Deck 5: Client Acceptance and Continuance and Preliminary Engagement Procedures

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

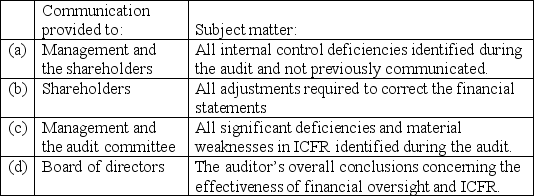

An audit engagement letter sets forth the auditor's responsibility for confirming its responsibility to provide written communications to the client company for each of the following items except:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 5: Client Acceptance and Continuance and Preliminary Engagement Procedures

1

An audit firm's business risk is affected by:

A) the client's business risk.

B) its ability to make profits from the work it performs.

C) the integrity of client's management.

D) All of the above.

A) the client's business risk.

B) its ability to make profits from the work it performs.

C) the integrity of client's management.

D) All of the above.

D

2

A company's recent restatement of previously issued financial statements is a favorable indicator that the company's internal controls are effective in the timely detection of errors and misstatements.

False

3

A management representation letter is an important item of audit evidence that auditors must obtain at the beginning of the engagement to establish an understanding of the terms of the engagement.

False

4

If a company's audit committee is not actively involved in the financial reporting function, this is viewed by auditors as a weakness in internal control.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

An incoming auditor should protect its independence by avoiding communications with the predecessor auditor.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

The risk of client misconduct is concerned with management's reputation and integrity.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

A request for proposal (RFP) is required for each client acceptance or continuance decision.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

Information about changes in a company's ownership, management, and/or audit firm is provided within Form 8K.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

Facts that warn an auditor that fraud may be occurring can also inform the auditor's judgments on client acceptance and continuance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

Companies often change audit firms prior to an initial public offering (IPO).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is used by auditors as a source of guidance on client acceptance and continuance decisions?

A) COSO Enterprise Risk Management and Internal Control frameworks.

B) Auditing standards on risk, fraud, and ICFR.

C) The audit firm's quality control standards.

D) All of the above.

A) COSO Enterprise Risk Management and Internal Control frameworks.

B) Auditing standards on risk, fraud, and ICFR.

C) The audit firm's quality control standards.

D) All of the above.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

In an audit engagement letter, a clause addressing document retention states that the auditors will retain the client company's accounting records until the audit fees have been collected.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is not a reason why auditors perform an investigation of potential clients as part of their client acceptance and continuance procedures?

A) It is important for auditors to establish good reputations, so they strive to accept clients that possess a high level of integrity.

B) They want to avoid business risks associated with potential litigation.

C) They want to be reasonably assured of their ability to earn a profit from the audit engagements they perform.

D) They want to assist their audit clients in recovering from financial decline.

A) It is important for auditors to establish good reputations, so they strive to accept clients that possess a high level of integrity.

B) They want to avoid business risks associated with potential litigation.

C) They want to be reasonably assured of their ability to earn a profit from the audit engagements they perform.

D) They want to assist their audit clients in recovering from financial decline.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

An auditor's quality control (QC) standards provide important benchmarks against which an auditor can assess the quality of a potential client.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

An audit firm should immediately decline to propose on a public company's audit if the company's CFO was recently a partner in the audit firm.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

An auditor's professional competence is directly related to the audit fees it is able to negotiate as part of the client acceptance or continuance activities.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

The Sarbanes-Oxley Act requires that all public companies have an audit committee comprised of at least three independent financial experts and at least one other person.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

Audit firms should always avoid a potential client company that conducts significant related party transactions in the ordinary course of business.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following best describes the role of an audit firm's quality control standards to provide guidance addressing client acceptance and continuance?

A) A standard framework should provide important benchmarks to be used by client companies to evaluate their own risk factors.

B) Representative legal cases should be documented whenever client company characteristics resemble fact patterns.

C) Policies and procedures should be in place for determining whether to accept or continue to perform an audit engagement.

D) A well-structured timeline and written communication plan should be in place for all proposal and decision processes.

A) A standard framework should provide important benchmarks to be used by client companies to evaluate their own risk factors.

B) Representative legal cases should be documented whenever client company characteristics resemble fact patterns.

C) Policies and procedures should be in place for determining whether to accept or continue to perform an audit engagement.

D) A well-structured timeline and written communication plan should be in place for all proposal and decision processes.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

An auditor's professional competence depends upon each of the following except:

A) knowledge.

B) a reputation for issuing unqualified audit opinions.

C) the availability of professional staff and other resources necessary for the audit engagement.

