Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

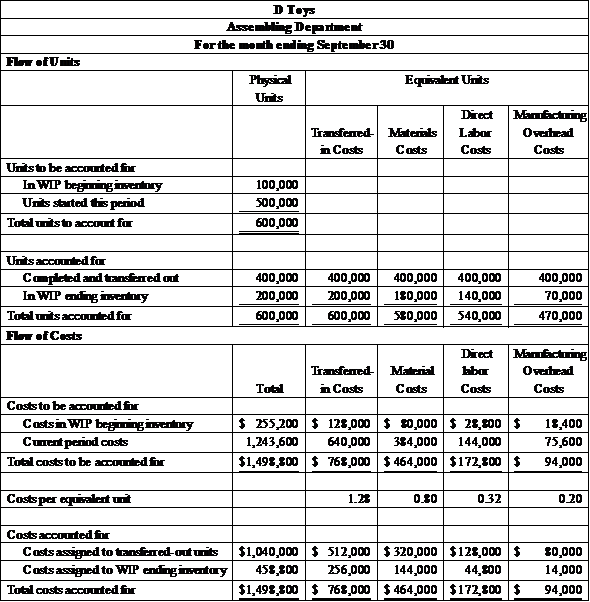

Edition 3ISBN: 0073527114Prepare a Production Cost Report: Weighted-Average Method

Douglas Toys is a manufacturer that uses the weighted-average process costing method to account for costs of production. It produces a plastic toy in three separate departments: Molding, Assembling, and Finishing. The following information was obtained for the Assembling Department for the month of September.

Work in process on September 1 had 100,000 units made up of the following:

|

| Degree of |

| Amount | Completion |

Prior department costs transferred in from the Molding Department. | $128,000 | 100% |

Costs added by the Assembling Department |

|

|

Direct materials | 80,000 | 100% |

Direct labor | 28,800 | 60% |

Manufacturing overhead | 18,400 $127,200 | 50% |

Work in process, September 1 | $255,200 |

|

During September, 500,000 units were transferred in from the Molding Department at a cost of $640,000. The Assembling Department added the following costs:

Direct materials | $384,000 |

Direct labor | 144 000 |

Manufacturing overhead | 75,600 |

Total costs added | $603,600 |

Assembling finished 400,000 units and transferred them to the Finishing Department.

At September 30, 200,000 units were still in work-in-process inventory. The degree of completion of work-in-process inventory at September 30 was as follows:

Direct materials | 90% |

Direct labor | 70 |

Manufacturing overhead | 35 |

Required

a.Prepare a production cost report using the weighted-average method.

b.Management would like to decrease the costs of manufacturing the toy. In particular, it has set the following per unit targets for this product in the Assembling Department: Materials, $0.80; labor, $0.40; and manufacturing overhead, $0.18. Has the product achieved management’s cost targets in the Assembling Department? Write a short report to management stating your answer(s).

Step 1 of 2

(a)

The required production cost report should be prepared in the following manner:

Working notes:

1. Work-in-process ending inventory is 90% complete for materials, 70% complete for direct labor, and 35% complete for manufacturing overheads. Therefore, equivalent units of work-in-process ending inventory for materials is 180,000 , for direct labor is 140,000

, for direct labor is 140,000 , and for manufacturing overheads is 70,000

, and for manufacturing overheads is 70,000 .

.

2. Cost per equivalent unit for each item has been computed by dividing total cost to be accounted for by total units to be accounted for.

3. Costs assigned to work-in-process ending inventory for each item has been computed by multiplying equivalent units by cost per equivalent unit.

Step 2 of 2

Why don’t you like this exercise?

Other