Deck 12: Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

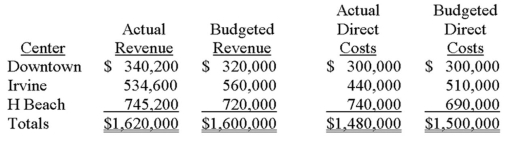

Management of Children Are Precious (CAP), an operator of day-care facilities, wants the company's profit to be subdivided by center. The firm's accountant has provided the following data:  CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.

CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.

If advertising expense were allocated to centers based on actual center profitability, the amount of advertising expense allocated to the Irvine center would be closest to:

A) $19,800.

B) $21,000.

C) $30,000.

D) $40,543.

E) None of the other answers are correct.

CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.If advertising expense were allocated to centers based on actual center profitability, the amount of advertising expense allocated to the Irvine center would be closest to:

A) $19,800.

B) $21,000.

C) $30,000.

D) $40,543.

E) None of the other answers are correct.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Management of Children Are Precious (CAP), an operator of day-care facilities, wants the company's profit to be subdivided by center. The firm's accountant has provided the following data:  CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.

CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.

Assume that management used the allocation base that is most influenced by advertising effort and consistent with sound managerial accounting practices. How much advertising would be allocated to the Irvine center?

A) $17,838.

B) $19,800.

C) $20,000.

D) $20,400.

E) $21,000.

CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.Assume that management used the allocation base that is most influenced by advertising effort and consistent with sound managerial accounting practices. How much advertising would be allocated to the Irvine center?

A) $17,838.

B) $19,800.

C) $20,000.

D) $20,400.

E) $21,000.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

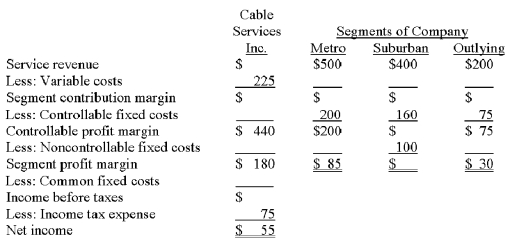

County Cable Services Inc. is organized in three segments: Metro, Suburban, and Outlying. Data for the company and for these segments follow.

Variable costs as a percentage of service revenue are: Metro, 20%; Suburban, 18.75%; and Outlying, 25%.

Required:

A. Complete the segmented income statement for County Cable.

B. Evaluate the three segment managers for consideration of a pay raise. Base the managers' performance on (1) absolute dollars of the appropriate profit measure, and (2) the appropriate profit measure as a percentage of service revenue. What causes any difference in rankings between the two approaches?

Variable costs as a percentage of service revenue are: Metro, 20%; Suburban, 18.75%; and Outlying, 25%.

Required:

A. Complete the segmented income statement for County Cable.

B. Evaluate the three segment managers for consideration of a pay raise. Base the managers' performance on (1) absolute dollars of the appropriate profit measure, and (2) the appropriate profit measure as a percentage of service revenue. What causes any difference in rankings between the two approaches?

Question

Question

Question

Question

Question

Question

Question

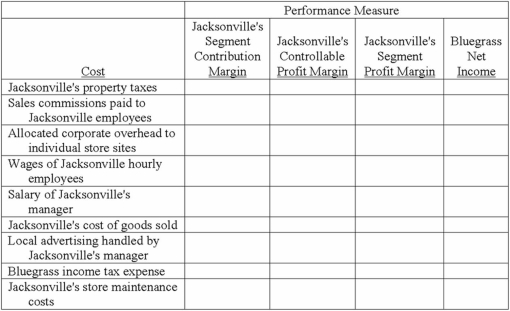

Bluegrass, Inc., which is headquartered in Atlanta, operates a chain of 225 clothing stores throughout the United States. Consider the costs that appear in the following table, many of which pertain to the company's sole operation in Jacksonville, Florida:

Specify store maintenance as a fixed costs. Adopt the following language." Jacksonville's store maintenance costs as agreed upon in yearly maintenance contract negotiated by Jacksonville's manager."

Required:

Analyze each of the costs and determine whether the cost affects Jacksonville's segment contribution margin, controllable profit margin, and segment profit margin, and/or the net income of Bluegrass, Inc. Place an "X" in the appropriate cell(s).

Specify store maintenance as a fixed costs. Adopt the following language." Jacksonville's store maintenance costs as agreed upon in yearly maintenance contract negotiated by Jacksonville's manager."

Required:

Analyze each of the costs and determine whether the cost affects Jacksonville's segment contribution margin, controllable profit margin, and segment profit margin, and/or the net income of Bluegrass, Inc. Place an "X" in the appropriate cell(s).

Question

Question

Question

Question

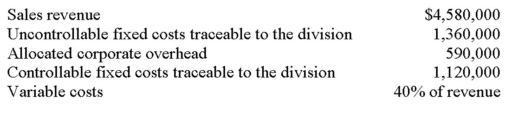

The following selected data relate to the Idaho Division of Far West Enterprises (FWE):

Required:

A. Compute the following for the Idaho Division:

1. Segment contribution margin.

2. Controllable profit margin.

3. Segment profit margin.

B. Which of the three preceding measures should be used when evaluating the Idaho Division as an investment of FWE's resources? Why?

C. Assume that management made the decision to prepare a segmented income statement that reflected Idaho's five operating departments. Would all $1,120,000 of the controllable fixed costs be easily traced to the departments? Briefly explain.

D. Which of the five-dollar amounts presented in the body of the problem would be used in computing the income before taxes of Far West Enterprises?

Required:

A. Compute the following for the Idaho Division:

1. Segment contribution margin.

2. Controllable profit margin.

3. Segment profit margin.

B. Which of the three preceding measures should be used when evaluating the Idaho Division as an investment of FWE's resources? Why?

C. Assume that management made the decision to prepare a segmented income statement that reflected Idaho's five operating departments. Would all $1,120,000 of the controllable fixed costs be easily traced to the departments? Briefly explain.

D. Which of the five-dollar amounts presented in the body of the problem would be used in computing the income before taxes of Far West Enterprises?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/72

Play

Full screen (f)

Deck 12: Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

1

Decentralized firms can delegate authority by structuring an organization into responsibility centers. Which of the following organizational segments is most like a totally independent, standalone business where managers are expected to "make it on their own"?

