Deck 20: Accounting Changes and Error Corrections

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Pages,Inc.receives subscription payments for annual (one year)subscriptions to its magazine.Payments are recorded as revenue when received.Amounts received but unearned at the end of each of the last three years are shown below.  Pages failed to record the unearned revenues in each of the three years.The entry needed to correct the above errors is

Pages failed to record the unearned revenues in each of the three years.The entry needed to correct the above errors is

A) Retained Earnings ..................150,000

Subscription Revenues ..............26,000

Unearned Revenues ...............176,000

B) Retained Earnings ..................30,000

Subscription Revenues ..............26,000

Unearned Revenues ...............56,000

C) Subscription Revenues ..............176,000

Unearned Revenues ...............176,000

D) Subscription Revenues ..............150,000

Retained Earnings ..................26,000

Unearned Revenues ...............176,000

Pages failed to record the unearned revenues in each of the three years.The entry needed to correct the above errors isA) Retained Earnings ..................150,000

Subscription Revenues ..............26,000

Unearned Revenues ...............176,000

B) Retained Earnings ..................30,000

Subscription Revenues ..............26,000

Unearned Revenues ...............56,000

C) Subscription Revenues ..............176,000

Unearned Revenues ...............176,000

D) Subscription Revenues ..............150,000

Retained Earnings ..................26,000

Unearned Revenues ...............176,000

Question

Question

Question

Question

Question

Question

Strong Company's December 31 year-end financial statements contained the following errors:  An insurance premium of $3,600 was prepaid in 2013 covering the years 2013,2014,and 2015.The entire amount was charged to expense in 2013.In addition,on December 31,2014,fully depreciated machinery was sold for $6,400 cash,but the sale was not recorded until 2015.There were no other errors during 2013 or 2014,and no corrections have been made for any of the errors.Ignore income tax considerations.What is the total effect of the errors on 2014 net income?

An insurance premium of $3,600 was prepaid in 2013 covering the years 2013,2014,and 2015.The entire amount was charged to expense in 2013.In addition,on December 31,2014,fully depreciated machinery was sold for $6,400 cash,but the sale was not recorded until 2015.There were no other errors during 2013 or 2014,and no corrections have been made for any of the errors.Ignore income tax considerations.What is the total effect of the errors on 2014 net income?

A) Net income is understated by $12,800.

B) Net income is overstated by $3,600.

C) Net income is understated by $1,600.

D) Net income is overstated by $2,400.

An insurance premium of $3,600 was prepaid in 2013 covering the years 2013,2014,and 2015.The entire amount was charged to expense in 2013.In addition,on December 31,2014,fully depreciated machinery was sold for $6,400 cash,but the sale was not recorded until 2015.There were no other errors during 2013 or 2014,and no corrections have been made for any of the errors.Ignore income tax considerations.What is the total effect of the errors on 2014 net income?A) Net income is understated by $12,800.

B) Net income is overstated by $3,600.

C) Net income is understated by $1,600.

D) Net income is overstated by $2,400.

Question

Cornwall Co.made the following errors in counting its year-end physical inventories:  The entry to correct the accounts at the end of 2014 is

The entry to correct the accounts at the end of 2014 is

A) Retained Earnings ...................48,000

Cost of Goods Sold ..................42,000

Inventory ........................90,000

B) Retained Earnings ...................18,000

Cost of Goods Sold ..................72,000

Inventory ........................90,000

C) Inventory ..........................90,000

Cost of Goods Sold ...............18,000

Retained Earnings ...............72,000

D) Cost of Goods Sold ..................198,000

Retained Earnings ................108,000

Inventory ........................90,000

The entry to correct the accounts at the end of 2014 isA) Retained Earnings ...................48,000

Cost of Goods Sold ..................42,000

Inventory ........................90,000

B) Retained Earnings ...................18,000

Cost of Goods Sold ..................72,000

Inventory ........................90,000

C) Inventory ..........................90,000

Cost of Goods Sold ...............18,000

Retained Earnings ...............72,000

D) Cost of Goods Sold ..................198,000

Retained Earnings ................108,000

Inventory ........................90,000

Question

Rickles,Inc.is a calendar-year corporation whose financial statements for 2013 and 2014 included errors as follows:  Assume that purchases were recorded correctly and that no correcting entries were made at December 31,2013,or December 31,2014.Ignoring income taxes,by how much should Rickles's retained earnings be retroactively adjusted at January 1,2015?

Assume that purchases were recorded correctly and that no correcting entries were made at December 31,2013,or December 31,2014.Ignoring income taxes,by how much should Rickles's retained earnings be retroactively adjusted at January 1,2015?

A) $27,000 increase

B) $27,000 decrease

C) $7,000 decrease

D) $3,000 decrease

Assume that purchases were recorded correctly and that no correcting entries were made at December 31,2013,or December 31,2014.Ignoring income taxes,by how much should Rickles's retained earnings be retroactively adjusted at January 1,2015?A) $27,000 increase

B) $27,000 decrease

C) $7,000 decrease

D) $3,000 decrease

Question

Question

McCartney Corp.reports on a calendar-year basis.Its 2013 and 2014 financial statements contained the following errors:  As a result of the above errors,2014 income would be

As a result of the above errors,2014 income would be

A) overstated by $4,000.

B) overstated by $24,000.

C) overstated by $22,000.

D) overstated by $16,000.

As a result of the above errors,2014 income would beA) overstated by $4,000.

B) overstated by $24,000.

C) overstated by $22,000.

D) overstated by $16,000.

Question

Crafter,Inc.receives subscription payments for annual (one year)subscriptions to its magazine.Payments are recorded as revenue when received.Amounts received but unearned at the end of each of the last three years are shown below:  Crafter failed to record the unearned revenues in each of the three years.As a result of the omission,2014 income was

Crafter failed to record the unearned revenues in each of the three years.As a result of the omission,2014 income was

A) overstated by $146,000.

B) understated by $146,000.

C) understated by $26,000.

D) overstated by $26,000.

Crafter failed to record the unearned revenues in each of the three years.As a result of the omission,2014 income wasA) overstated by $146,000.

B) understated by $146,000.

C) understated by $26,000.

D) overstated by $26,000.

Question

Question

Question

Newsman Co.made the following errors in counting its year-end physical inventories:  As a result of the above undetected errors,2014 income was

As a result of the above undetected errors,2014 income was

A) understated by $18,000.

B) overstated by $198,000.

C) overstated by $18,000.

D) understated by $198,000.

As a result of the above undetected errors,2014 income wasA) understated by $18,000.

B) overstated by $198,000.

C) overstated by $18,000.

D) understated by $198,000.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On January 1,2011,Shine Services Inc.purchased a new machine for $600,000.The machine had an estimated useful life of eight years and a salvage value of $150,000.Shine elected to depreciate the machine using the double-declining-balance method.On January 1,2014,the company decided to change to straight-line depreciation.

