Deck 12: Managing and Reporting Performance

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

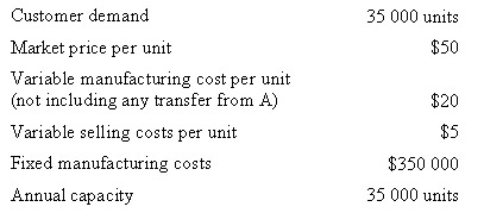

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assuming the Milling Division manager agrees to the special offer,what is the effect of the decision on the gross margin of Weber as a whole?

A) $20 000 decrease

B) $50 000 decrease

C) $30 000 increase

D) $50 000 increase

A) $20 000 decrease

B) $50 000 decrease

C) $30 000 increase

D) $50 000 increase

Question

Question

Question

Question

Question

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assume the company permits the division managers to negotiate a transfer price.The managers agree to a $15 transfer price adjusted to share equally the additional gross margin to Milling Division resulting from the sale to the Products Division.What is the agreed transfer price?

A) $14.00

B) $13.50

C) $12.50

D) $10.50

A) $14.00

B) $13.50

C) $12.50

D) $10.50

Question

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.00.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assume that demand increases for the Milling Division.All 25 000 units can be sold at the regular price to outside customers and the Product Division's annual demand declines to 5 000 units.What transfer price would be calculated under the general transfer-pricing formula?

A) $18.00

B) $17.00

C) $16.00

D) $10.00

A) $18.00

B) $17.00

C) $16.00

D) $10.00

Question

Question

Question

Question

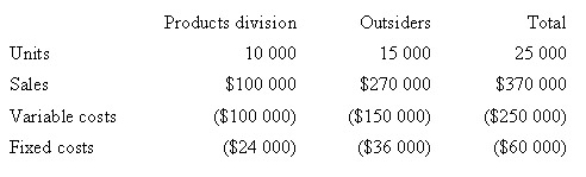

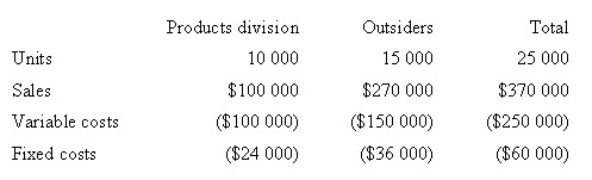

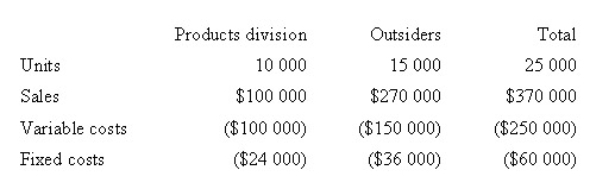

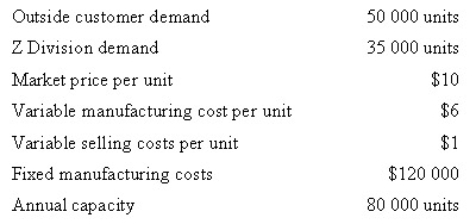

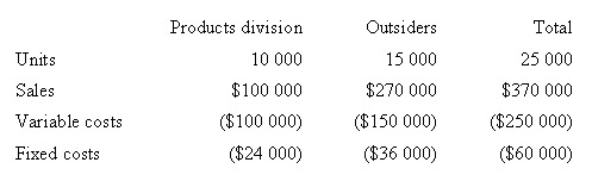

Barrister Company has two divisions: A and Z.The A Division produces a single product that can be sold to outside customers or to the Z Division.Sales forecasts,production statistics and costs for both divisions for 2008 are shown below:

A Division:

Z Division:

* When A Division sells to Z Division,no variable selling costs are incurred by A Division.Calculate the minimum per unit transfer price that A Division should charge Z Division in 2008,using the general transfer-pricing formula.

A) $6.00

B) $8.50

C) $7.26

D) None of the given answers

A Division:

Z Division:

* When A Division sells to Z Division,no variable selling costs are incurred by A Division.Calculate the minimum per unit transfer price that A Division should charge Z Division in 2008,using the general transfer-pricing formula.

A) $6.00

B) $8.50

C) $7.26

D) None of the given answers

Question

Question

Question

Question

Question

Question

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assume that demand increases for the Milling Division.20 000 units can be sold at the regular price to outside customers and the Products Division's annual demand remains at 10 000 units.What is the transfer price that would be calculated under the general transfer-pricing formula?

A) $12.00

B) $14.00

C) $16.00

D) $18.00

A) $12.00

B) $14.00

C) $16.00

D) $18.00

Question

Question

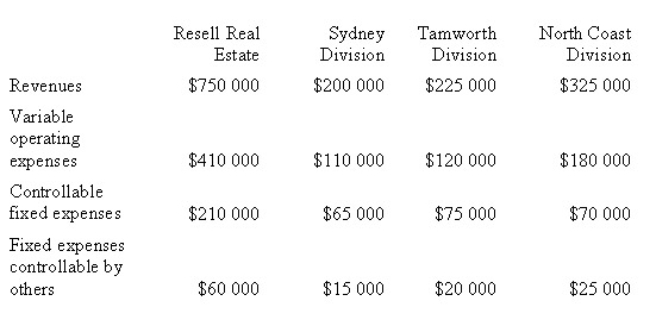

The following information was taken from the business united profit and loss statement of Resell Real Estate Agents for 2008:

In addition,the company incurred common fixed costs of $18 000.What was the business unit margin of the Tamworth Division during 2008?

A) ($8000)

B) $4000

C) $10 000

D) $30 000

In addition,the company incurred common fixed costs of $18 000.What was the business unit margin of the Tamworth Division during 2008?