A) Cost center.

B) Revenue center.

C) Profit center.

D) Investment center.

E) Contribution center.

A) Cost center.

B) Revenue center.

C) Profit center.

D) Investment center.

E) Contribution center.

D

2

A cost center manager does not have the ability to produce revenue.

True

3

Performance reports help managers use management by exception and effectively control operations.

True

4

A profit center manager:

A) does not have the ability to produce revenue.

B) may be involved with the sale of new marketing programs to clients.

C) would normally be held accountable for producing an adequate return on invested capital.

D) often oversees divisional operations.

E) may be the manager who oversees the operations of a retail store.

A) does not have the ability to produce revenue.

B) may be involved with the sale of new marketing programs to clients.

C) would normally be held accountable for producing an adequate return on invested capital.

D) often oversees divisional operations.

E) may be the manager who oversees the operations of a retail store.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

5

An allocation base for a cost pool should ideally be a cost object.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

6

An investment center manager:

A) does not have the ability to produce revenue.

B) may be involved with the sale of new marketing programs to clients.

C) would normally be held accountable for producing an adequate return on invested capital.

D) often oversees divisional operations.

E) may be the manager who oversees the operations of a retail store.

A) does not have the ability to produce revenue.

B) may be involved with the sale of new marketing programs to clients.

C) would normally be held accountable for producing an adequate return on invested capital.

D) often oversees divisional operations.

E) may be the manager who oversees the operations of a retail store.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

7

When managers of subunits throughout an organization strive to achieve the goals set by top management, the result is:

A) goal congruence.

B) planning and control.

C) responsibility accounting.

D) delegation of decision making.

E) strategic control.

A) goal congruence.

B) planning and control.

C) responsibility accounting.

D) delegation of decision making.

E) strategic control.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

8

The concepts and tools used to measure the performance of people and departments are known as:

A) goal congruence.

B) planning and control.

C) responsibility accounting.

D) delegation of decision making.

E) strategic control.

A) goal congruence.

B) planning and control.

C) responsibility accounting.

D) delegation of decision making.

E) strategic control.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

9

A manufacturer's raw-material purchasing department would likely be classified as a:

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

10

The Asian Division of a multinational manufacturing organization would likely be classified as a:

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

11

The typical balanced scorecard is best described as containing both financial and nonfinancial performance measures.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

12

Higgins Corporation is in the process of overhauling the performance evaluation system for its Los Angeles manufacturing division, which produces and sells parts that are popular in the aerospace industry. Which of the following is least likely to be chosen to evaluate the overall operations of the Los Angeles division?

A) Cost center.

B) Responsibility center.

C) Profit center.

D) Investment center.

E) The profit center and investment center are equally unlikely to be chosen.

A) Cost center.

B) Responsibility center.

C) Profit center.

D) Investment center.

E) The profit center and investment center are equally unlikely to be chosen.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

13

The Telemarketing Department of a residential remodeling company would most likely be evaluated as a:

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

14

A cost center manager:

A) does not have the ability to produce revenue.

B) may be involved with the sale of new marketing programs to clients.

C) would normally be held accountable for producing an adequate return on invested capital.

D) often oversees divisional operations.

E) may be the manager who oversees the operations of a retail store.

A) does not have the ability to produce revenue.

B) may be involved with the sale of new marketing programs to clients.

C) would normally be held accountable for producing an adequate return on invested capital.

D) often oversees divisional operations.

E) may be the manager who oversees the operations of a retail store.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is not an example of a responsibility center?

A) Cost center.

B) Revenue center.

C) Profit center.

D) Investment center.

E) Contribution center.

A) Cost center.

B) Revenue center.

C) Profit center.

D) Investment center.

E) Contribution center.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

16

If the head of a hotel's food and beverage operation is held accountable for revenues and costs, the food and beverage operation would be considered a (n):

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

17

A revenue center manager:

A) does not have the ability to produce revenue.

B) may be involved with the sale of new marketing programs to clients.

C) would normally be held accountable for producing an adequate return on invested capital.

D) often oversees divisional operations.

E) may be the manager who oversees the operations of a retail store.

A) does not have the ability to produce revenue.

B) may be involved with the sale of new marketing programs to clients.

C) would normally be held accountable for producing an adequate return on invested capital.

D) often oversees divisional operations.

E) may be the manager who oversees the operations of a retail store.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

18

Common costs are charged to a company's operating segments when preparing a segmented income statement.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following would have a low likelihood of being organized as a profit center?

A) A movie theater of a company that operates a chain of theaters.

B) A maintenance department that charges users for its services.

C) The billing department of an Internet Services Provider (ISP).

D) The mayor's office in a large city.

E) Both the billing department of an Internet Services Provider (ISP) and the mayor's office in a large city.

A) A movie theater of a company that operates a chain of theaters.

B) A maintenance department that charges users for its services.

C) The billing department of an Internet Services Provider (ISP).

D) The mayor's office in a large city.

E) Both the billing department of an Internet Services Provider (ISP) and the mayor's office in a large city.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

20

A responsibility center in which the manager is held accountable for the profitable use of assets and capital is commonly known as a (n):

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

A) cost center.

B) revenue center.

C) profit center.

D) investment center.

E) contribution center.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is an appropriate base to distribute the cost of building depreciation to responsibility centers?

A) Number of employees in the responsibility centers.

B) Budgeted sales dollars of the responsibility centers.

C) Square feet occupied by the responsibility centers.

D) Budgeted net income of the responsibility centers.

E) Total budgeted direct operating costs of the responsibility centers.

A) Number of employees in the responsibility centers.

B) Budgeted sales dollars of the responsibility centers.

C) Square feet occupied by the responsibility centers.

D) Budgeted net income of the responsibility centers.

E) Total budgeted direct operating costs of the responsibility centers.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

22

Distinguishing between controllable and noncontrollable costs on a performance report may result in:

A) an increase in the effectiveness of a cost management system.

B) a decrease in goal congruent behavior by managers.

C) an increase in the quality of performance information.

D) an increase in feelings of blame by managers.