Ignoring income tax considerations,prepare the entries to record

Ignoring income tax considerations,prepare the entries to record

Question

Question

Question

Question

Diamond Company changed from the completed-contract method of accounting for long-term contracts to the percentage-of-completion method,during 2014.Reported earnings in 2013 were $50,000,and the beginning 2013 retained earnings balance was $150,000.Net income for 2014 under the competed-contract method would have been $140,000.No dividends were declared during 2013 and 2014.

Required:

Required:

Prepare the 2013 and 2014 comparative retained earnings statements.

Required:Prepare the 2013 and 2014 comparative retained earnings statements.

Question

Question

A retailing firm changed from LIFO to FIFO in 2014.Inventory valuations for the two methods appear below:

Purchases in 2013 and 2014 were $60,000 in each year.

Purchases in 2013 and 2014 were $60,000 in each year.

Using the information above,in the comparative 2013 and 2014 income statements,what amounts would be shown for cost of goods sold? 2013 2014

A) $50,000 $58,000

B) $51,000 $55,000

C) $50,000 $55,000

D) $51,000 $58,000

Purchases in 2013 and 2014 were $60,000 in each year.Using the information above,in the comparative 2013 and 2014 income statements,what amounts would be shown for cost of goods sold? 2013 2014

A) $50,000 $58,000

B) $51,000 $55,000

C) $50,000 $55,000

D) $51,000 $58,000

Question

Question

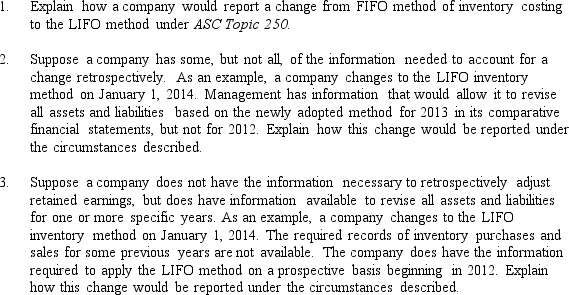

FASB ASC Topic 250 (Presentation-Accounting Changes and Error Corrections,requires that voluntary changes in accounting principles be reported retrospectively.The standard recognizes that such retrospective restatement is not always practical.

Required:

Required:

Question

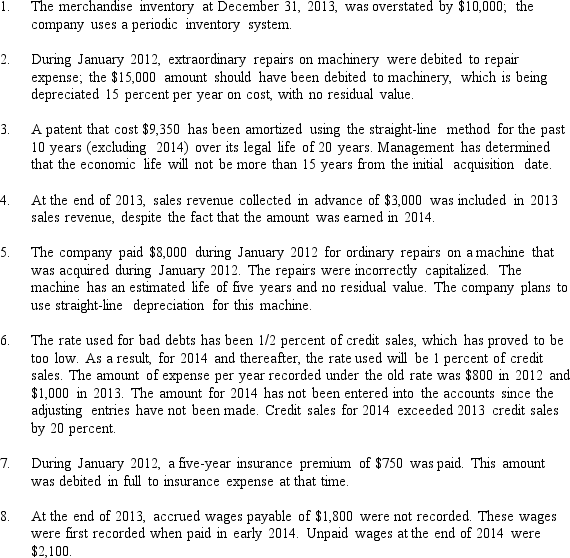

Witherfork Company was recently acquired by a new owner who has decided to correct the prior accounting records during the current reporting period ending December 31,2014.The accounts have been partially adjusted but have not been closed for 2014.The following items have been discovered:

Required:

Required:

Provide the appropriate entry to record any change or correction and give any adjusting entry needed in each instance at the end of 2014.Show computations for entries made,and provide explanations for situations for which no entry is required.

Required:Provide the appropriate entry to record any change or correction and give any adjusting entry needed in each instance at the end of 2014.Show computations for entries made,and provide explanations for situations for which no entry is required.

Question

Question

Question

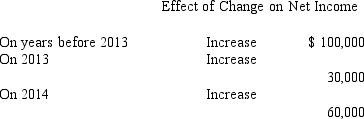

Improved Technologies has estimated bad debts using the percentage-of-sales method since their business began operations in 2011.Information relating to bad debts and sales is as follows:

At the beginning of 2014,Improved proposes changing their estimation of bad debt expense from 3 percent of sales to 2.5 percent.Sales for the year totaled $186,000 and actual bad debts amounted to $3,910.

At the beginning of 2014,Improved proposes changing their estimation of bad debt expense from 3 percent of sales to 2.5 percent.Sales for the year totaled $186,000 and actual bad debts amounted to $3,910.

At the beginning of 2014,Improved proposes changing their estimation of bad debt expense from 3 percent of sales to 2.5 percent.Sales for the year totaled $186,000 and actual bad debts amounted to $3,910. Question

A retailing firm changed from LIFO to FIFO in 2014.Inventory valuations for the two methods appear below:

Purchases in 2013 and 2014 were $60,000 in each year.

Using the information above,choose the following:

A) $4,000 RE $55,000

B) $7,000 RE $58,000

C) $4,000 Earnings $55,000

D) $7,000 Earnings $58,000

Purchases in 2013 and 2014 were $60,000 in each year.Using the information above,choose the following:

A) $4,000 RE $55,000

B) $7,000 RE $58,000

C) $4,000 Earnings $55,000

D) $7,000 Earnings $58,000

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/77

Play

Full screen (f)

Deck 20: Accounting Changes and Error Corrections

1

Which of the following does NOT represent a change in reporting entity?

A) Changing the companies included in combined financial statements

B) Disposition of a subsidiary or other business unit

C) Presenting consolidated statements in place of the statements of individual companies

D) Changing specific subsidiaries that constitute the group of companies for which consolidated financial statements are presented

A) Changing the companies included in combined financial statements

B) Disposition of a subsidiary or other business unit

C) Presenting consolidated statements in place of the statements of individual companies

D) Changing specific subsidiaries that constitute the group of companies for which consolidated financial statements are presented

B

2

Which of the following concepts or principles relates most directly to reporting accounting changes and errors?

A) Conservatism

B) Consistency

C) Objectivity

D) Materiality

A) Conservatism

B) Consistency

C) Objectivity

D) Materiality

B

3

Which of the following is NOT a change in accounting principle?

A) A change from FIFO to LIFO for inventory valuation

B) A change from eight years to five years in the useful life of a depreciable asset

C) A change from completed-contracts to percentage-of-completion

D) A change from double-declining-balance to straight-line depreciation

A) A change from FIFO to LIFO for inventory valuation

B) A change from eight years to five years in the useful life of a depreciable asset

C) A change from completed-contracts to percentage-of-completion

D) A change from double-declining-balance to straight-line depreciation

B

4

Which of the following is correct regarding the provisions of IAS No.8 on accounting changes and error corrections?

A) IAS No.8 requires that correction of an error be made only by restatement of all prior periods presented.

B) IAS No.8 requires correction of an error to be made only by reflecting the effect of the correction in income of the period in which the error was discovered without restating previously reported results.

C) IAS No.8 allows correction of an error to be made either through restatement of all period periods presented or by reflecting the effect of the correction in income of the period in which the error was discovered without restating previously reported results.

D) IAS No.8 reflects a preference for not restating prior results in reporting accounting changes and error corrections.