D) the requisite training and proficiency necessary for the audit engagement.

A) knowledge.

B) a reputation for issuing unqualified audit opinions.

C) the availability of professional staff and other resources necessary for the audit engagement.

D) the requisite training and proficiency necessary for the audit engagement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

When a potential client has announced its intention to "go public," the auditor's client acceptance decision is likely to depend upon:

A) the results of background checks performed on individuals in key financial management positions.

B) whether a formal RFP was used.

C) whether the predecessor auditor was appropriately independent.

D) characteristics of the shareholders who will purchase the public shares.

A) the results of background checks performed on individuals in key financial management positions.

B) whether a formal RFP was used.

C) whether the predecessor auditor was appropriately independent.

D) characteristics of the shareholders who will purchase the public shares.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

In which publicly-filed document is an auditor most likely to find information about a potential client's financial trends?

A) Form 8K.

B) Management discussion and analysis section of the Form 10K.

C) Proxy statements.

D) Engagement letter.

A) Form 8K.

B) Management discussion and analysis section of the Form 10K.

C) Proxy statements.

D) Engagement letter.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is least likely to warrant further investigation of a potential client company?

A) Several companies in the same industry are experiencing business failures.

B) None of the audit committee members is a financial expert.

C) The audit committee concurs with management's selection of accounting treatments.

D) One of the directors was convicted of tax evasion.

A) Several companies in the same industry are experiencing business failures.

B) None of the audit committee members is a financial expert.

C) The audit committee concurs with management's selection of accounting treatments.

D) One of the directors was convicted of tax evasion.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following are least problematic for an auditor about going concern issues of a potential audit client?

A) Recent cash flow trends raise questions about the company's ability to pay its audit fees and other financial obligations.

B) Recent financial instability heightens the company's risk for being sued.

C) Escalating financial pressures heighten the company's risk of experiencing management fraud.

D) Changing economic conditions create additional demand for the company's products.

A) Recent cash flow trends raise questions about the company's ability to pay its audit fees and other financial obligations.

B) Recent financial instability heightens the company's risk for being sued.

C) Escalating financial pressures heighten the company's risk of experiencing management fraud.

D) Changing economic conditions create additional demand for the company's products.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

A RFP is an important source of information that is:

A) provided by a potential client about its proposal process and audit engagement.

B) provided by an auditor about how its professional competencies match the needs of the audit engagement.

C) used only for audits of public companies.

D) used only when a company needs to change auditors.

A) provided by a potential client about its proposal process and audit engagement.

B) provided by an auditor about how its professional competencies match the needs of the audit engagement.

C) used only for audits of public companies.

D) used only when a company needs to change auditors.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

By speaking with individuals inside the company, an auditor may learn about:

A) Management's philosophy and integrity.

B) The composition of the Board of Directors and audit committee.

C) The organizational structure and accounting functions.

D) All of the above.

A) Management's philosophy and integrity.

B) The composition of the Board of Directors and audit committee.

C) The organizational structure and accounting functions.

D) All of the above.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following would be least likely to preclude an audit firm from proposing on a potential client due to independence concerns?

A) A recently-promoted partner in the audit firm holds a financial interest in the potential client company.

B) Someone who resigned from the audit firm three years ago is now the Chief Accounting Officer at the potential client company.

C) The audit firm provides internal audit outsourcing and certain nonaudit services to the client company.

D) The audit firm's pension plan holds securities of the potential client company.

A) A recently-promoted partner in the audit firm holds a financial interest in the potential client company.

B) Someone who resigned from the audit firm three years ago is now the Chief Accounting Officer at the potential client company.

C) The audit firm provides internal audit outsourcing and certain nonaudit services to the client company.

D) The audit firm's pension plan holds securities of the potential client company.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

Financial statement restatements:

A) are a strong indicator of material weakness in ICFR when they are undertaken for the purpose of correcting an error in previously issued financial statements.

B) may not be considered significant when they are the result of more evidence becoming available after the financial statements have been released.

C) are required to be disclosed in the financial reports, as well as in the financial press.

D) All of the above.

A) are a strong indicator of material weakness in ICFR when they are undertaken for the purpose of correcting an error in previously issued financial statements.

B) may not be considered significant when they are the result of more evidence becoming available after the financial statements have been released.

C) are required to be disclosed in the financial reports, as well as in the financial press.

D) All of the above.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

An engagement letter for an audit:

A) provides recommendations to management about improvements in its system of ICFR.

B) distinguishes management's responsibilities throughout the audit process from the auditor's.

C) specifies the high risk areas that will be the focus of the audit engagement.