A) ($8000)

B) $4000

C) $10 000

D) $30 000

Question

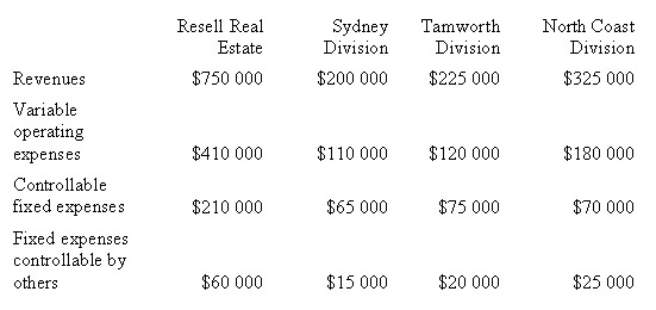

The following information was taken from the business united profit and loss statement of Resell Real Estate Agents for 2008:

In addition,the company incurred common fixed costs of $18 000.Which amount should be used to evaluate the Sydney Division as an investment of the company?

A) $25 000

B) $10 000

C) $4000

D) ($8000)

In addition,the company incurred common fixed costs of $18 000.Which amount should be used to evaluate the Sydney Division as an investment of the company?

A) $25 000

B) $10 000

C) $4000

D) ($8000)

Question

Question

Question

Question

Question

Question

Question

Question

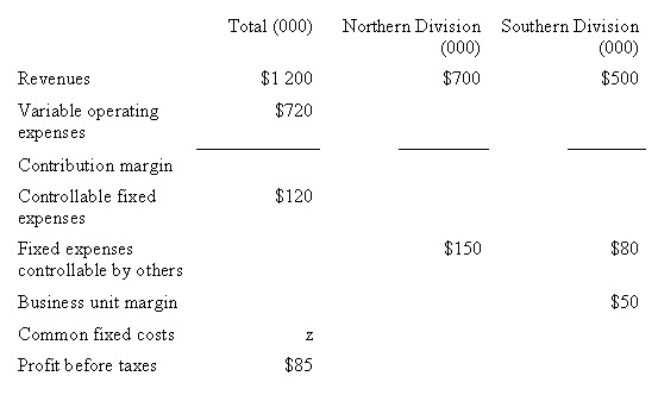

Callahan Company consists of two divisions,Northern and Southern.During 2008,many of the accounting records were destroyed in a fire.The managing director has asked the accountant for information relating to 2008.The following information is available to the accountant.In addition,the contribution margin ratio for both divisions was the same.What were the common fixed costs (z)during 2008?

A) $130 000

B) $45 000

C) $70 000

D) $65 000

A) $130 000

B) $45 000

C) $70 000

D) $65 000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/88

Play

Full screen (f)

Deck 12: Managing and Reporting Performance

1

Responsibility accounting:

A) fosters goal congruence

B) involves using the various concepts and tools used by management accountants for planning and control

C) is used to measure the performance of subunits

D) All of the given answers

A) fosters goal congruence

B) involves using the various concepts and tools used by management accountants for planning and control

C) is used to measure the performance of subunits

D) All of the given answers

D

2

Which of the following managers is held accountable for only the revenue attributed to a subunit?

A) Cost centre manager

B) Revenue centre manager

C) Sales manager

D) Investment centre manager

A) Cost centre manager

B) Revenue centre manager

C) Sales manager

D) Investment centre manager

B

3

An opportunity cost can best be described as the:

A) pricing of goods as per market trends

B) direct expenses incurred in producing goods

C) total difference in cost of production between two divisions

D) the benefit that is foregone for one alternative in order to pursue another alternative

A) pricing of goods as per market trends

B) direct expenses incurred in producing goods

C) total difference in cost of production between two divisions

D) the benefit that is foregone for one alternative in order to pursue another alternative

D

4

Which of the following statements is/are false?

A) Goal congruence is difficult to achieve because managers are often unaware of the effects of their decisions on the organisation's subunits.

B) The development of performance measures to evaluate a subunit and its managers will help achieve goal congruence.

C) People are naturally concerned with the performance of all subunits within the organisation.

D) Goal congruence can be achieved by having a reward system tied to a manager's performance.

A) Goal congruence is difficult to achieve because managers are often unaware of the effects of their decisions on the organisation's subunits.

B) The development of performance measures to evaluate a subunit and its managers will help achieve goal congruence.

C) People are naturally concerned with the performance of all subunits within the organisation.

D) Goal congruence can be achieved by having a reward system tied to a manager's performance.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

5

An example of a profit centre is the:

A) painting department

B) sales department

C) company-owned restaurant in a fast-food chain

D) All of the given answers

A) painting department

B) sales department

C) company-owned restaurant in a fast-food chain

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

6

What is a negative consequence of decentralisation?

A) Narrow focus

B) Services may be duplicated

C) Suboptimal decisions may be made

D) All of the given answers

A) Narrow focus

B) Services may be duplicated

C) Suboptimal decisions may be made

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

7

Fragrance Pty Ltd has two divisions: the Cologne Division and the Bottle Division.The company is decentralised and each division is evaluated as a profit centre.The Bottle Division produces bottles that can be used by the Cologne Division.The Bottle Division's variable manufacturing cost per unit is $2.00 and shipping costs are $0.10 per unit.The Bottle Division's external sales price is $3.00 per unit.No shipping costs are incurred on sales to the Cologne Division.The Cologne Division can purchase similar bottles in the external market for $2.50.Assume the Bottle Division has no excess capacity and can sell everything produced externally.What is the maximum amount Cologne Division would be willing to pay for the bottles?

A) $2.00

B) $2.10

C) $2.50

D) $2.90

A) $2.00

B) $2.10

C) $2.50

D) $2.90

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following is not an example of a responsibility centre?

