Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XConsider the standard simple regression model y = ?0 + ?1x + u under the Gauss-Markov Assumptions SLR.l through SLR.5. The usual OLS estimators 30 and J3X are unbiased for their respective population parameters. Let  1 be the estimator of ?1 obtained by assuming the intercept is zero (see Section 2.6).

1 be the estimator of ?1 obtained by assuming the intercept is zero (see Section 2.6).

(i) Find E(

1) in terms of the x, ?0, and ?1. Verify that

1 is unbiased for ?1 when the population intercept (?0) is zero. Are there other cases where ?1 is unbiased?

(ii) Find the variance of

1. (Hint: The variance does not depend on ?1.)

(iv)Comment on the trade off between bias and variance when choosing between

and

.

Step 1 of 3

i)

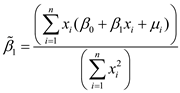

To show the unbiasedness of the regression coefficient, use the following formula for the estimator:

Substituting  gives

gives

Now, the numerator can be written as;

Finally,

Conditional on the xi, we then have,

Since, E(ui) = 0 for all I, therefore, the bias in  is given in the equation. The bias will be zero when

is given in the equation. The bias will be zero when  =0. It will also be zero when

=0. It will also be zero when  = 0. Meaning, regression through the origin is identical to regression with intercept.

= 0. Meaning, regression through the origin is identical to regression with intercept.

Step 2 of 3

Step 3 of 3

Why don’t you like this exercise?

Other