A) IAS No.8 requires that correction of an error be made only by restatement of all prior periods presented.

B) IAS No.8 requires correction of an error to be made only by reflecting the effect of the correction in income of the period in which the error was discovered without restating previously reported results.

C) IAS No.8 allows correction of an error to be made either through restatement of all period periods presented or by reflecting the effect of the correction in income of the period in which the error was discovered without restating previously reported results.

D) IAS No.8 reflects a preference for not restating prior results in reporting accounting changes and error corrections.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following changes in accounting principle does not require the retrospective approach?

A) Change from the percentage-of-completion to the completed-contract method

B) Change of inventory method from LIFO to FIFO

C) Change of inventory method from FIFO to LIFO

D) All of these require retroactive adjustment.

A) Change from the percentage-of-completion to the completed-contract method

B) Change of inventory method from LIFO to FIFO

C) Change of inventory method from FIFO to LIFO

D) All of these require retroactive adjustment.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is NOT correct regarding a change in reporting entity?

A) Financial statements of the year in which the change in reporting entity is made should disclose the nature of the change and the reason for the change.

B) The effect of the change on income before extraordinary items,net income,and earnings per share amounts should be reported for all periods presented.

C) Financial statements presented for all prior periods must be restated.

D) The effect of the change on income before extraordinary items,net income,and earnings per share amounts should be reported for all periods presented and must be repeated in all periods subsequent to the period of the change.

A) Financial statements of the year in which the change in reporting entity is made should disclose the nature of the change and the reason for the change.

B) The effect of the change on income before extraordinary items,net income,and earnings per share amounts should be reported for all periods presented.

C) Financial statements presented for all prior periods must be restated.

D) The effect of the change on income before extraordinary items,net income,and earnings per share amounts should be reported for all periods presented and must be repeated in all periods subsequent to the period of the change.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

7

The cumulative effect on prior years' earnings of a change in accounting principle should be reported separately as an adjustment to retained earnings for the earliest period presented for all of the following changes except

A) completed-contract method of accounting for long-term construction-type contracts to the percentage-of-completion method.

B) percentage-of-completion method of accounting for long-term construction-type contracts to the completed-contract method.

C) FIFO method of inventory pricing to LIFO method.

D) LIFO method of inventory pricing to the weighted-average method.

A) completed-contract method of accounting for long-term construction-type contracts to the percentage-of-completion method.

B) percentage-of-completion method of accounting for long-term construction-type contracts to the completed-contract method.

C) FIFO method of inventory pricing to LIFO method.

D) LIFO method of inventory pricing to the weighted-average method.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

8

An example of an item that should be reported as a prior period adjustment is the

A) collection of previously written off accounts receivable.

B) payment of taxes resulting from examination of prior years' income tax returns.

C) correction of an error in financial statements of a prior year.

D) receipt of insurance proceeds for damage to a building sustained in a prior year.

A) collection of previously written off accounts receivable.

B) payment of taxes resulting from examination of prior years' income tax returns.

C) correction of an error in financial statements of a prior year.

D) receipt of insurance proceeds for damage to a building sustained in a prior year.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

9

The correction of an error in the financial statements of a prior period should be reflected,net of applicable income taxes,in the current

A) income statement after income from continuing operations and before extraordinary items.

B) income statement after income from continuing operations and after extraordinary items.

C) retained earnings statement after net income but before dividends.

D) retained earnings statement as an adjustment of the opening balance.

A) income statement after income from continuing operations and before extraordinary items.

B) income statement after income from continuing operations and after extraordinary items.

C) retained earnings statement after net income but before dividends.

D) retained earnings statement as an adjustment of the opening balance.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following should be reported as a change in accounting estimate?

A) Change in the reported beginning inventory amount due to a discovery of a bookkeeping error

B) Change from the completed-contract method to the percentage-of- completion method for revenue recognition on long-term construction contracts

C) Increase in the rate applied to net credit sales from 1 percent to 1-1/2 percent in determining losses from uncollectible receivables

D) Change made to comply with a new FASB pronouncement

A) Change in the reported beginning inventory amount due to a discovery of a bookkeeping error

B) Change from the completed-contract method to the percentage-of- completion method for revenue recognition on long-term construction contracts

C) Increase in the rate applied to net credit sales from 1 percent to 1-1/2 percent in determining losses from uncollectible receivables

D) Change made to comply with a new FASB pronouncement

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

11

The effect of a change in accounting principle that is inseparable from the effect of a change in accounting estimate should be reported

A) by showing the pro forma effects of retroactive application.

B) by restating the financial statements of all prior periods presented.

C) in the period of change and future periods

D) as a correction of an error.

A) by showing the pro forma effects of retroactive application.

B) by restating the financial statements of all prior periods presented.

C) in the period of change and future periods

D) as a correction of an error.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following is the proper time period in which to record a change in accounting estimate?

A) Current period and future periods

B) Current period and retroactively

C) Retroactively only

D) Current period only

A) Current period and future periods

B) Current period and retroactively

C) Retroactively only

D) Current period only

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

13

At the time Hollywood Corporation became a subsidiary of Vine Corporation,Hollywood switched depreciation of its plant assets from the straight-line method to the sum-of-the-years'-digits method used by Vine.With respect to Hollywood,this change was a

A) change in an accounting estimate.

B) correction of an error.

C) change in the reporting entity.

D) change in accounting principle.

A) change in an accounting estimate.

B) correction of an error.

C) change in the reporting entity.

D) change in accounting principle.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following accounting treatments is proper for a change in reporting entity?

A) Restatement of all financial statements presented

B) Restatement of current period financial statements

C) Note disclosure and supplementary schedules

D) Adjustment to retained earnings and note disclosure

A) Restatement of all financial statements presented

B) Restatement of current period financial statements

C) Note disclosure and supplementary schedules

D) Adjustment to retained earnings and note disclosure

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

15

A company changes from an accounting principle that is not generally accepted to one that is generally accepted.The effect of the change should be reported as a

A) change in accounting principle.

B) change in accounting estimate

C) correction of an error.

D) change of accounting estimate effected by a change in accounting principle.

A) change in accounting principle.

B) change in accounting estimate

C) correction of an error.

D) change of accounting estimate effected by a change in accounting principle.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is not correct regarding the provisions of IAS No.8 on accounting changes and error corrections?

A) A change in accounting estimate is reflected in the current and future periods.

B) A change in depreciation method (such as from an accelerated method to the straight-line method)is classified as a change in estimate.

C) A change in depreciation method (such as from accelerated method to the straight-line method)is classified as a change in accounting principle.

D) IAS No.8 generally reflects a preference for restating prior results to improve comparability of financial statements.

A) A change in accounting estimate is reflected in the current and future periods.

B) A change in depreciation method (such as from an accelerated method to the straight-line method)is classified as a change in estimate.

C) A change in depreciation method (such as from accelerated method to the straight-line method)is classified as a change in accounting principle.

D) IAS No.8 generally reflects a preference for restating prior results to improve comparability of financial statements.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is NOT a change in reporting entity?