A) Corporate centre

B) Revenue centre

C) Profit centre

D) Investment centre

A) Corporate centre

B) Revenue centre

C) Profit centre

D) Investment centre

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

9

A sales department manager is an example of a:

A) cost centre manager

B) revenue centre manager

C) profit centre manager

D) investment centre manager

A) cost centre manager

B) revenue centre manager

C) profit centre manager

D) investment centre manager

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

10

The biggest challenge in making a decentralised organisation function effectively is:

A) to earn maximum profits through fair practices

B) to minimise organisational losses

C) taking advantage of the specialised knowledge and skills of a manager

D) obtaining goal congruence among the organisation's autonomous managers

A) to earn maximum profits through fair practices

B) to minimise organisational losses

C) taking advantage of the specialised knowledge and skills of a manager

D) obtaining goal congruence among the organisation's autonomous managers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following managers is held accountable for the profit of the subunit?

A) Revenue centre manager

B) Profit centre manager

C) Investment centre manager

D) Both B and C

A) Revenue centre manager

B) Profit centre manager

C) Investment centre manager

D) Both B and C

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following managers is held accountable for the subunit's profit and invested capital?

A) Investment centre manager

B) Revenue centre manager

C) Profit centre manager

D) Sales manager

A) Investment centre manager

B) Revenue centre manager

C) Profit centre manager

D) Sales manager

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

13

Delegating decision making to lower-level managers,thereby enabling an organisation to react quickly to opportunities and problems as they arise,is a characteristic of:

A) a decentralised organisation

B) a centralised organisation

C) a corporation

D) responsibility accounting

A) a decentralised organisation

B) a centralised organisation

C) a corporation

D) responsibility accounting

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

14

When managers within the various subunits of an organisation are committed to achieving the goals set by top management,the result is:

A) goal congruence

B) planning and control

C) responsibility accounting

D) delegation of decision making

A) goal congruence

B) planning and control

C) responsibility accounting

D) delegation of decision making

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

15

The amount charged when one business unit sells goods or services to another business unit is called a(n):

A) opportunity cost

B) transfer price

C) standard variable cost

D) residual price

A) opportunity cost

B) transfer price

C) standard variable cost

D) residual price

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following statements about transfer prices is/are true?

I)When the producing division has excess capacity and the external market is imperfectly competitive,the general transfer-pricing rule and the external market price will be the same

Ii)If the transfer price is set at the market price,the supplying division will be indifferent to selling internally or externally.

Iii)If the transfer price is set at the market price,the buying division will usually purchase goods from inside its organisation,if product specifications are met.

A) i and ii

B) ii and iii

C) i and iii

D) All of the given answers

I)When the producing division has excess capacity and the external market is imperfectly competitive,the general transfer-pricing rule and the external market price will be the same

Ii)If the transfer price is set at the market price,the supplying division will be indifferent to selling internally or externally.

Iii)If the transfer price is set at the market price,the buying division will usually purchase goods from inside its organisation,if product specifications are met.

A) i and ii

B) ii and iii

C) i and iii

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

17

Fragrance Pty Ltd has two divisions: the Cologne Division and the Bottle Division.The company is decentralised and each division is evaluated as a profit centre.The Bottle Division produces bottles that can be used by the Cologne Division.The Bottle Division's variable manufacturing cost per unit is $2.00 and shipping costs are $0.10 per unit.The Bottle Division's external sales price is $3.00 per unit.No shipping costs are incurred on sales to the Cologne Division.The Cologne Division can purchase similar bottles in the external market for $2.50.The Bottle Division has sufficient capacity to meet all external market demands in addition to meeting the demands of the Cologne Division.Using the general rule,the minimum transfer price from the Bottle Division to the Cologne Division would be:

A) $2.00

B) $2.10

C) $2.50

D) $2.90

A) $2.00

B) $2.10

C) $2.50

D) $2.90

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is not a benefit of decentralisation?

A) Specialised information about the local markets

B) Motivation

C) Relief to upper-level management

D) Narrow focus on the manager's own subunit

A) Specialised information about the local markets

B) Motivation

C) Relief to upper-level management

D) Narrow focus on the manager's own subunit

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following managers is held responsible for only the costs incurred in the subunit?

A) Cost centre manager

B) Revenue centre manager

C) Profit centre manager

D) Investment centre manager

A) Cost centre manager

B) Revenue centre manager

C) Profit centre manager

D) Investment centre manager

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

20

Fragrance Pty Ltd has two divisions: the Cologne Division and the Bottle Division.The company is decentralised and each division is evaluated as a profit centre.The Bottle Division produces bottles that can be used by the Cologne Division.The Bottle Division's variable manufacturing cost per unit is $2.00 and shipping costs are $0.10 per unit.The Bottle Division's external sales price is $3.00 per unit.No shipping costs are incurred on sales to the Cologne Division.The Cologne Division can purchase similar bottles in the external market for $2.50.Assume the Bottle Division has no excess capacity and can sell everything produced externally.Using the general rule,the transfer price from the Bottle Division to the Cologne Division would be:

A) $2.10

B) $2.50

C) $2.90

D) $3.00

A) $2.10

B) $2.50

C) $2.90

D) $3.00

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

21

Nova Company has two divisions: OPA Division and LPA Division.The OPA Division manufactures a single product,presently operates at 95 per cent of full capacity (100 000 units)and can sell all 95 000 units produced to outside customers.This product is also a component used in a product made by the LPA Division.OPA's full cost of production is $22.50 per unit,including $4.50 of applied fixed overhead costs.The applied fixed overhead is calculated based upon production of 95 000 units.OPA's management believes that production can be raised to 100 000 units without affecting cost behaviour.OPA's selling price per unit is $30 with a 10 per cent sales commission on outside sales.LPA is presently negotiating the purchase of units from OPA.LPA can purchase a comparable component outside for $29.What is the minimum acceptable transfer price for the first 5000 units from the viewpoint of OPA's management?