E) an increase in the effectiveness of a cost management system and an increase in the quality of performance information.

A) an increase in the effectiveness of a cost management system.

B) a decrease in goal congruent behavior by managers.

C) an increase in the quality of performance information.

D) an increase in feelings of blame by managers.

E) an increase in the effectiveness of a cost management system and an increase in the quality of performance information.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

23

Management of Children Are Precious (CAP), an operator of day-care facilities, wants the company's profit to be subdivided by center. The firm's accountant has provided the following data: CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.

If advertising expense were allocated to centers based on actual center profitability, the amount of advertising expense allocated to the Irvine center would be closest to:

A) $19,800.

B) $21,000.

C) $30,000.

D) $40,543.

E) None of the other answers are correct.

CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.If advertising expense were allocated to centers based on actual center profitability, the amount of advertising expense allocated to the Irvine center would be closest to:

A) $19,800.

B) $21,000.

C) $30,000.

D) $40,543.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

24

Henry Company is preparing a segmented income statement, subdivided into departments (billing, purchasing, and telemarketing). Which of the following choices correctly describes the accounting treatment of the firm's compensation cost for key executives (president and vice-presidents)?

A) The cost is charged to the departments.

B) The cost is not charged to the departments because, although easily traceable to the departments, it is not controllable at the departmental level.

C) The cost is not charged to the departments because, although controllable at the departmental level, it is not easily traceable to the departments.

D) The cost is not charged to the departments because it is both easily traceable to the departments and controllable by the departments.

E) The cost is not charged to the departments because it is neither easily traceable to the departments nor controllable by the departments.

A) The cost is charged to the departments.

B) The cost is not charged to the departments because, although easily traceable to the departments, it is not controllable at the departmental level.

C) The cost is not charged to the departments because, although controllable at the departmental level, it is not easily traceable to the departments.

D) The cost is not charged to the departments because it is both easily traceable to the departments and controllable by the departments.

E) The cost is not charged to the departments because it is neither easily traceable to the departments nor controllable by the departments.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

25

Responsibility accounting systems strive to:

A) place blame on guilty individuals.

B) provide information to managers.

C) hold managers accountable for both controllable and noncontrollable costs.

D) identify unfavorable variances.

E) provide information so that managers can make decisions that are in the best interest of their individual centers rather than in the best interests of the firm as a whole.

A) place blame on guilty individuals.

B) provide information to managers.

C) hold managers accountable for both controllable and noncontrollable costs.

D) identify unfavorable variances.

E) provide information so that managers can make decisions that are in the best interest of their individual centers rather than in the best interests of the firm as a whole.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

26

A cost pool is:

A) a collection of homogeneous costs to be assigned.

B) almost always the combined result of decisions made by different responsibility center managers.

C) the primary function of a responsibility accounting system.

D) the amount of cost that has been allocated, say, 10%, to a user department.

E) the tool used to allocate cost dollars to user departments.

A) a collection of homogeneous costs to be assigned.

B) almost always the combined result of decisions made by different responsibility center managers.

C) the primary function of a responsibility accounting system.

D) the amount of cost that has been allocated, say, 10%, to a user department.

E) the tool used to allocate cost dollars to user departments.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

27

West Coast Electronics (WCE) operates 87 stores and has three divisions: California, Oregon, and Washington. Which of the following costs would not appear on Oregon's portion of WCE's segmented income statement?

A) Costs related to statewide advertising contracts, negotiated by Oregon's divisional manager.

B) Variable sales commissions paid to Oregon's salespeople.

C) Compensation paid to Oregon's chief operating officer, as determined by WCE's management.

D) Oregon's allocated share of general WCE corporate overhead.

E) Compensation paid to Oregon's chief operating officer, as determined by WCE's management and Oregon's allocated share of general WCE corporate overhead.

A) Costs related to statewide advertising contracts, negotiated by Oregon's divisional manager.

B) Variable sales commissions paid to Oregon's salespeople.

C) Compensation paid to Oregon's chief operating officer, as determined by WCE's management.

D) Oregon's allocated share of general WCE corporate overhead.

E) Compensation paid to Oregon's chief operating officer, as determined by WCE's management and Oregon's allocated share of general WCE corporate overhead.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

28

Cost pools should be charged to responsibility centers by using:

A) budgeted amounts of allocation bases because the cost allocation to one responsibility center should influence the allocations to others.

B) budgeted amounts of allocation bases because the cost allocation to one responsibility center should not influence the allocations to others.

C) actual amounts of allocation bases because the cost allocation to one responsibility center should influence the allocations to others.

D) actual amounts of allocation bases because the cost allocation to one responsibility center should not influence the allocations to others.

E) some other approach.

A) budgeted amounts of allocation bases because the cost allocation to one responsibility center should influence the allocations to others.

B) budgeted amounts of allocation bases because the cost allocation to one responsibility center should not influence the allocations to others.

C) actual amounts of allocation bases because the cost allocation to one responsibility center should influence the allocations to others.

D) actual amounts of allocation bases because the cost allocation to one responsibility center should not influence the allocations to others.

E) some other approach.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

29

Kel-Leigh Corporation, with operations throughout the country, will soon allocate corporate overhead to the firm's various responsibility centers. Which of the following is definitely not a cost object in this situation?

A) The maintenance department.

B) Product no. 675.

C) Kelly Corporation.

D) The Midwest division.

E) The telemarketing center.

A) The maintenance department.

B) Product no. 675.

C) Kelly Corporation.

D) The Midwest division.

E) The telemarketing center.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

30

Common costs:

A) are not easily related to a segment's activities.

B) are easily related to a segment's activities.

C) are charged to a company's operating segments when preparing a segmented income statement.

D) are not charged to a company's operating segments when preparing a segmented income statement.

E) are not easily related to a segment's activities and also are not charged to a company's operating segments when preparing a segmented income statement.

A) are not easily related to a segment's activities.

B) are easily related to a segment's activities.

C) are charged to a company's operating segments when preparing a segmented income statement.

D) are not charged to a company's operating segments when preparing a segmented income statement.