A) A company acquires a subsidiary that is to be accounted for as a purchase.

B) A company presents consolidated or combined statements in place of statements of individual companies.

C) A company changes the companies included in combined financial statements.

D) A company changes the subsidiaries for which consolidated statements are presented.

A) A company acquires a subsidiary that is to be accounted for as a purchase.

B) A company presents consolidated or combined statements in place of statements of individual companies.

C) A company changes the companies included in combined financial statements.

D) A company changes the subsidiaries for which consolidated statements are presented.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

18

Albritton Inc.bought a patent for $900,000 on January 2,2010,at which time the patent had an estimated useful life of ten years.On February 2,2014,it was determined that the patent's useful life would expire at the end of 2016.How much would Albritton record as amortization expense for this patent for the year ending December 31,2014?

A) $200,000

B) $180,000

C) $110,000

D) $90,000

A) $200,000

B) $180,000

C) $110,000

D) $90,000

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is not correct regarding the provisions of IAS No.8 on accounting changes and error corrections?

A) IAS No.8 requires that results from prior periods be presented for all changes in accounting principles.

B) IAS No.8 allows a change in accounting principle to be accounted for by reflecting the cumulative effect of the change in the income of the current period without restating prior-period results.

C) Under IAS No.8,the recommended approach for a change in accounting principle is that results from prior periods should be restated.

D) IAS No.8 requires a change in accounting estimate to be reflected in the current and future periods.

A) IAS No.8 requires that results from prior periods be presented for all changes in accounting principles.

B) IAS No.8 allows a change in accounting principle to be accounted for by reflecting the cumulative effect of the change in the income of the current period without restating prior-period results.

C) Under IAS No.8,the recommended approach for a change in accounting principle is that results from prior periods should be restated.

D) IAS No.8 requires a change in accounting estimate to be reflected in the current and future periods.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

20

An accounting change that requires the retrospective approach is a change in

A) the life of equipment from five to seven years.

B) depreciation method from straight-line to double-declining-balance.

C) he percentage used to determine the allowance for bad debts.

D) the specific subsidiaries included in consolidated financial statements.t

A) the life of equipment from five to seven years.

B) depreciation method from straight-line to double-declining-balance.

C) he percentage used to determine the allowance for bad debts.

D) the specific subsidiaries included in consolidated financial statements.t

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

21

Pages,Inc.receives subscription payments for annual (one year)subscriptions to its magazine.Payments are recorded as revenue when received.Amounts received but unearned at the end of each of the last three years are shown below. Pages failed to record the unearned revenues in each of the three years.The entry needed to correct the above errors is

A) Retained Earnings ..................150,000

Subscription Revenues ..............26,000

Unearned Revenues ...............176,000

B) Retained Earnings ..................30,000

Subscription Revenues ..............26,000

Unearned Revenues ...............56,000

C) Subscription Revenues ..............176,000

Unearned Revenues ...............176,000

D) Subscription Revenues ..............150,000

Retained Earnings ..................26,000

Unearned Revenues ...............176,000

Pages failed to record the unearned revenues in each of the three years.The entry needed to correct the above errors isA) Retained Earnings ..................150,000

Subscription Revenues ..............26,000

Unearned Revenues ...............176,000

B) Retained Earnings ..................30,000

Subscription Revenues ..............26,000

Unearned Revenues ...............56,000

C) Subscription Revenues ..............176,000

Unearned Revenues ...............176,000

D) Subscription Revenues ..............150,000

Retained Earnings ..................26,000

Unearned Revenues ...............176,000

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements is not correct?

A) A change from an inappropriate accounting principle to a proper one should be accounted for as an accounting error.

B) A change from an inappropriate accounting principle to a proper one should be accounted for as a change in accounting principle.

C) A change from an inappropriate accounting principle to a proper one should be accounted for retrospectively.

D) A change from an inappropriate accounting principle to a proper one may require an adjustment to beginning retained earnings for the earliest year reported.

A) A change from an inappropriate accounting principle to a proper one should be accounted for as an accounting error.

B) A change from an inappropriate accounting principle to a proper one should be accounted for as a change in accounting principle.

C) A change from an inappropriate accounting principle to a proper one should be accounted for retrospectively.

D) A change from an inappropriate accounting principle to a proper one may require an adjustment to beginning retained earnings for the earliest year reported.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

23

On January 1,2011,Caravanos Company purchased for $320,000 a machine with a useful life of ten years and no salvage value.The machine was depreciated by the double-declining-balance method,and the carrying amount of the machine was $204,800 on December 31,2012.Caravanos changed to the straight-line method on January 1,2013.Caravanos can justify the change.What should be the depreciation expense on this machine for the year ended December 31,2014?

A) $20,480

B) 25,600

C) 32,000

D) 52,480

A) $20,480

B) 25,600

C) 32,000

D) 52,480

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

24

Basilia Corporation purchased a machine for $180,000 on January 1,2013.Basilia will depreciate the machine using the straight-line method using a five-year period with no residual value.As a result of an error in its purchasing records,Basilia did not recognize any depreciation for the machine in its 2013 financial statements.Basilia discovered the during the preparation of its 2014 financial statements.What amount should Basilia record for depreciation expense on this machine for 2014?

A) $0

B) $36,000

C) $44,000

D) $72,000

A) $0

B) $36,000

C) $44,000

D) $72,000

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

25

On December 31,2014,Ohio Corporation appropriately changed its inventory valuation method to FIFO cost from LIFO cost for both financial statement and income tax purposes.The change will result in a $140,000 increase in the beginning inventory at January 1,2014.Assume a 30 percent income tax rate.The cumulative effect of this accounting change Ohio for the year ended December 31,2014,is

A) $0.

B) $42,000.

C) $98,000.

D) $140,000.

A) $0.

B) $42,000.

C) $98,000.

D) $140,000.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

26

On January 1,2011,Mardi Gras Shipping bought a machine for $1,500,000.At that time,this machine had an estimated useful life of six years,with no salvage value.As a result of additional information,Mardi Gras determined on January 1,2014,that the machine had an estimated useful life of eight years from the date it was acquired,with no salvage value.Accordingly,the appropriate accounting change was made in 2014.How much depreciation expense for this machine should Mardi Gras record for the year ended December 31,2014,assuming Mardi Gras uses the straight-line method of depreciation?

A) $125,000

B) $150,000

C) $187,500

D) $250,000

A) $125,000

B) $150,000

C) $187,500

D) $250,000

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

27

Strong Company's December 31 year-end financial statements contained the following errors: An insurance premium of $3,600 was prepaid in 2013 covering the years 2013,2014,and 2015.The entire amount was charged to expense in 2013.In addition,on December 31,2014,fully depreciated machinery was sold for $6,400 cash,but the sale was not recorded until 2015.There were no other errors during 2013 or 2014,and no corrections have been made for any of the errors.Ignore income tax considerations.What is the total effect of the errors on 2014 net income?

A) Net income is understated by $12,800.

B) Net income is overstated by $3,600.

C) Net income is understated by $1,600.

D) Net income is overstated by $2,400.