A) $18.00

B) $22.00

C) $27.00

D) $27.80

A) $18.00

B) $22.00

C) $27.00

D) $27.80

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements about the general transfer-pricing rule is/are true?

I)When the producing division has excess capacity,the transfer decision should be based on the outlay cost

Ii)When the producing division has no excess capacity,the opportunity cost is the foregone contribution from the lost sale.

Iii)If the producing division has excess capacity or the external market is imperfectly competitive,the general rule and the external market price will not yield the same transfer price.

A) i

B) ii

C) ii and iii

D) All of the given answers

I)When the producing division has excess capacity,the transfer decision should be based on the outlay cost

Ii)When the producing division has no excess capacity,the opportunity cost is the foregone contribution from the lost sale.

Iii)If the producing division has excess capacity or the external market is imperfectly competitive,the general rule and the external market price will not yield the same transfer price.

A) i

B) ii

C) ii and iii

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is usually achieved when the general transfer-pricing rule is implemented?

A) Harmony

B) Perfect competition

C) Goal congruence

D) Cost measurement

A) Harmony

B) Perfect competition

C) Goal congruence

D) Cost measurement

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

24

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assuming the Milling Division manager agrees to the special offer,what is the effect of the decision on the gross margin of Weber as a whole?

A) $20 000 decrease

B) $50 000 decrease

C) $30 000 increase

D) $50 000 increase

A) $20 000 decrease

B) $50 000 decrease

C) $30 000 increase

D) $50 000 increase

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

25

Symonds Bendigo Division purchases from an outside supplier for $52 per unit.The company's Ballarat Division,which has no excess capacity,makes and sells the same part for external customers at a variable cost of $38 and a selling price of $58.If Ballarat commences sales to Bendigo it will (1)use the general rule and (2)be able to reduce the variable cost on internal transfers by $4.If external sales are not affected,Ballarat should establish a transfer price of:

A) $34

B) $38

C) $54

D) $58

A) $34

B) $38

C) $54

D) $58

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

26

Hamilton has no excess capacity.If the company wishes to implement the general transfer-pricing rule,the opportunity cost would be equal to:

A) zero

B) the direct expenses incurred in producing the goods

C) the total difference in the cost of production between two divisions

D) the contribution foregone from the lost external sale

A) zero

B) the direct expenses incurred in producing the goods

C) the total difference in the cost of production between two divisions

D) the contribution foregone from the lost external sale

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

27

Polly Woodside Maritime Division purchases from an outside supplier for $52 per unit.The company's Shore Division,which has excess capacity,makes and sells the same part for external customers at a variable cost of $38 and a selling price of $58.If Shore Division commences sales to Maritime Division it will (1)use the general rule and (2)be able to reduce the variable cost on internal transfers by $4.If external sales are not affected,Shore Division should establish a transfer price of:

A) $34

B) $38

C) $58

D) None of the given answers

A) $34

B) $38

C) $58

D) None of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following statements is false,with respect to a negotiated transfer price?

A) The profit of each division will depend on the negotiating skills of the managers.

B) The process always results in a spirit of cooperation and unity that is desirable throughout an organisation.

C) The market price is usually the base line for negotiations.

D) Negotiations can lead to divisiveness and competition between participating business unit managers.

A) The profit of each division will depend on the negotiating skills of the managers.

B) The process always results in a spirit of cooperation and unity that is desirable throughout an organisation.

C) The market price is usually the base line for negotiations.

D) Negotiations can lead to divisiveness and competition between participating business unit managers.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

29

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assume the company permits the division managers to negotiate a transfer price.The managers agree to a $15 transfer price adjusted to share equally the additional gross margin to Milling Division resulting from the sale to the Products Division.What is the agreed transfer price?

A) $14.00

B) $13.50

C) $12.50

D) $10.50

A) $14.00

B) $13.50

C) $12.50

D) $10.50

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

30

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.00.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assume that demand increases for the Milling Division.All 25 000 units can be sold at the regular price to outside customers and the Product Division's annual demand declines to 5 000 units.What transfer price would be calculated under the general transfer-pricing formula?

A) $18.00

B) $17.00

C) $16.00

D) $10.00

A) $18.00

B) $17.00

C) $16.00

D) $10.00

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following statements is/are true?

When a multinational company transfers goods or services between business units located in different countries:

I)the tax rates of the different countries will have no effect on overall company profits

Ii)the result is a moving of profits from one country to another.

Iii)the company will consider the tax rates of the different countries when determining the transfer price.

A) i

B) ii

C) i and ii

D) ii and iii

When a multinational company transfers goods or services between business units located in different countries:

I)the tax rates of the different countries will have no effect on overall company profits

Ii)the result is a moving of profits from one country to another.

Iii)the company will consider the tax rates of the different countries when determining the transfer price.

A) i

B) ii

C) i and ii

D) ii and iii

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

32

Transfer prices should not be based on actual costs because:

A) inefficient producing divisions have higher costs of production,which would be passed on by buying divisions.

B) producing divisions have no incentives to control costs.

C) inefficient units with high costs of production have no opportunity for profit.

D) inefficient producing divisions have higher costs of production,which would be passed on by buying divisions AND producing divisions have no incentives to control costs.

A) inefficient producing divisions have higher costs of production,which would be passed on by buying divisions.

B) producing divisions have no incentives to control costs.

C) inefficient units with high costs of production have no opportunity for profit.

D) inefficient producing divisions have higher costs of production,which would be passed on by buying divisions AND producing divisions have no incentives to control costs.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following statements about transfer pricing is/are true?

I)Income taxes and import duties are an important consideration when setting a transfer price for international companies

Ii)Transfer prices cannot be used by organisations in a service industry.

Iii)Transfer prices are totally cost based and not market based.

A) i

B) ii

C) i and ii

D) All of the given answers

I)Income taxes and import duties are an important consideration when setting a transfer price for international companies

Ii)Transfer prices cannot be used by organisations in a service industry.

