Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Extensions of the CVP Model—Taxes

Odd Wallow Drinks is considering adding a new line of fruit juices to its merchandise products. This line of juices has the following prices and costs:

Selling price per case (24 bottles) of juice | $ 50 |

Variable cost per case (24 bottles) of juice | $ 24 |

Fixed costs per year associated with | |

this product | $8,112,000 |

Income tax rate | 40% |

Required

a. Compute Odd Wallow Drinks’s break-even point in units per year.

b. How many cases must Odd Wallow Drinks sell to earn $1,872,000 per year after taxes on the juice?

Step 1 of 2

a.

Break-even point (in units)

Break-even point is the level of operations at which the sales revenue and total costs (variable costs and fixed costs) become equal. There is no profit or no loss at break-even point sales.

Break-even point (in units) can be calculated using the following equation

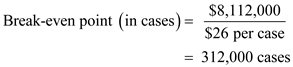

Selling price is $50 per case of juice and variable cost is $24 per case of juice. The yearly fixed costs are $8,112,000

Contribution margin is the profit earned by the company before adjusting for the fixed costs.

Now we calculate the break-even point (in cases) as follows:

The company’s break-even point (in cases of juice) is 312,000 cases.

Break-even point (in bottles)

Each case of juice has 24 bottles.

Therefore, break-even point in cases is 7,488,000 bottles.

Step 2 of 2

Why don’t you like this exercise?

Other