An insurance premium of $3,600 was prepaid in 2013 covering the years 2013,2014,and 2015.The entire amount was charged to expense in 2013.In addition,on December 31,2014,fully depreciated machinery was sold for $6,400 cash,but the sale was not recorded until 2015.There were no other errors during 2013 or 2014,and no corrections have been made for any of the errors.Ignore income tax considerations.What is the total effect of the errors on 2014 net income?A) Net income is understated by $12,800.

B) Net income is overstated by $3,600.

C) Net income is understated by $1,600.

D) Net income is overstated by $2,400.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

28

Cornwall Co.made the following errors in counting its year-end physical inventories: The entry to correct the accounts at the end of 2014 is

A) Retained Earnings ...................48,000

Cost of Goods Sold ..................42,000

Inventory ........................90,000

B) Retained Earnings ...................18,000

Cost of Goods Sold ..................72,000

Inventory ........................90,000

C) Inventory ..........................90,000

Cost of Goods Sold ...............18,000

Retained Earnings ...............72,000

D) Cost of Goods Sold ..................198,000

Retained Earnings ................108,000

Inventory ........................90,000

The entry to correct the accounts at the end of 2014 isA) Retained Earnings ...................48,000

Cost of Goods Sold ..................42,000

Inventory ........................90,000

B) Retained Earnings ...................18,000

Cost of Goods Sold ..................72,000

Inventory ........................90,000

C) Inventory ..........................90,000

Cost of Goods Sold ...............18,000

Retained Earnings ...............72,000

D) Cost of Goods Sold ..................198,000

Retained Earnings ................108,000

Inventory ........................90,000

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

29

Rickles,Inc.is a calendar-year corporation whose financial statements for 2013 and 2014 included errors as follows: Assume that purchases were recorded correctly and that no correcting entries were made at December 31,2013,or December 31,2014.Ignoring income taxes,by how much should Rickles's retained earnings be retroactively adjusted at January 1,2015?

A) $27,000 increase

B) $27,000 decrease

C) $7,000 decrease

D) $3,000 decrease

Assume that purchases were recorded correctly and that no correcting entries were made at December 31,2013,or December 31,2014.Ignoring income taxes,by how much should Rickles's retained earnings be retroactively adjusted at January 1,2015?A) $27,000 increase

B) $27,000 decrease

C) $7,000 decrease

D) $3,000 decrease

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

30

Effective January 2,2014,Moldaur Co.adopted the accounting principle of expensing advertising and promotion costs as they are incurred.Previously,advertising and promotion costs applicable to future periods were recorded in prepaid expenses.Moldaur can justify the change,which was made for both financial statement and income tax reporting purposes.Moldaur's prepaid advertising and promotion costs totaled $250,000 at December 31,2013.Assume that the income tax rate is 40 percent for 2013 and 2014.The adjustment for the effect of the change in accounting principle should result in a net charge against income in the income statement for 2014 of

A) $0.

B) $100,000.

C) $150,000.

D) $250,000.

A) $0.

B) $100,000.

C) $150,000.

D) $250,000.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

31

McCartney Corp.reports on a calendar-year basis.Its 2013 and 2014 financial statements contained the following errors: As a result of the above errors,2014 income would be

A) overstated by $4,000.

B) overstated by $24,000.

C) overstated by $22,000.

D) overstated by $16,000.

As a result of the above errors,2014 income would beA) overstated by $4,000.

B) overstated by $24,000.

C) overstated by $22,000.

D) overstated by $16,000.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

32

Crafter,Inc.receives subscription payments for annual (one year)subscriptions to its magazine.Payments are recorded as revenue when received.Amounts received but unearned at the end of each of the last three years are shown below: Crafter failed to record the unearned revenues in each of the three years.As a result of the omission,2014 income was

A) overstated by $146,000.

B) understated by $146,000.

C) understated by $26,000.

D) overstated by $26,000.

Crafter failed to record the unearned revenues in each of the three years.As a result of the omission,2014 income wasA) overstated by $146,000.

B) understated by $146,000.

C) understated by $26,000.

D) overstated by $26,000.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

33

Songtress Company bought a machine on January 1,2012,for $24,000,at which time it had an estimated useful life of eight years,with no residual value.Straight-line depreciation is used for all of Songtress' depreciable assets.On January 1,2014,the machine's estimated useful life was determined to be only six years from the acquisition date.Accordingly,the appropriate accounting change was made in 2014.Songtress' income tax rate was 40 percent in all the affected years.In Songtress' 2014 financial statements,how much should be reported as the cumulative effect on prior years because of the change in the estimated useful life of the machine?

A) $0

B) $1,200

C) $2,000

D) $2,800

A) $0

B) $1,200

C) $2,000

D) $2,800

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

34

On January 2,2012,Lynch Company acquired machinery at a cost of $800,000.This machinery was being depreciated by the double-declining-balance method over an estimated useful life of eight years,with no residual value.At the beginning of 2014,Lynch decided to change to the straight-line method of depreciation.Ignoring income tax considerations,the cumulative effect of this accounting change is

A) $0.

B) $100,000.

C) $155,556

D) $177,778

A) $0.

B) $100,000.

C) $155,556

D) $177,778

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

35

Newsman Co.made the following errors in counting its year-end physical inventories: As a result of the above undetected errors,2014 income was

A) understated by $18,000.

B) overstated by $198,000.

C) overstated by $18,000.

D) understated by $198,000.

As a result of the above undetected errors,2014 income wasA) understated by $18,000.

B) overstated by $198,000.

C) overstated by $18,000.

D) understated by $198,000.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

36

Badger Corporation purchased a machine for $132,000 on January 1,2011,and depreciated it by the straight-line method using an estimated useful life of eight years with no salvage value.On January 1,2014,Badger determined that the machine had a useful life of six years from the date of acquisition and will have a salvage value of $12,000.A change in estimate was made in 2014 to reflect these additional data.What amount should Badger record as the balance of the accumulated depreciation account for this machine at December 31,2014?

A) $73,000

B) $77,000

C) $61,250

D) $63,600

A) $73,000

B) $77,000

C) $61,250

D) $63,600

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

37

A change from an accelerated depreciation method to the straight-line depreciation method should be accounted for as a

A) change in accounting estimate.

B) change in accounting estimate effected by a change in accounting principle.

C) correction of an error.

D) a prior period adjustment.

A) change in accounting estimate.

B) change in accounting estimate effected by a change in accounting principle.

C) correction of an error.

D) a prior period adjustment.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

38

A change in the unit depletion rate would be accounted for as a

A) correction of an accounting error.

B) change in accounting principle.

C) change in accounting estimate.

D) change in accounting estimate effected through a change in accounting principle.

A) correction of an accounting error.

B) change in accounting principle.

C) change in accounting estimate.

D) change in accounting estimate effected through a change in accounting principle.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

39

On December 31,2014,Artistown Company appropriately changed to the FIFO cost method from the weighted-average cost method for financial statement and income tax purposes.The change will result in a $700,000 increase in the beginning inventory at January 1,2014.Assuming a 40 percent income tax rate and that no comparative financial statements for prior years are reported,the cumulative effect of this accounting change reported for the year ended December 31,2014,is

A) $700,000.