Iii)Transfer prices are totally cost based and not market based.

A) i

B) ii

C) i and ii

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

34

Barrister Company has two divisions: A and Z.The A Division produces a single product that can be sold to outside customers or to the Z Division.Sales forecasts,production statistics and costs for both divisions for 2008 are shown below:

A Division:

Z Division:

* When A Division sells to Z Division,no variable selling costs are incurred by A Division.Calculate the minimum per unit transfer price that A Division should charge Z Division in 2008,using the general transfer-pricing formula.

A) $6.00

B) $8.50

C) $7.26

D) None of the given answers

A Division:

Z Division:

* When A Division sells to Z Division,no variable selling costs are incurred by A Division.Calculate the minimum per unit transfer price that A Division should charge Z Division in 2008,using the general transfer-pricing formula.

A) $6.00

B) $8.50

C) $7.26

D) None of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

35

Transfer prices should not be based on absorption costs as this could result in suboptimal decisions by the:

A) personnel division.

B) competitive market.

C) buying division.

D) selling division.

A) personnel division.

B) competitive market.

C) buying division.

D) selling division.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

36

Division A transfers a profitable subassembly to Division B,where it is assembled into a final product.Division A is located in New Zealand,which has a high tax rate.Division B is located in Thailand,which has a low tax rate.Ideally, (1)which type of before tax income should each division report from the transfer and (2)what type of transfer price should be set for the subassembly?

Division A

Division B

Division C

Income

Income

Price

A) low

Low

Low

B) low

High

Low

C) low

High

High

D) high

Low

High

Division A

Division B

Division C

Income

Income

Price

A) low

Low

Low

B) low

High

Low

C) low

High

High

D) high

Low

High

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

37

Nova Company has two divisions: OPA Division and LPA Division.The OPA Division manufactures a single product,presently operates at 95 per cent of full capacity (100 000 units)and can sell all 95 000 units produced to outside customers.This product is also a component used in a product made by the LPA Division.OPA's full cost of production is $22.50 per unit,including $4.50 of applied fixed overhead costs.The applied fixed overhead is calculated based on production of 95 000 units.OPA's management believes that production can be raised to 100 000 units without affecting cost behaviour.OPA's selling price per unit is $30 with a 10 per cent sales commission on outside sales.LPA is presently negotiating the purchase of units from OPA.LPA can purchase a comparable component outside for $29.Using the general transfer-pricing formula,calculate a transfer price for 5000 units that would be in the best interests of the company as a whole.

A) $18.00

B) $22.50

C) $27.80

D) $29.00

A) $18.00

B) $22.50

C) $27.80

D) $29.00

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

38

Hamilton has excess capacity.If the company wishes to implement the general transfer-pricing rule,the opportunity cost would be equal to:

A) zero

B) the direct expenses incurred in producing the goods

C) the total difference in the cost of production between two divisions

D) the sum of the variable cost plus the fixed cost

A) zero

B) the direct expenses incurred in producing the goods

C) the total difference in the cost of production between two divisions

D) the sum of the variable cost plus the fixed cost

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following statements about cost-based transfer prices is/are true?

I)A transfer price set at standard variable cost plus a mark-up provides an incentive for the supplying business to make the transfer

Ii)Absorption cost-based transfer prices are good for the company as a whole because all costs are considered.

Iii)Transfer prices should be based on standard costs rather than actual costs since the cost of inefficiency should not be passed on.

A) i and ii

B) ii and iii

C) i and iii

D) All of the given answers

I)A transfer price set at standard variable cost plus a mark-up provides an incentive for the supplying business to make the transfer

Ii)Absorption cost-based transfer prices are good for the company as a whole because all costs are considered.

Iii)Transfer prices should be based on standard costs rather than actual costs since the cost of inefficiency should not be passed on.

A) i and ii

B) ii and iii

C) i and iii

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

40

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assume that demand increases for the Milling Division.20 000 units can be sold at the regular price to outside customers and the Products Division's annual demand remains at 10 000 units.What is the transfer price that would be calculated under the general transfer-pricing formula?

A) $12.00

B) $14.00

C) $16.00

D) $18.00

A) $12.00

B) $14.00

C) $16.00

D) $18.00

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

41

The budgeted and actual amount of a responsibility centre's key financial results are shown on a:

A) responsibility report

B) variance report

C) variable cost report

D) performance report

A) responsibility report

B) variance report

C) variable cost report

D) performance report

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

42

The following information was taken from the business united profit and loss statement of Resell Real Estate Agents for 2008:

In addition,the company incurred common fixed costs of $18 000.What was the business unit margin of the Tamworth Division during 2008?

A) ($8000)

B) $4000

C) $10 000

D) $30 000

In addition,the company incurred common fixed costs of $18 000.What was the business unit margin of the Tamworth Division during 2008?

A) ($8000)

B) $4000

C) $10 000

D) $30 000

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

43

The following information was taken from the business united profit and loss statement of Resell Real Estate Agents for 2008:

In addition,the company incurred common fixed costs of $18 000.Which amount should be used to evaluate the Sydney Division as an investment of the company?

A) $25 000

B) $10 000

C) $4000

D) ($8000)

In addition,the company incurred common fixed costs of $18 000.Which amount should be used to evaluate the Sydney Division as an investment of the company?

A) $25 000

B) $10 000

C) $4000

D) ($8000)

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following statements best completes this sentence? 'A cost is deemed to be controllable by the manager …'

A) who has staff authority over that cost

B) who has line authority over that cost

C) who is next in line to the financial controller of the firm

D) who is in the best position to influence that cost in some way

A) who has staff authority over that cost

B) who has line authority over that cost

C) who is next in line to the financial controller of the firm

D) who is in the best position to influence that cost in some way

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following statements unambiguously describes the term 'contribution margin'?