E) are not easily related to a segment's activities and also are not charged to a company's operating segments when preparing a segmented income statement.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

31

Leisure Time owns six hotels in Hawaii, collectively known as the Hawaiian Division. The various hotels, including the Surf & Sun, have operating departments (such as Maintenance, Housekeeping, and Food and Beverage) that are evaluated as either cost centers or profit centers. The Food and Beverage Department, for example, is a profit center, with activities divided into three segments: Banquets and Catering, Restaurants, and Kitchen. If Leisure Time uses a performance-reporting system that is based on responsibility accounting, which of the following disclosures is likely to occur?

A) The detailed operating costs of the Surf & Sun's Kitchen Department will appear on the Hawaiian Division's performance report.

B) The Food and Beverage Department's profit will appear on Kitchen's performance report.

C) The profit of the Surf & Sun hotel will appear on the Hawaiian Division's performance report.

D) The Food and Beverage profit at the Surf & Sun will appear on Leisure Time's performance report.

E) The profit of the Surf & Sun hotel will appear on Food and Beverage's performance report.

A) The detailed operating costs of the Surf & Sun's Kitchen Department will appear on the Hawaiian Division's performance report.

B) The Food and Beverage Department's profit will appear on Kitchen's performance report.

C) The profit of the Surf & Sun hotel will appear on the Hawaiian Division's performance report.

D) The Food and Beverage profit at the Surf & Sun will appear on Leisure Time's performance report.

E) The profit of the Surf & Sun hotel will appear on Food and Beverage's performance report.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

32

For a company that uses responsibility accounting, which of the following costs is least likely to appear on a performance report of an assembly-line supervisor?

A) Direct materials used.

B) Departmental supplies.

C) Assembly-line labor.

D) Repairs and maintenance.

E) Assembly-line facilities depreciation.

A) Direct materials used.

B) Departmental supplies.

C) Assembly-line labor.

D) Repairs and maintenance.

E) Assembly-line facilities depreciation.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

33

The difference between the profit margin controllable by a segment manager and the segment profit margin is caused by:

A) variable operating expenses.

B) allocated common expenses.

C) fixed expenses controllable by the segment manager.

D) fixed expenses traceable to the segment but controllable by others.

E) sales revenue.

A) variable operating expenses.

B) allocated common expenses.

C) fixed expenses controllable by the segment manager.

D) fixed expenses traceable to the segment but controllable by others.

E) sales revenue.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

34

Performance reports help managers:

A) use management by exception and effectively control operations.

B) decide whether a cost, profit, or investment center framework is appropriate.

C) design their organizational hierarchy.

D) pinpoint trouble spots.

E) use management by exception and effectively control operations and pinpoint trouble spots.

A) use management by exception and effectively control operations.

B) decide whether a cost, profit, or investment center framework is appropriate.

C) design their organizational hierarchy.

D) pinpoint trouble spots.

E) use management by exception and effectively control operations and pinpoint trouble spots.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

35

Controllable costs, as used in a responsibility accounting system, consist of:

A) only fixed costs.

B) only direct materials and direct labor.

C) those costs that a manager can influence in the time period under review.

D) those costs about which a manager has some knowledge.

E) those costs that are influenced by parties external to the organization.

A) only fixed costs.

B) only direct materials and direct labor.

C) those costs that a manager can influence in the time period under review.

D) those costs about which a manager has some knowledge.

E) those costs that are influenced by parties external to the organization.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

36

The profit margin controllable by the segment manager would not include:

A) variable operating expenses.

B) fixed expenses controllable by the segment manager.

C) a share of the company's common fixed expenses.

D) income tax expense.

E) a share of the company's common fixed expenses and income tax expense.

A) variable operating expenses.

B) fixed expenses controllable by the segment manager.

C) a share of the company's common fixed expenses.

D) income tax expense.

E) a share of the company's common fixed expenses and income tax expense.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

37

An allocation base for a cost pool should ideally be:

A) machine hours.

B) a cost object.

C) a common cost.

D) a cost driver.

E) direct labor, either cost or hours.

A) machine hours.

B) a cost object.

C) a common cost.

D) a cost driver.

E) direct labor, either cost or hours.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

38

Consider the following statements about performance reports:

I) Performance reports provide feedback to managers and allow them to better control operations.

II) Many performance reports have budget, actual, and variance data.

III) Performance reports are often structured around a firm's organizational hierarchy-that is, data relating to lower-level units (e.g., departments) are combined and flow into higher-level units (e.g., stores).

Which of the above statements is (are) true?

A) I only.

B) I and II.

C) I and III.

D) II and III.

E) I, II, and III.

I) Performance reports provide feedback to managers and allow them to better control operations.

II) Many performance reports have budget, actual, and variance data.

III) Performance reports are often structured around a firm's organizational hierarchy-that is, data relating to lower-level units (e.g., departments) are combined and flow into higher-level units (e.g., stores).

Which of the above statements is (are) true?

A) I only.

B) I and II.

C) I and III.

D) II and III.

E) I, II, and III.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

39

A cost object is:

A) a collection of costs to be assigned.

B) a responsibility center, product, or service to which cost is to be assigned.

C) the tool used to charge cost dollars to user departments.

D) the primary function of a responsibility accounting system.

E) a common cost.

A) a collection of costs to be assigned.

B) a responsibility center, product, or service to which cost is to be assigned.

C) the tool used to charge cost dollars to user departments.

D) the primary function of a responsibility accounting system.

E) a common cost.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

40

Management of Children Are Precious (CAP), an operator of day-care facilities, wants the company's profit to be subdivided by center. The firm's accountant has provided the following data: CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.

Assume that management used the allocation base that is most influenced by advertising effort and consistent with sound managerial accounting practices. How much advertising would be allocated to the Irvine center?

A) $17,838.

B) $19,800.

C) $20,000.

D) $20,400.

E) $21,000.

CAP's advertising, which is handled by the home office, is not reflected in the preceding figures and amounted to $60,000.Assume that management used the allocation base that is most influenced by advertising effort and consistent with sound managerial accounting practices. How much advertising would be allocated to the Irvine center?

A) $17,838.

B) $19,800.

C) $20,000.

D) $20,400.