B) $350,000.

C) $420,000.

D) $280,000.

A) $700,000.

B) $350,000.

C) $420,000.

D) $280,000.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

40

Nevada Enterprises purchased a machine on January 2,2013,at a cost of $140,000.An additional $70,000 was spent for installation,but this amount was charged erroneously to repairs expense.The machine has a useful life of five years and a salvage value of $40,000.As a result of the error,

A) retained earnings at December 31,2014,was understated by $34,000 and 2014 income was overstated by $6,000.

B) retained earnings at December 31,2014,was understated by $42,000 and 2014 income was overstated by $6,000.

C) retained earnings at December 31,2014,was understated by $34,000 and 2014 income was overstated by $14,000.

D) 2013 income was understated by $70,000.

A) retained earnings at December 31,2014,was understated by $34,000 and 2014 income was overstated by $6,000.

B) retained earnings at December 31,2014,was understated by $42,000 and 2014 income was overstated by $6,000.

C) retained earnings at December 31,2014,was understated by $34,000 and 2014 income was overstated by $14,000.

D) 2013 income was understated by $70,000.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

41

In 2014,a company changed from the FIFO method of accounting for inventory to LIFO.The company's 2013 and 2014 comparative financial statements will reflect which method or methods? 2013 2014

A) LIFO LIFO

B) LIFO FIFO

C) FIFO FIFO

D) LIFO either LIFO or FIFO

A) LIFO LIFO

B) LIFO FIFO

C) FIFO FIFO

D) LIFO either LIFO or FIFO

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following should NOT be reported retroactively?

A) Use of an unacceptable accounting principle,then changing to an acceptable accounting principle

B) Correction of an overstatement of ending inventory made two years ago

C) Use of an unrealistic accounting estimate,then changing to a realistic estimate

D) Change from a good faith but erroneous estimate to a new estimate

A) Use of an unacceptable accounting principle,then changing to an acceptable accounting principle

B) Correction of an overstatement of ending inventory made two years ago

C) Use of an unrealistic accounting estimate,then changing to a realistic estimate

D) Change from a good faith but erroneous estimate to a new estimate

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

43

The September 30,2014,physical inventory of Pollack Corporation appropriately included $6,300 of merchandise purchased on account that was not recorded in purchases until October 2014.What effect will this error have on September 30,2014,assets,liabilities,retained earnings,and earnings for the year then ended,respectively?

A) Understate;no effect;overstate;overstate

B) No effect;overstate;understate;understate

C) No effect;understate;overstate;overstate

D) No effect;understate;understate;overstate

A) Understate;no effect;overstate;overstate

B) No effect;overstate;understate;understate

C) No effect;understate;overstate;overstate

D) No effect;understate;understate;overstate

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

44

In 2014,a company changed from the LIFO method of accounting for inventory to FIFO.The company's 2013 and 2014 comparative financial statements will reflect which method or methods? 2013 2014

A) LIFO LIFO

B) FIFO FIFO

C) LIFO FIFO

D) LIFO either LIFO or FIFO

A) LIFO LIFO

B) FIFO FIFO

C) LIFO FIFO

D) LIFO either LIFO or FIFO

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following is not an example of an accounting error,as distinguished from a change in accounting principle or change in accounting estimate?

A) Misstatement of assets,liabilities,or owners' equity

B) Incorrect classification of an expenditure as between expense and an asset

C) Failure to recognize accruals and deferrals

D) Recognition of a gain on disposal of fully depreciated property

A) Misstatement of assets,liabilities,or owners' equity

B) Incorrect classification of an expenditure as between expense and an asset

C) Failure to recognize accruals and deferrals

D) Recognition of a gain on disposal of fully depreciated property

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following is characteristic of a change in accounting principle?

A) Requires the reporting of pro forma amounts for prior periods

B) Does not affect the financial statements of prior periods

C) Never needs to be disclosed

D) Should be reported by retrospectively adjusting the financial statements for all years reported,and reporting the cumulative effect of the change in income for all preceding years as an adjustment to the beginning balance of retained earnings for the earliest year reported

A) Requires the reporting of pro forma amounts for prior periods

B) Does not affect the financial statements of prior periods

C) Never needs to be disclosed

D) Should be reported by retrospectively adjusting the financial statements for all years reported,and reporting the cumulative effect of the change in income for all preceding years as an adjustment to the beginning balance of retained earnings for the earliest year reported

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following is characteristic of a change in accounting estimate?

A) Requires the reporting of pro forma amounts for prior periods

B) Does not affect the financial statements of prior periods

C) Never needs to be disclosed

D) Should be reported by retrospectively adjusting the financial statements for all years reported,and reporting the cumulative effect of the change in income for all preceding years as an adjustment to the beginning balance of retained earnings for the earliest year reported

A) Requires the reporting of pro forma amounts for prior periods

B) Does not affect the financial statements of prior periods

C) Never needs to be disclosed

D) Should be reported by retrospectively adjusting the financial statements for all years reported,and reporting the cumulative effect of the change in income for all preceding years as an adjustment to the beginning balance of retained earnings for the earliest year reported

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following would cause income of the current period to be understated?

A) Capitalizing research and development costs

B) Failure to recognize unearned rent revenue

C) Changing from LIFO to FIFO for merchandise inventory

D) Understating estimates of asset residual values

A) Capitalizing research and development costs

B) Failure to recognize unearned rent revenue

C) Changing from LIFO to FIFO for merchandise inventory

D) Understating estimates of asset residual values

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

49

If,at the end of a period,Michaels Company erroneously excluded some goods from its ending inventory and also erroneously did NOT record the purchase of these goods in its accounting records,these errors would cause

A) no effect on the company's net income,working capital,and retained earnings.

B) the company's cost of goods available for sale,cost of goods sold,and net income to be understated.

C) the company's ending inventory,cost of goods available for sale,and retained earnings to be understated.

D) the company's ending inventory,cost of goods sold,and retained earnings to be understated.

A) no effect on the company's net income,working capital,and retained earnings.

B) the company's cost of goods available for sale,cost of goods sold,and net income to be understated.

C) the company's ending inventory,cost of goods available for sale,and retained earnings to be understated.

D) the company's ending inventory,cost of goods sold,and retained earnings to be understated.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

50

Ranger Company uses a periodic inventory system.If the company's beginning inventory in the current year is overstated,and that is the only error in the current year,then the company's income for the current year will be

A) understated and assets correct.

B) understated and assets overstated.

C) overstated and assets overstated.

D) understated and assets understated.

A) understated and assets correct.

B) understated and assets overstated.

C) overstated and assets overstated.

D) understated and assets understated.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

51

The ending inventory for Wyeth Company was overstated by $6,000 in 2014.The overstatement will cause Wyeth Company's

A) retained earnings to be understated on the 2014 balance sheet.

B) 2015 balance sheet not to be misstated

C) cost of goods sold to be overstated on the 2014 income statement.

D) cost of goods sold to be understated on the 2015 income statement.