A) Contribution of the business unit towards the company's profits

B) Revenue minus the total manufacturing costs of the business unit

C) Revenue minus all variable costs of the business unit

D) Revenue minus all of the business unit's costs,whether fixed or variable

A) Contribution of the business unit towards the company's profits

B) Revenue minus the total manufacturing costs of the business unit

C) Revenue minus all variable costs of the business unit

D) Revenue minus all of the business unit's costs,whether fixed or variable

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

46

The data in a performance report helps managers to:

A) consider ways of improving their performance

B) use their computers

C) make personnel changes

D) eliminate spending

A) consider ways of improving their performance

B) use their computers

C) make personnel changes

D) eliminate spending

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following are characteristics of flash reports?

I)Provided daily

Ii)Include both financial and non-financial information

Iii)Comprehensive and cover the full range of performance criteria

A) i and ii

B) i and iii

C) ii and iii

D) All of the given answers

I)Provided daily

Ii)Include both financial and non-financial information

Iii)Comprehensive and cover the full range of performance criteria

A) i and ii

B) i and iii

C) ii and iii

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

48

Business unit reporting shows profit and loss statements for the company as a whole and for:

A) its major business units

B) controllable expenses

C) uncontrollable expenses

D) the contribution margin

A) its major business units

B) controllable expenses

C) uncontrollable expenses

D) the contribution margin

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

49

One advantage of business unit reports is that they make a distinction between business units and:

A) business unit managers

B) budgets

C) allocated costs

D) cost objects

A) business unit managers

B) budgets

C) allocated costs

D) cost objects

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following might you expect to see being used as a performance measure for an investment centre?

A) Return on investment

B) Actual business unit profit compared with budget business unit profit

C) Actual business unit revenue compared with budget business unit revenue

D) Both return on investment AND actual business unit revenue compared with budget business unit revenue

A) Return on investment

B) Actual business unit profit compared with budget business unit profit

C) Actual business unit revenue compared with budget business unit revenue

D) Both return on investment AND actual business unit revenue compared with budget business unit revenue

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

51

Callahan Company consists of two divisions,Northern and Southern.During 2008,many of the accounting records were destroyed in a fire.The managing director has asked the accountant for information relating to 2008.The following information is available to the accountant.In addition,the contribution margin ratio for both divisions was the same.What were the common fixed costs (z)during 2008?

A) $130 000

B) $45 000

C) $70 000

D) $65 000

A) $130 000

B) $45 000

C) $70 000

D) $65 000

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following might you expect to see being used as a performance measure for a revenue centre?

A) Actual business unit profit compared with budget business unit profit

B) Standard cost variances

C) Actual business unit revenue compared with budget business unit revenue

D) Both standard cost variances AND actual business unit revenue compared with budget business unit revenue

A) Actual business unit profit compared with budget business unit profit

B) Standard cost variances

C) Actual business unit revenue compared with budget business unit revenue

D) Both standard cost variances AND actual business unit revenue compared with budget business unit revenue

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following might you expect to see being used as a performance measure for a profit centre?

A) Return on investment

B) Actual business unit profit compared with budget business unit profit

C) Standard cost variances

D) Both return on investment AND standard cost variances

A) Return on investment

B) Actual business unit profit compared with budget business unit profit

C) Standard cost variances

D) Both return on investment AND standard cost variances

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

54

A common cost is:

A) not easily related to any business unit's activities

B) avoidable

C) employees' wages

D) direct labour

A) not easily related to any business unit's activities

B) avoidable

C) employees' wages

D) direct labour

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

55

Business unit profit and loss statements show:

A) profits for the major responsibility centres and for the organisation as a whole

B) profits by quarter for the organisation as a whole

C) comparative profits by year for the organisation as a whole

D) All of the given answers

A) profits for the major responsibility centres and for the organisation as a whole

B) profits by quarter for the organisation as a whole

C) comparative profits by year for the organisation as a whole

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following are risks associated with self-managed work teams?

I)Deterioration in job satisfaction of team members

Ii)Less opportunity to improve the quality of service

Iii)Slower response time to customer needs

A) i and ii

B) i and iii

C) ii and iii

D) None of the given answers

I)Deterioration in job satisfaction of team members

Ii)Less opportunity to improve the quality of service

Iii)Slower response time to customer needs

A) i and ii

B) i and iii

C) ii and iii

D) None of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following are benefits of self-managed work teams?

I)Improved customer service

Ii)Increased goal congruence among team members

Iii)Increased control by top management over outcomes

A) i and ii

B) i and iii

C) ii and iii

D) None of the given answers

I)Improved customer service

Ii)Increased goal congruence among team members

Iii)Increased control by top management over outcomes

A) i and ii

B) i and iii

C) ii and iii

D) None of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following are characteristics of shared service units?

I)Head office dominates

Ii)Usually structured as a cost centre

Iii)Services tend to be standardised

A) i and ii

B) i and iii

C) ii and iii

D) None of the given answers

I)Head office dominates

Ii)Usually structured as a cost centre

Iii)Services tend to be standardised

A) i and ii

B) i and iii

C) ii and iii

D) None of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following statements about business unit reporting is/are true?

I)Business unit reports distinguish between costs that are controllable by the business unit manager and costs that are beyond the influence of the business unit manager

Ii)These statements must be presented in an absorption-costing format.

Iii)Business unit reporting shows profit and loss statements for the company as a whole and for its major business units.

A) i and ii

B) All of the given answers

C) i and iii

D) ii and iii

I)Business unit reports distinguish between costs that are controllable by the business unit manager and costs that are beyond the influence of the business unit manager

Ii)These statements must be presented in an absorption-costing format.

Iii)Business unit reporting shows profit and loss statements for the company as a whole and for its major business units.

A) i and ii

B) All of the given answers

C) i and iii

D) ii and iii

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following might you expect to see being used as a performance measure for a cost centre?

