Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Sensitivity Analysis

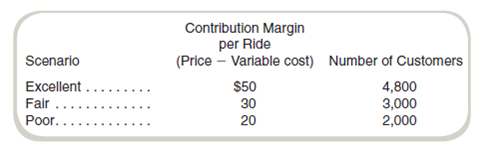

Bay Area Limos operates transportation services to Bay City airport. The price of service is fixed at a flat rate for each trip and most costs of providing the service are fixed for each trip. Betty Smith, the owner, forecasts income by estimating two factors that fluctuate with the economy: the fuel cost associated with the trip and the number of customers who would take trips. Looking at next year, Betty develops the following estimates of contribution margin (price less variable costs, including fuel) for the estimated number of customers. For simplicity, she assumes that the fuel costs (therefore the contribution margin per ride) and the number of customers are independent.

In addition to the costs of a ride, Betty estimates that other service costs are $45,000 plus $5 for each customer (ride) in excess of 3,000 rides. Annual administrative and marketing costs are estimated to be $20,000 plus 10 percent of the contribution margin.

Required

Use a spreadsheet to prepare an analysis of the possible operating income for Bay Area Limos similar to that in Exhibit 13.5. What is the range of possible operating incomes?

Step 1 of 4

Budget

Budgets are the estimates the company makes regarding its financial performance. At beginning of the year company estimates the revenue, expenses and based on it estimates its operating and net income. Based on the income statement it also determines its financial position. Thus, budgets are management estimates for the coming year. Budgets are prepared in order to allocate funds and for the managers to achieve the targets for coming year. At end of the year when the actuals are prepared company compares its budget with the actuals so as to analyze its performance in relation to the budget.

Step 2 of 4

Step 3 of 4

Step 4 of 4

Why don’t you like this exercise?

Other