A) retained earnings to be understated on the 2014 balance sheet.

B) 2015 balance sheet not to be misstated

C) cost of goods sold to be overstated on the 2014 income statement.

D) cost of goods sold to be understated on the 2015 income statement.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

52

Ending inventory for 2012 is overstated by $5,500 due to a faulty count and costing.The tax rate is 39%.Assume the same accounting methods for both financial reporting and taxes.The error is discovered late in 2014.The 2014 annual report shows the financial statements for 2012,2013,2014 on a comparative basis. Which of the following is correct regarding the reporting of this error in the 2014 annual report?

A) A journal entry is made to report the prior period adjustment,and the 2012 and 2013 statements are shown corrected.

B) No journal entry is needed,and the 2012 and 2013 statements are shown as they were in the 2013 annual report.

C) No journal entry is needed,and the 2012 and 2013 statements are shown corrected.

D) A journal entry is made to report the prior period adjustment,and the 2012 and 2013 statements are shown as they were in the 2013 annual report.

A) A journal entry is made to report the prior period adjustment,and the 2012 and 2013 statements are shown corrected.

B) No journal entry is needed,and the 2012 and 2013 statements are shown as they were in the 2013 annual report.

C) No journal entry is needed,and the 2012 and 2013 statements are shown corrected.

D) A journal entry is made to report the prior period adjustment,and the 2012 and 2013 statements are shown as they were in the 2013 annual report.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following types of errors will NOT self-correct in the next year?

A) Accrued expenses not recognized at year-end

B) Accrued revenues that have not been collected not recognized at year-end

C) Depreciation expense overstated for the year

D) Prepaid expenses not recognized at year-end

A) Accrued expenses not recognized at year-end

B) Accrued revenues that have not been collected not recognized at year-end

C) Depreciation expense overstated for the year

D) Prepaid expenses not recognized at year-end

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

54

A change in the estimated useful life of a building

A) is not allowed by generally accepted accounting principles.

B) affects the depreciation on the building beginning with the year of the change.

C) must be handled as a retroactive adjustment to all accounts affected,back to the year of the acquisition of the building.

D) creates a new account to be recognized on the income statement reflecting the difference in net income up to the beginning of the year of the change.

A) is not allowed by generally accepted accounting principles.

B) affects the depreciation on the building beginning with the year of the change.

C) must be handled as a retroactive adjustment to all accounts affected,back to the year of the acquisition of the building.

D) creates a new account to be recognized on the income statement reflecting the difference in net income up to the beginning of the year of the change.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following,if discovered by Somber Company in the accounting period subsequent to the period of occurrence,requires the company to report the correction of an error?

A) The estimate of the useful life of a depreciable asset should have been revised.

B) Capitalization of an expense

C) A change from declining-balance depreciation method to straight-line method

D) Change in percentage of sales used for determining bad debt expense

A) The estimate of the useful life of a depreciable asset should have been revised.

B) Capitalization of an expense

C) A change from declining-balance depreciation method to straight-line method

D) Change in percentage of sales used for determining bad debt expense

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following would NOT be accounted for as a change in accounting principle?

A) Change from the first-in,first-out method to the last-in,first-out method of inventory pricing

B) Change from the last-in,first-out method to the first-in,first-out method of inventory pricing

C) Change from completed-contract accounting to percentage-of-completion

D) Change from straight-line method to accelerated method of depreciation

A) Change from the first-in,first-out method to the last-in,first-out method of inventory pricing

B) Change from the last-in,first-out method to the first-in,first-out method of inventory pricing

C) Change from completed-contract accounting to percentage-of-completion

D) Change from straight-line method to accelerated method of depreciation

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

57

When a firm changed its method of accounting for inventory from LIFO to FIFO in 2014,it decided that the 2014 financial statements should be shown comparatively with the 2013 results. Which of the following statements concerning reporting the change in the retained earnings statement is correct?

A) Both the January 1,2013,and January 1,2014,retained earnings balances are reported at different amounts to reflect the effects of the change in earnings before those respective dates.

B) Only the January 1,2013,retained earnings balance is reported at a different amount to reflect the effects of the change in earnings.

C) Only the January 1,2014,retained earnings balance is reported at a different amount to reflect the effects of the change in earnings.

D) No direct change to retained earnings is needed since earnings for both years have been adjusted to reflect the change.

A) Both the January 1,2013,and January 1,2014,retained earnings balances are reported at different amounts to reflect the effects of the change in earnings before those respective dates.

B) Only the January 1,2013,retained earnings balance is reported at a different amount to reflect the effects of the change in earnings.

C) Only the January 1,2014,retained earnings balance is reported at a different amount to reflect the effects of the change in earnings.

D) No direct change to retained earnings is needed since earnings for both years have been adjusted to reflect the change.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following is a counterbalancing error?

A) Understated depletion expense

B) Bond premium underamortized

C) Prepaid expense adjusted incorrectly

D) Overstated depreciation expenses

A) Understated depletion expense

B) Bond premium underamortized

C) Prepaid expense adjusted incorrectly

D) Overstated depreciation expenses

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

59

On December 27,2014,Admission Company ordered merchandise for resale from Eviction,Inc. ,that cost $7,000 (terms cash within 10 days).Eviction shipped the merchandise f.o.b.shipping point on December 28,2014,and the goods arrived on January 2,2015.The invoice was received on December 30,2014.Admission Company did not record the purchase in 2014 and did not include the goods in ending inventory.The effects on Admission Company's 2014 financial statements were

A) income and owners' equity were correct;liabilities were incorrect,assets were correct.

B) income and owners' equity were correct;assets and liabilities were incorrect.

C) income,assets,liabilities,and owners' equity were correct.

D) income,assets,liabilities,and owners' equity were incorrect.

A) income and owners' equity were correct;liabilities were incorrect,assets were correct.

B) income and owners' equity were correct;assets and liabilities were incorrect.

C) income,assets,liabilities,and owners' equity were correct.

D) income,assets,liabilities,and owners' equity were incorrect.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

60

Queener Corporation uses a periodic inventory system and neglected to record a purchase of merchandise on account at year-end.This merchandise was omitted from the year-end physical count.How will these errors affect Queener's assets,liabilities,and stockholders' equity at year-end and net earnings for the year? Stockholders'

Assets Liabilities Equity Net Earnings

A) Understate Understate No effect No effect

B) Understate No effect Understate Understate

C) No effect Understate Overstate Overstate

D) No effect Overstate Understate Understate

Assets Liabilities Equity Net Earnings

A) Understate Understate No effect No effect

B) Understate No effect Understate Understate

C) No effect Understate Overstate Overstate

D) No effect Overstate Understate Understate

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

61

Baron Co.began operations on January 1,2011,at which time it acquired depreciable assets of $100,000.The assets have an estimated useful life of ten years and no salvage value.

In 2014,Baron Co.changed from the sum-of-the-years'-digits depreciation method to the straight-line depreciation method.

Required:

Determine the depreciation expense for 2014 and prepare the appropriate journal entry.

In 2014,Baron Co.changed from the sum-of-the-years'-digits depreciation method to the straight-line depreciation method.

