Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Estimated Net Realizable Value and Effects of Processing Further

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of allocating joint production costs. Following is a summary of costs and other data for the quarter ended June 30.

No inventories were on hand at the beginning of the quarter. No raw material was on hand at June 30. All units on hand at the end of the quarter were fully complete as to processing.

Products | A | B | C |

Pounds sold | 20,000 | 59,000 | 70,000 |

Pounds on hand at June 30 | 50,000 | -0- | 40,000 |

Sales revenues | $45,000 | $265,500 | $367,500 |

Departments | X | Y | Z |

Raw material cost | $168,000 | $ -0- | $ -0- |

Direct labor cost | 72,000 | 121,350 | 287,625 |

Manufacturing overhead | 30,000 | 31,650 | 109,875 |

Required

a. Determine the following amounts for each product: (1) estimated net realizable value used for allocating joint costs, (2) joint costs allocated to each of the three products, (3) cost of goods sold, and (4) finished goods inventory costs, June 30.

b. Assume that the entire output of product A could be processed further at an additional cost of $6.00 per pound and then sold for $12.90 per pound. What would have been the effect on operating profits if all of product A output for the quarter had been further processed and then sold rather than being sold at the split-off point?

c. Write a memo to management indicating whether the company should process product A further and why.

Step 1 of 5

a.

? |

| Departments | ||||

| Production Costs | X |

| Y |

| Z |

| Raw materials? | $168,000 |

| — |

| — |

| Direct labor? | 72,000 |

| $121,350 |

| $ 287,625 |

| Manufacturing overhead? | 30,000 |

| 31,650 |

| 109,875 |

| Total? | $270,000 |

| $153,000 |

| $397,500 |

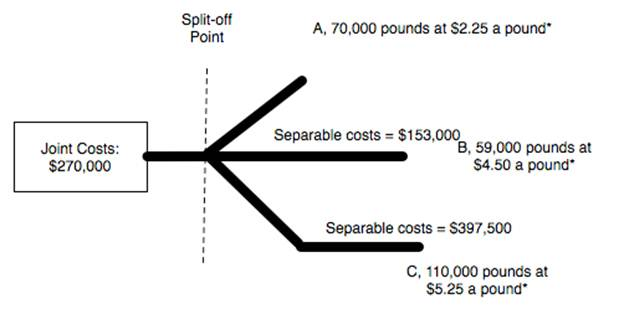

?A diagram of the problem follows:

*$2.25 = $45,000 ÷ 20,000 lbs; $4.50 = $265,500 ÷ 59,000 lbs;

$5.25 = $367,500 ÷ 70,000 lbs.

|

| Product A |

| Product B |

| Product C |

| Total |

1. | Selling price per pound: |

|

|

|

|

|

|

|

| ?X: $45,000 ¸ 20,000? | $2.25 |

|

|

|

|

|

|

| ?Z: $367,500 ¸ 70,000? |

|

|

|

| $5.25 |

|

|

| Multiply by pounds produced: |

|

|

|

|

|

| |

| ?A: 20,000 + 50,000? | x 70,000 |

|

|

|

|

|

|

| ?C: 70,000 + 40,000? | ?? |

| ?? |

| x 110,000 |

|

|

| Gross sales values? | $157,500 |

| $265,500a |

| $577,500b |

|

|

| Less costs of separate processing: |

|

|

|

|

|

| |

| ?A: —? | — |

| — |

| — |

|

|

| ?B: $121,350 + $31,650? | — |

| 153,000 |

| — |

|

|

| ?C: $287,625 + $109,875? | — |

| — |

| 397,500 |

|

|

| Estimated net realizable values at split-off point? | $157,500 |

| $ 112,500 |

| $180,000 |

| $450,000 |

| Percentage of total? | 35% |

| 25% |

| 40% |

| 100% |

a Given

b Or: $367,500 | x | (110,000 ÷ 70,000) | = | $577,500 |

Step 2 of 5

Step 3 of 5

Step 4 of 5

Step 5 of 5

Why don’t you like this exercise?

Other