A) Return on investment

B) Actual business unit profit compared with budget business unit profit

C) Standard cost variances

D) All of the given answers

A) Return on investment

B) Actual business unit profit compared with budget business unit profit

C) Standard cost variances

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

61

Although shared service units are generally established as profit centres it is often acceptable if a zero profit is achieved.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

62

In a divisional corporate organisation,an ideal inter-divisional transfer price should:

A) maximise the profits of the selling division

B) maximise the profits of the corporation

C) ensure goal congruence,divisional autonomy and motivation

D) All of the given answers

A) maximise the profits of the selling division

B) maximise the profits of the corporation

C) ensure goal congruence,divisional autonomy and motivation

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

63

Fruities Ltd has two divisions,Durian Division and Juice Division.Durian Division has an annual capacity of 10 000 units of either juice concentrate or fruit paste.Usually,Durian Division produces durian juice concentrate for the Juice Division.Juice Division's annual requirement of durian juice concentrate is 8000 units.There is no external market for durian juice concentrate;however,the Durian Division can use its facilities to manufacturer prune paste,which is a very popular product with unlimited external demand.The market price for prune paste is $13 per unit.The variable production cost of one unit of durian juice concentrate at Durian Division is $6,and the variable production cost of one unit of prune paste is $8.Durian division also incurs $1 additional shipping cost per unit when selling prune paste to external suppliers.Using the transfer pricing formula,what is the per unit transfer price selling one unit of durian juice concentrate to Juice Division?

A) $6

B) $8

C) $10

D) $11

A) $6

B) $8

C) $10

D) $11

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following is a benefit of decentralisation?

A) Increased motivation of management

B) Goal congruence

C) Focus on the firm as a whole

D) Suboptimal decision making

A) Increased motivation of management

B) Goal congruence

C) Focus on the firm as a whole

D) Suboptimal decision making

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

65

What is the general rule for setting a transfer price?

A) Additional costs of the supplying division + opportunity cost to the buying division

B) Additional costs of the supplying division + opportunity cost to the supplying division

C) Additional costs of the buying division + opportunity cost to the supplying division

D) Always set at full-cost-plus price

A) Additional costs of the supplying division + opportunity cost to the buying division

B) Additional costs of the supplying division + opportunity cost to the supplying division

C) Additional costs of the buying division + opportunity cost to the supplying division

D) Always set at full-cost-plus price

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

66

Fruities Ltd has two divisions,Durian Division and Juice Division.Durian Division has an annual capacity of 10 000 units of durian juice concentrate.Juice Division's annual requirement of durian juice concentrate is 8000 units.There is no external market for durian juice concentrate;however,the Durian Division can use its facilities to manufacturer prune paste,which is a very popular product with unlimited external demand,at $13 per unit.The variable production cost of one unit of durian juice concentrate at Durian Division is $6,and the variable production cost of one unit of prune paste is $8.Durian division also incurs $1 additional shipping cost per unit when selling prune paste to external suppliers.Using the transfer pricing formula,what is the per unit opportunity cost of selling one unit of durian juice concentrate to Juice Division?

A) $0

B) $4

C) $5

D) $12

A) $0

B) $4

C) $5

D) $12

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following is a problem with the use of cost-based transfer pricing?

A) It does not lead to optimal decisions for the firm.

B) There are many definitions of cost-based transfer pricing.

C) There are potential goal-congruence problems.

D) It does not lead to optimal decisions for the firm AND there are potential goal-congruence problems.

A) It does not lead to optimal decisions for the firm.

B) There are many definitions of cost-based transfer pricing.

C) There are potential goal-congruence problems.

D) It does not lead to optimal decisions for the firm AND there are potential goal-congruence problems.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following is a key problem with the use of market-based transfer prices?

A) It does not take into account the saving in cost (e.g.selling expenses,collection expenses)because of transferring internally.

B) It leads to decision making that is suboptimal for the firm.

C) It does not promote divisional autonomy.

D) It does not show the contribution of each division to overall profit.

A) It does not take into account the saving in cost (e.g.selling expenses,collection expenses)because of transferring internally.

B) It leads to decision making that is suboptimal for the firm.

C) It does not promote divisional autonomy.

D) It does not show the contribution of each division to overall profit.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

69

When management is using performance reports to evaluate the performance of a business unit manager,which of the following costs should be considered:

A) Any costs that are attributable to the business unit

B) Common costs and any costs that are attributable to the business unit

C) Costs controllable by the business unit manager,common costs,and any costs that are attributable to the business unit

D) Only costs controllable by the business unit manager

A) Any costs that are attributable to the business unit

B) Common costs and any costs that are attributable to the business unit

C) Costs controllable by the business unit manager,common costs,and any costs that are attributable to the business unit

D) Only costs controllable by the business unit manager

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

70

A strategic business unit is:

A) A cost centre

B) Either a revenue centre or a profit centre

C) Either a revenue centre or an investment centre.

D) Either a profit centre or an investment centre.

A) A cost centre

B) Either a revenue centre or a profit centre

C) Either a revenue centre or an investment centre.

D) Either a profit centre or an investment centre.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following is a problem with the use of a negotiated transfer price?

A) The negotiations can be extremely time-consuming.

B) The final transfer price may be primarily due to an individual's superior negotiation skills.

C) It can lead to suboptimal decisions for the firm.

D) All of the given answers

A) The negotiations can be extremely time-consuming.

B) The final transfer price may be primarily due to an individual's superior negotiation skills.

C) It can lead to suboptimal decisions for the firm.