Required:

Determine the depreciation expense for 2014 and prepare the appropriate journal entry.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following is not a justification for a change in depreciation methods?

A) A change in the estimated useful life of an asset as a result of unexpected obsolescence

B) A change in the pattern of receiving the estimated future benefits from an asset

C) To conform to the depreciation method prevalent in a particular industry

D) A change in the estimated future benefits from the asset

A) A change in the estimated useful life of an asset as a result of unexpected obsolescence

B) A change in the pattern of receiving the estimated future benefits from an asset

C) To conform to the depreciation method prevalent in a particular industry

D) A change in the estimated future benefits from the asset

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

63

Ideally,managers should make accounting changes only as a result of new experience or information,or due to changes in economic conditions that demand methods of accounting that more accurately reflect such changing conditions.Managers should be attempting to achieve the closest match between reporting and economic reality.

Identify motivations for managers to make accounting changes other than the goal of achieving congruence between reporting and economic reality.

Identify motivations for managers to make accounting changes other than the goal of achieving congruence between reporting and economic reality.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

64

On January 1,2011,Shine Services Inc.purchased a new machine for $600,000.The machine had an estimated useful life of eight years and a salvage value of $150,000.Shine elected to depreciate the machine using the double-declining-balance method.On January 1,2014,the company decided to change to straight-line depreciation.

Ignoring income tax considerations,prepare the entries to record

Ignoring income tax considerations,prepare the entries to record

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

65

Asuncion Company purchased some equipment on January 2,2011,for $24,000.The company used straight-line depreciation based on a ten-year estimated life with no residual value.During 2014,management decided that this equipment could be used only three more years and then would be replaced with a technologically superior model.What entry should the company make as of January 1,2014,to reflect this change?

A) No entry

B) Debit a Prior Period Adjustment account for $4,800 and credit accumulated depreciation for $4,800.

C) Debit Retained Earnings for $4,800 and credit accumulated depreciation for $4,800.

D) Debit Depreciation Expense for $4,800 and credit Accumulated Depreciation for $4,800.

A) No entry

B) Debit a Prior Period Adjustment account for $4,800 and credit accumulated depreciation for $4,800.

C) Debit Retained Earnings for $4,800 and credit accumulated depreciation for $4,800.

D) Debit Depreciation Expense for $4,800 and credit Accumulated Depreciation for $4,800.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

66

Elder Corporation decided to change its depreciation policy by (1)changing from double-declining-balance depreciation,and (2)changing the estimated useful life on all automobiles used in the business from five years to four years. Which of the following is correct concerning these two changes?

A) Both are changes in accounting principle.

B) Both are changes in accounting estimate.

C) One is an error correction,and one is change in accounting principle.

D) One is a change in estimate effected through a change in accounting principle,and one is a change in estimate.

A) Both are changes in accounting principle.

B) Both are changes in accounting estimate.

C) One is an error correction,and one is change in accounting principle.

D) One is a change in estimate effected through a change in accounting principle,and one is a change in estimate.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

67

For a company with a periodic inventory system,which of the following would cause income to be overstated in the period of occurrence?

A) Overestimating bad debt expense

B) Understating beginning inventory

C) Overstated purchases

D) Understated ending inventory

A) Overestimating bad debt expense

B) Understating beginning inventory

C) Overstated purchases

D) Understated ending inventory

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

68

Diamond Company changed from the completed-contract method of accounting for long-term contracts to the percentage-of-completion method,during 2014.Reported earnings in 2013 were $50,000,and the beginning 2013 retained earnings balance was $150,000.Net income for 2014 under the competed-contract method would have been $140,000.No dividends were declared during 2013 and 2014.

Required:

Prepare the 2013 and 2014 comparative retained earnings statements.

Required:Prepare the 2013 and 2014 comparative retained earnings statements.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

69

A company mistakenly expensed a $100,000 machine purchased January 1,2011.The machine has no salvage value and is expected to provide benefits for five years.The error was discovered in 2014.The company shows two years of comparative statements in its December 31 annual reports.In the company's 2013 and 2014 reports shown comparatively,what amounts would be shown as adjustments to the respective retained earnings balances? 2013 2014

A) $60,000 $40,000

B) $0 $40,000

C) $60,000 $0

D) $60,000 $20,000

A) $60,000 $40,000

B) $0 $40,000

C) $60,000 $0

D) $60,000 $20,000

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

70

A retailing firm changed from LIFO to FIFO in 2014.Inventory valuations for the two methods appear below:

Purchases in 2013 and 2014 were $60,000 in each year.

Using the information above,in the comparative 2013 and 2014 income statements,what amounts would be shown for cost of goods sold? 2013 2014

A) $50,000 $58,000

B) $51,000 $55,000

C) $50,000 $55,000

D) $51,000 $58,000

Purchases in 2013 and 2014 were $60,000 in each year.Using the information above,in the comparative 2013 and 2014 income statements,what amounts would be shown for cost of goods sold? 2013 2014

A) $50,000 $58,000

B) $51,000 $55,000

C) $50,000 $55,000

D) $51,000 $58,000

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

71

In 2014,a company discovered that $20,000 of equipment purchased on January 1,2011,was expensed in full.The equipment has a ten-year life,no residual value,and should have been depreciated on the straight-line basis.The error is corrected.As a result,the comparative 2013 and 2014 financial statements will show what amounts as adjustments to the beginning balances of retained earnings dated: 1/1/2013 1/1/2014

A) $14,000 $14,000

B) $16,000 $0

C) $0 $14,000

D) $16,000 $14,000

A) $14,000 $14,000

B) $16,000 $0

C) $0 $14,000

D) $16,000 $14,000

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

72

FASB ASC Topic 250 (Presentation-Accounting Changes and Error Corrections,requires that voluntary changes in accounting principles be reported retrospectively.The standard recognizes that such retrospective restatement is not always practical.

Required:

Required:

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

73

Witherfork Company was recently acquired by a new owner who has decided to correct the prior accounting records during the current reporting period ending December 31,2014.The accounts have been partially adjusted but have not been closed for 2014.The following items have been discovered:

Required:

Provide the appropriate entry to record any change or correction and give any adjusting entry needed in each instance at the end of 2014.Show computations for entries made,and provide explanations for situations for which no entry is required.

Required:Provide the appropriate entry to record any change or correction and give any adjusting entry needed in each instance at the end of 2014.Show computations for entries made,and provide explanations for situations for which no entry is required.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

74

Chiclet Company decides at the beginning of 2014 to adopt the FIFO method of inventory valuation.The company had been using the LIFO method for financial and tax reporting since it inception on January 1,2012.The profit-sharing agreement was in place for all years prior to the year of change,2014.Payments under this agreement are not an inventoriable cost. Which of the following statements regarding the accounting for the profit-sharing agreement in connection with the change from LIFO to FIFO is correct?

A) The effects of the change in accounting principle on the profit-sharing agreement must be treated retrospectively.

B) The effects of the change in accounting principle on the profit-sharing agreement should be reported only in the period in which the change in accounting principle was made.