E) $21,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

41

An increasingly popular approach that integrates financial and customer performance measures with measures in the areas of internal operations and learning and growth is known as:

A) the integrated performance measurement tool (IPMT).

B) the balanced scorecard.

C) gain sharing.

D) cycle efficiency.

E) overall quality assessment (OQA).

A) the integrated performance measurement tool (IPMT).

B) the balanced scorecard.

C) gain sharing.

D) cycle efficiency.

E) overall quality assessment (OQA).

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

42

Sand Fly Corporation operates two stores: J and K. The following information relates to J: J's segment contribution margin is:

A) $345,000.

B) $425,000.

C) $620,000.

D) $700,000.

E) $745,000.

A) $345,000.

B) $425,000.

C) $620,000.

D) $700,000.

E) $745,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

43

The following information was taken from the segmented income statement of Restin, Inc., and the company's three divisions: In addition, the company incurred common fixed costs of $18,000.

Assuming use of a responsibility accounting system, which of the following amounts should be used to evaluate the performance of the Los Angeles division manager?

A) $4,000.

B) $8,000.

C) $10,000.

D) $25,000.

E) $90,000.

Assuming use of a responsibility accounting system, which of the following amounts should be used to evaluate the performance of the Los Angeles division manager?

A) $4,000.

B) $8,000.

C) $10,000.

D) $25,000.

E) $90,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

44

The following information was taken from the segmented income statement of Restin, Inc., and the company's three divisions: In addition, the company incurred common fixed costs of $18,000.

Which of the following amounts should be used to evaluate whether Restin, Inc., should continue to invest company resources in the Los Angeles division?

A) $4,000.

B) $8,000.

C) $10,000.

D) $25,000.

E) $90,000.

Which of the following amounts should be used to evaluate whether Restin, Inc., should continue to invest company resources in the Los Angeles division?

A) $4,000.

B) $8,000.

C) $10,000.

D) $25,000.

E) $90,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

45

On a segmented income statement, common fixed expenses will have an effect on a company's:

A) segment contribution margin.

B) profit margin controllable by the segment manager.

C) segment profit margin.

D) segment contribution margin and segment profit margin.

E) None of the other answers are correct.

A) segment contribution margin.

B) profit margin controllable by the segment manager.

C) segment profit margin.

D) segment contribution margin and segment profit margin.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

46

The following information was taken from the segmented income statement of Restin, Inc., and the company's three divisions: In addition, the company incurred common fixed costs of $18,000.

The profit margin controllable by the Central Valley segment manager is:

A) $32,000.

B) $44,000.

C) $50,000.

D) $75,000.

E) $145,000.

The profit margin controllable by the Central Valley segment manager is:

A) $32,000.

B) $44,000.

C) $50,000.

D) $75,000.

E) $145,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following balanced-scorecard perspectives is influenced by a company's vision and strategy?

A) Financial.

B) Customer.

C) Internal operations.

D) Learning and growth.

E) All of the other answers are correct.

A) Financial.

B) Customer.

C) Internal operations.

D) Learning and growth.

E) All of the other answers are correct.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following would be the best measure on which to base a segment manager's performance evaluation for purposes of granting a bonus?

A) Segment sales revenue.

B) Segment contribution margin.

C) Profit margin controllable by the segment manager.

D) Segment profit margin.

E) Segment net income.

A) Segment sales revenue.

B) Segment contribution margin.

C) Profit margin controllable by the segment manager.

D) Segment profit margin.

E) Segment net income.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

49

Guernsey Retail has three stores in Wisconsin. Which of the following costs would likely be excluded when computing the profit margin controllable by store no. 3's manager?

A) Hourly labor costs incurred by personnel at store no. 3.

B) Property taxes attributable to store no. 3.

C) The salary of Guernsey's president.

D) The salary of store no. 3's manager.

E) All answers except hourly labor costs incurred by personnel at store no. 3 are correct.

A) Hourly labor costs incurred by personnel at store no. 3.

B) Property taxes attributable to store no. 3.

C) The salary of Guernsey's president.

D) The salary of store no. 3's manager.

E) All answers except hourly labor costs incurred by personnel at store no. 3 are correct.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

50

The following information was taken from the segmented income statement of Restin, Inc., and the company's three divisions: In addition, the company incurred common fixed costs of $18,000.

Assume that the Los Angeles division increases its promotion expense, a controllable fixed cost, by $10,000. As a result, revenues increased by $50,000. If variable expenses are tied directly to revenues, the new Los Angeles segment contribution margin is:

A) $12,500.

B) $22,500.

C) $32,500.

D) $50,000.

E) $60,000.

Assume that the Los Angeles division increases its promotion expense, a controllable fixed cost, by $10,000. As a result, revenues increased by $50,000. If variable expenses are tied directly to revenues, the new Los Angeles segment contribution margin is:

A) $12,500.

B) $22,500.

C) $32,500.

D) $50,000.

E) $60,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

51

Swedish Cruise Lines (SCL), which operates in a very competitive marketplace, is considering four categories of performance measures: (1) profitability measures, (2) customer-satisfaction measures, (3) efficiency and quality measures, and (4) learning and growth measures. The company assigns one manager to each ship in its fleet to oversee the ship's general operations. If SCL desired to adopt a balanced-scorecard approach, which measures should the firm use in the evaluation of its managers?

A) 1.

B) 1, 2.

C) 2, 3.

D) 1, 2, 4.

E) 1, 2, 3, 4.

A) 1.

B) 1, 2.

C) 2, 3.

D) 1, 2, 4.

E) 1, 2, 3, 4.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

52

When using a balanced scorecard, which of the following is typically classified as an internal-operations performance measure?

A) Cash flow.

B) Number of customer complaints.

C) Employee training hours.

D) Number of employee suggestions.

E) Number of suppliers used.

A) Cash flow.

B) Number of customer complaints.

C) Employee training hours.

D) Number of employee suggestions.

E) Number of suppliers used.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

53

The following data relate to Department no. 3 of Tsing Corporation: On the basis of this information, Department no. 3's variable operating expenses are:

A) $80,000.

B) $160,000.

C) $230,000.

D) $390,000.

E) not determinable.

A) $80,000.

B) $160,000.

C) $230,000.

D) $390,000.

