Accounting: What the Numbers Mean 9th Edition by Wayne W McManus, Daniel F Viele, David H Marshall

Edition 9ISBN: 0073527068Accounting: What the Numbers Mean 9th Edition by Wayne W McManus, Daniel F Viele, David H Marshall

Edition 9ISBN: 0073527068Record transactions and adjustments Prepare an answer sheet with the column headings shown after the following list of transactions. Record the effect, if any, of the transaction entry or adjusting entry on the appropriate balance sheet category or on the income statement by entering the account name and amount and indicating whether it is an addition ( + ) or subtraction (-). Column headings reflect the expanded balance sheet equation; items that affect net income should not be shown as affecting owners’ equity. The first transaction is provided as an illustration.

(Note: As an alternative to using the columns, you may write the journal entry for each transaction or adjustment.)

a. During the month, Supplies Expense was debited $2,600 for supplies purchased. The cost of supplies used during the month was $1,900. Record the adjustment to properly reflect the amount of supplies used and supplies still on hand at the end of the month.

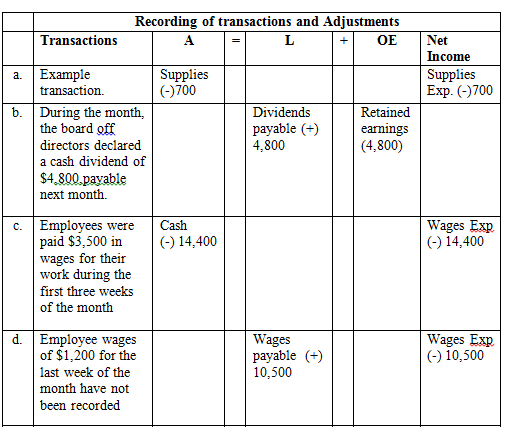

b. During the month, the board of directors declared a cash dividend of $4,800, payable next month.

c. Employees were paid $3,500 in wages for their work during the first three weeks of the month.

d. Employee wages of $1,200 for the last week of the month have not been recorded.

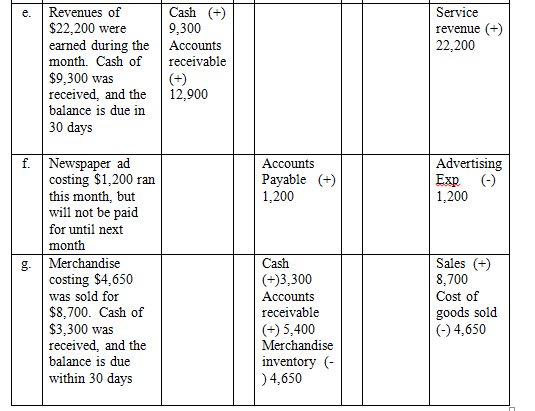

e. Revenues from services performed during the month totaled $7,400. Of this amount, $3,100 was received in cash and the balance is expected to be received within 30 days.

f. A contract was signed with a newspaper for a $400 advertisement; the ad ran during this month but will not be paid for until next month.

g. Merchandise that cost $1,550 was sold for $2,900. Of this amount, $1,100 was received in cash and the balance is expected to be received within 30 days.

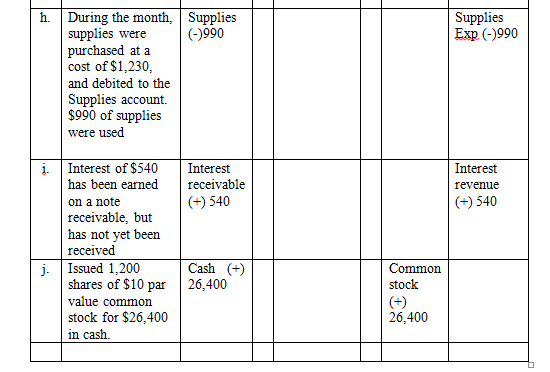

h. Independent of transaction a, assume that during the month, supplies were purchased at a cost of $410 and debited to the Supplies (asset) account. A total of $330 of supplies were used during the month. Record the adjustment to properly reflect the amount of supplies used and supplies still on hand at the end of the month.

i. Interest of $180 has been earned on a note receivable but has not yet been received.

j. Issued 400 shares of $10 par value common stock for $8,800 in cash.

Transaction / Situation | Assets | Liabilities | Owners’ Equity | Net Income |

a. | Supplies +700 |

|

| Supplies Exp. +700 |

|

|

| (Note: A decrease to Supplies Expense increases Net Income.) |

Step 1 of 2

The recording of transactions and adjustments into financial statements is as follows:

Record Journal entries:

The journal entries for the given transactions are recorded in the table below. The normal balance for assets and expenses are debits and the normal balance for liabilities and stockholders’ equity accounts are credits. This means that debits debit the balance for assets and expenses and credits debit the balance for liabilities and stockholders’ equity. Revenues and paid-in capital are considered stockholders’ equity account. Notes payable and accounts payable are considered liability accounts. Cash, equipment, supplies and accounts receivable are considered assets accounts.

As an alternative to columns, the journal writings for the presented transactions are as follows:

Step 2 of 2

Why don’t you like this exercise?

Other