respectively

Consider is the sample average of the errors

is the sample average of the errors

(i)

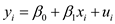

It shall be noted that in the population regression model is given by:

The sample regression model is given by:

Now, the estimate of  is given as:

is given as:

Since,

This implies

Where,

Step 2 of 7

Step 3 of 7

Step 4 of 7

Step 5 of 7

Step 6 of 7

Step 7 of 7

Why don’t you like this exercise?

Other