E) not determinable.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

54

Wirefree, Inc. provides a variety of telecommunications services to residential and commercial customers from its massive campus-like headquarters in suburban Orlando. For a number of years the firm's maintenance group has been organized as a cost center, rendering services free of charge to the company's user departments (sales, billing, accounting, marketing, research, and so forth).

Requests for maintenance have grown considerably, and demand is approaching the point where quality and timeliness of services provided are becoming an issue. As a result, management is studying whether the maintenance operation should be converted from a cost center to a profit center, with users to be billed for services performed.

Required:

A. Differentiate between a cost center and a profit center. How is each of these centers evaluated?

B. What will likely happen to the number of user service requests if the company makes the switch to a profit-center form of organization? Why?

C. Assume that a user department has requested a particular service, one that is time consuming and costly to perform. The maintenance group's actual cost incurred in providing this service is $17,800, and the user has agreed to pay $20,800 if the switch to a profit center is made. If this case is fairly typical within the firm, which of the two forms of organization (cost center or profit center) will result in a more responsive, service-oriented maintenance group for Wirefree? Why?

Requests for maintenance have grown considerably, and demand is approaching the point where quality and timeliness of services provided are becoming an issue. As a result, management is studying whether the maintenance operation should be converted from a cost center to a profit center, with users to be billed for services performed.

Required:

A. Differentiate between a cost center and a profit center. How is each of these centers evaluated?

B. What will likely happen to the number of user service requests if the company makes the switch to a profit-center form of organization? Why?

C. Assume that a user department has requested a particular service, one that is time consuming and costly to perform. The maintenance group's actual cost incurred in providing this service is $17,800, and the user has agreed to pay $20,800 if the switch to a profit center is made. If this case is fairly typical within the firm, which of the two forms of organization (cost center or profit center) will result in a more responsive, service-oriented maintenance group for Wirefree? Why?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

55

The typical balanced scorecard is best described as containing:

A) financial performance measures.

B) nonfinancial performance measures.

C) neither financial nor nonfinancial performance measures.

D) both financial and nonfinancial performance measures.

E) either financial or nonfinancial performance measures but not both.

A) financial performance measures.

B) nonfinancial performance measures.

C) neither financial nor nonfinancial performance measures.

D) both financial and nonfinancial performance measures.

E) either financial or nonfinancial performance measures but not both.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

56

When using a balanced scorecard, a company's market share is typically classified as an element of the firm's:

A) financial performance measures.

B) customer performance measures.

C) learning and growth performance measures.

D) internal-operations performance measures.

E) interdisciplinary performance measures.

A) financial performance measures.

B) customer performance measures.

C) learning and growth performance measures.

D) internal-operations performance measures.

E) interdisciplinary performance measures.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

57

The following data relate to Department no. 2 of Eva Corporation: On the basis of this information, fixed costs traceable to Department no. 2 but controllable by others are:

A) $160,000.

B) $220,000.

C) $260,000.

D) $480,000.

E) not determinable.

A) $160,000.

B) $220,000.

C) $260,000.

D) $480,000.

E) not determinable.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

58

Lead indicators guide management to:

A) take actions now that will have positive effects on organizational performance now.

B) take actions now that will have positive effects on organizational performance in the future.

C) take actions in the future that will have positive effects on organizational performance now.

D) take actions in the past that will have positive effects on organizational performance in the future.

E) pursue identical strategies as those implemented with lag indicators.

A) take actions now that will have positive effects on organizational performance now.

B) take actions now that will have positive effects on organizational performance in the future.

C) take actions in the future that will have positive effects on organizational performance now.

D) take actions in the past that will have positive effects on organizational performance in the future.

E) pursue identical strategies as those implemented with lag indicators.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

59

The following information was taken from the segmented income statement of Restin, Inc., and the company's three divisions: In addition, the company incurred common fixed costs of $18,000.

Bay Area's segment profit margin is:

A) $14,000.

B) $18,000.

C) $20,000.

D) $40,000.

E) $115,000.

Bay Area's segment profit margin is:

A) $14,000.

B) $18,000.

C) $20,000.

D) $40,000.

E) $115,000.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

60

A segment contribution margin would reflect the impact of:

A) variable operating expenses.

B) fixed expenses controllable by the segment manager.

C) fixed expenses traceable to the segment but controllable by others.

D) common fixed expenses.

E) All answers except common fixed expenses are correct.

A) variable operating expenses.

B) fixed expenses controllable by the segment manager.

C) fixed expenses traceable to the segment but controllable by others.

D) common fixed expenses.

E) All answers except common fixed expenses are correct.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

61

County Cable Services Inc. is organized in three segments: Metro, Suburban, and Outlying. Data for the company and for these segments follow.

Variable costs as a percentage of service revenue are: Metro, 20%; Suburban, 18.75%; and Outlying, 25%.

Required:

A. Complete the segmented income statement for County Cable.

B. Evaluate the three segment managers for consideration of a pay raise. Base the managers' performance on (1) absolute dollars of the appropriate profit measure, and (2) the appropriate profit measure as a percentage of service revenue. What causes any difference in rankings between the two approaches?

Variable costs as a percentage of service revenue are: Metro, 20%; Suburban, 18.75%; and Outlying, 25%.

Required:

A. Complete the segmented income statement for County Cable.

B. Evaluate the three segment managers for consideration of a pay raise. Base the managers' performance on (1) absolute dollars of the appropriate profit measure, and (2) the appropriate profit measure as a percentage of service revenue. What causes any difference in rankings between the two approaches?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

62

Balanced scorecards contain a number of factors that are important to the success of a business. These factors are often divided into four categories: financial, internal operations, customer, and learning and growth?

Consider the twelve factors that follow.

1. Market share

2. Earnings per share

3. Manufacturing cycle efficiency

4. Machine downtime

5. Number of patents held

6. Employee suggestions

7. Number of repeat sales

8. Levels of inventories held

9. Number of vendors used

10. Cash flow from operations

11. Employee training hours

12. Gross margin

Required:

Determine the proper classification (financial, internal operations, customer, and learning and growth?) for each of the twelve factors listed.

Consider the twelve factors that follow.