D) All of the given answers

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

72

When management is using performance reports to evaluate the economic performance of a business unit,which of the following costs should be considered:

A) Any costs that are attributable to the business unit

B) Costs that are both attributable to the business unit AND are controllable by the business unit manager

C) Common costs and any costs that are attributable to the business unit

D) Only costs controllable by the business unit manager

A) Any costs that are attributable to the business unit

B) Costs that are both attributable to the business unit AND are controllable by the business unit manager

C) Common costs and any costs that are attributable to the business unit

D) Only costs controllable by the business unit manager

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

73

Fruities Ltd has two divisions,Durian Division and Juice Division.Durian Division has an annual capacity of 10 000 units of durian juice concentrate.Juice Division's annual requirement of durian juice concentrate is 8000 units.Fruities Ltd requires that divisions should purchase inputs internally where available,and uses a cost-plus transfer price policy,where transfer price is set at variable cost plus 25 per cent.Therefore,Durian Division always satisfies the demand of the Juice Division first,before selling the remaining durian concentrate to external suppliers at the market price of $10 per unit.The variable cost of one unit of durian juice concentrate at Durian Division is $6.The external demand for Durian Division's durian juice concentrate is 2000 units.What is the difference in the overall profit of Fruities Ltd under the cost-plus transfer price policy and a market-price transfer price policy?

A) Fruities Ltd's profit is $20 000 lower under the cost-plus transfer pricing approach

B) Fruities Ltd's profit is $20 000 higher under the cost-plus transfer pricing approach

C) Fruites Ltd's profit is $25 000 higher under the cost-plus transfer pricing approach

D) There is no difference under the two policies.

A) Fruities Ltd's profit is $20 000 lower under the cost-plus transfer pricing approach

B) Fruities Ltd's profit is $20 000 higher under the cost-plus transfer pricing approach

C) Fruites Ltd's profit is $25 000 higher under the cost-plus transfer pricing approach

D) There is no difference under the two policies.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following statements best completes this sentence? 'The biggest challenge(s)facing all decentralised firms is …'

A) to reap the advantages of autonomy

B) to attempt to ensure goal congruence

C) to choose the most appropriate transfer price

D) to reap the advantages of autonomy AND to attempt to ensure goal congruence

A) to reap the advantages of autonomy

B) to attempt to ensure goal congruence

C) to choose the most appropriate transfer price

D) to reap the advantages of autonomy AND to attempt to ensure goal congruence

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

75

Which of the following information should be taken into account when using a negotiated transfer price method to determine transfer price?

I)external market price

Ii savings in selling and distribution costs when transferring internally

Iii excess capacity in the selling division

Iv excess capacity in the buying division

A) ii and iii

B) i,ii and iii

C) ii,iii and iv

D) i,ii,iii and iv

I)external market price

Ii savings in selling and distribution costs when transferring internally

Iii excess capacity in the selling division

Iv excess capacity in the buying division

A) ii and iii

B) i,ii and iii

C) ii,iii and iv

D) i,ii,iii and iv

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

76

If a manager were responsible for a division's performance and activities,the division would have to be classified as a cost centre.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

77

Fruities Ltd has two divisions,Durian Division and Juice Division.Durian Division has an annual capacity of 10 000 units of durian juice concentrate.Juice Division's annual requirement of durian juice concentrate is 8000 units.The variable production cost of one unit of durian juice concentrate at Durian Division is $6,but the division incurs $1 additional shipping cost per unit when selling to external suppliers.The market price for the division's durian juice concentrate is $10 per unit,and currently,the external demand for Durian Division's durian juice concentrate is 5000 units.Using the transfer pricing formula,Durian Division should charge the Juice Division:

A) $6.00

B) $7.13

C) $9.00

D) $10.00

A) $6.00

B) $7.13

C) $9.00

D) $10.00

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

78

The difference between establishing a shared service unit and centralisation shared services include:

I)centralised services are located at corporate headquarters;shared services are located close to internal customers

Ii centralised services are more efficient than shared services

Iii centralised services are evaluated based on service adherence to service level agreements;shared services are evaluated based on budgets and corporate objectives

A) i and ii

B) iii

C) i

D) i and iii

I)centralised services are located at corporate headquarters;shared services are located close to internal customers

Ii centralised services are more efficient than shared services

Iii centralised services are evaluated based on service adherence to service level agreements;shared services are evaluated based on budgets and corporate objectives

A) i and ii

B) iii

C) i

D) i and iii

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

79

Fruities Ltd has two divisions,Durian Division and Juice Division.Durian Division has an annual capacity of 10 000 units of durian juice concentrate.Juice Division's annual requirement of durian juice concentrate is 8000 units.Fruities Ltd requires that divisions should purchase inputs internally where available and uses a cost-plus transfer price policy,where transfer price is set at variable cost plus 25 per cent.Therefore,Durian Division always satisfies the demand of the Juice Division first,before selling the remaining durian concentrate to external suppliers at the market price of $10 per unit.The variable cost of one unit of durian juice concentrate at Durian Division is $6.What is the difference in Durian Division's profit under the cost-plus transfer price policy and a market-price transfer price policy?

A) Fruities Ltd's profit is $20 000 lower under the cost-plus transfer pricing approach

B) Fruities Ltd's profit is $20 000 higher under the cost-plus transfer pricing approach

C) Fruites Ltd's profit is $25 000 higher under the cost-plus transfer pricing approach

D) There is no difference under the two policies.

A) Fruities Ltd's profit is $20 000 lower under the cost-plus transfer pricing approach

B) Fruities Ltd's profit is $20 000 higher under the cost-plus transfer pricing approach

C) Fruites Ltd's profit is $25 000 higher under the cost-plus transfer pricing approach

D) There is no difference under the two policies.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

80

When the transfer price chosen by management charges another department the price that would be charged to outside customers,this type of transfer pricing is called:

A) marginal cost transfer pricing

B) cost-based transfer pricing

C) market-based transfer pricing

D) negotiated transfer pricing

A) marginal cost transfer pricing

B) cost-based transfer pricing

C) market-based transfer pricing

D) negotiated transfer pricing

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 88 flashcards in this deck.