1. Market share

2. Earnings per share

3. Manufacturing cycle efficiency

4. Machine downtime

5. Number of patents held

6. Employee suggestions

7. Number of repeat sales

8. Levels of inventories held

9. Number of vendors used

10. Cash flow from operations

11. Employee training hours

12. Gross margin

Required:

Determine the proper classification (financial, internal operations, customer, and learning and growth?) for each of the twelve factors listed.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

63

Kirsten, Inc. operates a chain of 80 retail stores throughout the Northwest that specializes in the sale of sports equipment. The following costs relate to store no. 19 in Seattle, Washington:

1. Salary of store manager: $58,000

2. Allocated corporate overhead: $55,000

3. Cost of goods sold: $2,560,000

4. Landscaping and grounds costs (yearly contract): $6,800

5. Hourly wages of sales clerks: $343,000

6. Local advertising (negotiated by store manager): $76,000

7. Property taxes: $25,800

8. Sales commissions: $221,000

Required:

Which of the preceding costs would be used in computing:

A. Store no. 19's segment contribution margin?

B. Store no. 19's controllable profit margin?

C. Store no. 19's segment profit margin?

D. The net income of Kasten, Inc.?

1. Salary of store manager: $58,000

2. Allocated corporate overhead: $55,000

3. Cost of goods sold: $2,560,000

4. Landscaping and grounds costs (yearly contract): $6,800

5. Hourly wages of sales clerks: $343,000

6. Local advertising (negotiated by store manager): $76,000

7. Property taxes: $25,800

8. Sales commissions: $221,000

Required:

Which of the preceding costs would be used in computing:

A. Store no. 19's segment contribution margin?

B. Store no. 19's controllable profit margin?

C. Store no. 19's segment profit margin?

D. The net income of Kasten, Inc.?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

64

The performance reports generated by a responsibility accounting system often form a "hierarchy of performance reports." Explain what is meant by this term.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

65

Bob's Burgers and Such, a national fast-food chain, has experienced a number of problems in the past few years, and management is considering the adoption of a balanced scorecard as part of a turnaround effort.

Required:

A. Briefly explain the concept of a balanced scorecard. What general factors are included in a typical balanced scorecard?

B. Independent of your answer in requirement "A," assume that Bob's is very concerned about customer satisfaction. List four different (and specific) customer-satisfaction measures that may be appropriate for the firm (and for other fast-food providers).

C. Independent of requirement "A," assume that Bob's wants to return to former levels of profitability. List several financial measures that would allow management to assess success or failure with respect to the following goals: (1) pay creditors on a timely basis, (2) keep shareholders happy, and (3) improve profitability over time at stores that have been open at least one year.

Required:

A. Briefly explain the concept of a balanced scorecard. What general factors are included in a typical balanced scorecard?

B. Independent of your answer in requirement "A," assume that Bob's is very concerned about customer satisfaction. List four different (and specific) customer-satisfaction measures that may be appropriate for the firm (and for other fast-food providers).

C. Independent of requirement "A," assume that Bob's wants to return to former levels of profitability. List several financial measures that would allow management to assess success or failure with respect to the following goals: (1) pay creditors on a timely basis, (2) keep shareholders happy, and (3) improve profitability over time at stores that have been open at least one year.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

66

Segmented income statements are used to show revenues, expenses, and income for major parts of an organization.

Required:

A. Consider a regional chain of department stores that has two or three stores in each of several cities. One way to segment this business is geographically. Describe another way of segmenting the firm.

B. Segmented income statements often distinguish between "fixed expenses controllable by the segment manager" and "fixed expenses traceable to the segment, but controllable by others." Assume that the Cleveland district has three retail stores. Give two examples of each type of fixed cost.

C. Common costs create difficulties when preparing segmented income statements. Define "common costs," give an example for the regional chain of department stores, and explain in general terms why such costs create a problem.

Required:

A. Consider a regional chain of department stores that has two or three stores in each of several cities. One way to segment this business is geographically. Describe another way of segmenting the firm.

B. Segmented income statements often distinguish between "fixed expenses controllable by the segment manager" and "fixed expenses traceable to the segment, but controllable by others." Assume that the Cleveland district has three retail stores. Give two examples of each type of fixed cost.

C. Common costs create difficulties when preparing segmented income statements. Define "common costs," give an example for the regional chain of department stores, and explain in general terms why such costs create a problem.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

67

Consider the following situation:

The marketing manager of Gilroy, Inc. accepted a rush order for a nonstock item from a valued customer. The manager filed the necessary paperwork with the production department, and a production manager did the same with purchasing for needed raw materials. Unfortunately, a purchasing clerk temporarily lost the paperwork; by the time it was found, it was too late to order from Gilroy's regular supplier. A new supplier was located that quoted a very attractive price.

The materials soon arrived and were found to be of poor quality, thus giving rise to a favorable materials price variance, an unfavorable materials quantity variance, and an unfavorable labor efficiency variance. These latter two variances, based on normal practice, appeared on the production manager's performance report for the period just ended.

Required:

A. Given that the company uses a responsibility accounting system, should the production manager be penalized for poor performance? Briefly discuss, keeping in mind that a production manager is generally in a very good position to control material usage and labor efficiency.

B. Should anything be done to correct the situation? If "yes," briefly explain.

The marketing manager of Gilroy, Inc. accepted a rush order for a nonstock item from a valued customer. The manager filed the necessary paperwork with the production department, and a production manager did the same with purchasing for needed raw materials. Unfortunately, a purchasing clerk temporarily lost the paperwork; by the time it was found, it was too late to order from Gilroy's regular supplier. A new supplier was located that quoted a very attractive price.

The materials soon arrived and were found to be of poor quality, thus giving rise to a favorable materials price variance, an unfavorable materials quantity variance, and an unfavorable labor efficiency variance. These latter two variances, based on normal practice, appeared on the production manager's performance report for the period just ended.

Required:

A. Given that the company uses a responsibility accounting system, should the production manager be penalized for poor performance? Briefly discuss, keeping in mind that a production manager is generally in a very good position to control material usage and labor efficiency.

B. Should anything be done to correct the situation? If "yes," briefly explain.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

68

Bluegrass, Inc., which is headquartered in Atlanta, operates a chain of 225 clothing stores throughout the United States. Consider the costs that appear in the following table, many of which pertain to the company's sole operation in Jacksonville, Florida:

Specify store maintenance as a fixed costs. Adopt the following language." Jacksonville's store maintenance costs as agreed upon in yearly maintenance contract negotiated by Jacksonville's manager."

Required:

Analyze each of the costs and determine whether the cost affects Jacksonville's segment contribution margin, controllable profit margin, and segment profit margin, and/or the net income of Bluegrass, Inc. Place an "X" in the appropriate cell(s).

Specify store maintenance as a fixed costs. Adopt the following language." Jacksonville's store maintenance costs as agreed upon in yearly maintenance contract negotiated by Jacksonville's manager."

Required:

Analyze each of the costs and determine whether the cost affects Jacksonville's segment contribution margin, controllable profit margin, and segment profit margin, and/or the net income of Bluegrass, Inc. Place an "X" in the appropriate cell(s).

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

69

The allocation of costs gives rise to several unique terms. Briefly discuss the following: cost object, cost allocation base, and cost allocation.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

70

Bronze Life Corporation (BLC) manufactures decorative, sculpted accessories that are sold by interior decorators and home furnishing stores. The following situation concerns two BLC employees: Deborah Philbun, head of the company's Billing Department, and Gary Bitner, the firm's general manager.

Philbun's Billing Department makes heavy use of hourly employees and is evaluated as a cost center. Understanding the need for prompt collection of receivables, Philbun strives to run a first-class operation. Philbun also understands the need to contribute in a big way to BLC's financial performance so she continually strives to minimize Billing Department expenses.

Unfortunately, Philbun experienced a heated discussion with Bitner several weeks ago, the subject being the shoddy operation that she is running. Bitner complained loudly about the lack of timely billings to customers and the general lack of attention to detail, as many complaints have surfaced about erroneous invoices and customer statements.

Required:

A. What is meant by the term "responsibility accounting?"

B. What measure(s) of performance would companies normally use to evaluate a cost-center manager?

C. Does Bitner have a valid reason to be upset with Philbun? Given the nature of the Billing Department, did Philbun err in her quest to minimize expenses? Explain.

D. Is it likely that the Billing Department could be evaluated as a profit center? Why?

Philbun's Billing Department makes heavy use of hourly employees and is evaluated as a cost center. Understanding the need for prompt collection of receivables, Philbun strives to run a first-class operation. Philbun also understands the need to contribute in a big way to BLC's financial performance so she continually strives to minimize Billing Department expenses.

Unfortunately, Philbun experienced a heated discussion with Bitner several weeks ago, the subject being the shoddy operation that she is running. Bitner complained loudly about the lack of timely billings to customers and the general lack of attention to detail, as many complaints have surfaced about erroneous invoices and customer statements.

Required:

A. What is meant by the term "responsibility accounting?"

B. What measure(s) of performance would companies normally use to evaluate a cost-center manager?

C. Does Bitner have a valid reason to be upset with Philbun? Given the nature of the Billing Department, did Philbun err in her quest to minimize expenses? Explain.

D. Is it likely that the Billing Department could be evaluated as a profit center? Why?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

71

Fog City Retail operates a retail store in Phoenix, Las Vegas, and Portland. The following information relates to the Phoenix facility:

• The store sold 65,000 units at $18.00 each, after having purchased the units from various suppliers for $12.50. Phoenix salespeople are paid a 5% commission based on gross sales dollars.

• Phoenix's sales manager oversees the placement of local advertising contracts, which totaled $54,000 for the year. Local property taxes amounted to $14,500.

• The sales manager's $65,000 salary is set by Phoenix's store manager. In contrast, the store manager's $134,000 salary is determined by Fog City's vice president.

• Phoenix incurred $6,800 of other noncontrollable costs.

• Nontraceable (common) corporate overhead totaled $68,000.

Fog City's corporate headquarters is located in Portland, and the company uses responsibility accounting to evaluate performance.

Required:

Prepare a segmented income statement for the Phoenix store, being sure to disclose the segment contribution margin, the segment controllable profit margin, and segment profit margin.

• The store sold 65,000 units at $18.00 each, after having purchased the units from various suppliers for $12.50. Phoenix salespeople are paid a 5% commission based on gross sales dollars.

• Phoenix's sales manager oversees the placement of local advertising contracts, which totaled $54,000 for the year. Local property taxes amounted to $14,500.

• The sales manager's $65,000 salary is set by Phoenix's store manager. In contrast, the store manager's $134,000 salary is determined by Fog City's vice president.

• Phoenix incurred $6,800 of other noncontrollable costs.

• Nontraceable (common) corporate overhead totaled $68,000.

Fog City's corporate headquarters is located in Portland, and the company uses responsibility accounting to evaluate performance.

Required:

Prepare a segmented income statement for the Phoenix store, being sure to disclose the segment contribution margin, the segment controllable profit margin, and segment profit margin.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

72

The following selected data relate to the Idaho Division of Far West Enterprises (FWE):

Required:

A. Compute the following for the Idaho Division:

1. Segment contribution margin.

2. Controllable profit margin.

3. Segment profit margin.

B. Which of the three preceding measures should be used when evaluating the Idaho Division as an investment of FWE's resources? Why?

C. Assume that management made the decision to prepare a segmented income statement that reflected Idaho's five operating departments. Would all $1,120,000 of the controllable fixed costs be easily traced to the departments? Briefly explain.

D. Which of the five-dollar amounts presented in the body of the problem would be used in computing the income before taxes of Far West Enterprises?

Required:

A. Compute the following for the Idaho Division:

1. Segment contribution margin.

2. Controllable profit margin.

3. Segment profit margin.

B. Which of the three preceding measures should be used when evaluating the Idaho Division as an investment of FWE's resources? Why?

C. Assume that management made the decision to prepare a segmented income statement that reflected Idaho's five operating departments. Would all $1,120,000 of the controllable fixed costs be easily traced to the departments? Briefly explain.

D. Which of the five-dollar amounts presented in the body of the problem would be used in computing the income before taxes of Far West Enterprises?

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 72 flashcards in this deck.