D) specifies the type of audit opinion that will be issued.

A) provides recommendations to management about improvements in its system of ICFR.

B) distinguishes management's responsibilities throughout the audit process from the auditor's.

C) specifies the high risk areas that will be the focus of the audit engagement.

D) specifies the type of audit opinion that will be issued.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

By communicating with the predecessor auditor, an incoming auditor may gain valuable information pertaining to:

A) potential problem areas as indicated in the predecessor's work papers.

B) the updated status of a pending lawsuit.

C) the results of the current year budget variance analysis.

D) the audit tests that must be performed on a recurring basis.

A) potential problem areas as indicated in the predecessor's work papers.

B) the updated status of a pending lawsuit.

C) the results of the current year budget variance analysis.

D) the audit tests that must be performed on a recurring basis.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

Independence issues that would preclude an audit firm from proposing on a potential audit client:

A) are only applicable on public company audit engagements.

B) are not affected by the Sarbanes-Oxley Act.

C) cannot be determined until the audit planning process is complete.

D) may result from current business relationships of the audit firm's former employees.

A) are only applicable on public company audit engagements.

B) are not affected by the Sarbanes-Oxley Act.

C) cannot be determined until the audit planning process is complete.

D) may result from current business relationships of the audit firm's former employees.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

Where can auditors obtain information about a potential client company?

A) The company's Web site.

B) Reports filed with the SEC.

C) The shareholders.

D) Both a and

B)

A) The company's Web site.

B) Reports filed with the SEC.

C) The shareholders.

D) Both a and

B)

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

Related party transactions are:

A) quite rare, and are therefore a reason for auditors to avoid new client relationships due to the increased risk.

B) required to be disclosed in the financial statements.

C) assumed to be arms-length transactions unless they are disclosed in the financial statements.

D) considered to be a warning sign of going concern issues.

A) quite rare, and are therefore a reason for auditors to avoid new client relationships due to the increased risk.

B) required to be disclosed in the financial statements.

C) assumed to be arms-length transactions unless they are disclosed in the financial statements.

D) considered to be a warning sign of going concern issues.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

Earnings management pertains to:

A) accounting manipulations for the purpose of presenting the company in a biased manner.

B) conservative accounting treatments included in the financial disclosures.

C) the company's ability to limit production, if needed.

D) assigning responsibility for new accounting requirements.

A) accounting manipulations for the purpose of presenting the company in a biased manner.

B) conservative accounting treatments included in the financial disclosures.

C) the company's ability to limit production, if needed.

D) assigning responsibility for new accounting requirements.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

Communications between an incoming auditor and predecessor auditor:

A) require advanced approval from the client company.

B) are required to be documented in an engagement letter.

C) must be documented in a RFP if going concern issues exist.

D) are limited whenever the potential client is a public company.

A) require advanced approval from the client company.

B) are required to be documented in an engagement letter.

C) must be documented in a RFP if going concern issues exist.

D) are limited whenever the potential client is a public company.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

Whenever a company refuses to allow business professionals to communicate openly with an auditor, the auditor should be concerned about the likelihood that:

A) a RFP was not formalized.

B) information exists that the company wants to withhold.

C) management is centralized.

D) the company is experiencing rapid growth.

A) a RFP was not formalized.

B) information exists that the company wants to withhold.

C) management is centralized.

D) the company is experiencing rapid growth.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following factors pertaining to a client's accounting function is most significant in the client acceptance or continuance decision?

A) Effectiveness of internal controls.

B) Use of a commercial accounting software program.

C) Frequency of performance evaluations for accounting personnel.

D) Frequency of updating the general ledger.

A) Effectiveness of internal controls.

B) Use of a commercial accounting software program.

C) Frequency of performance evaluations for accounting personnel.

D) Frequency of updating the general ledger.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following is least likely to be used as a source of information about a potential new audit client?

A) The potential client company's predecessor auditor.

B) The potential client's management and directors.

C) Former employees and shareholders of the potential client company.

D) Published financial information of the potential client company.

A) The potential client company's predecessor auditor.

B) The potential client's management and directors.

C) Former employees and shareholders of the potential client company.

D) Published financial information of the potential client company.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is not a likely reason why an audit firm does not possess the necessary resources to perform an audit engagement?

A) The client company is very large and has multiple geographic locations.

B) The client company is in a highly regulated industry for which significant industry expertise is required.

C) The client company has a very complex IT system for which significant technical expertise is required.

D) The client company has a decentralized structure for providing management oversight.

A) The client company is very large and has multiple geographic locations.

B) The client company is in a highly regulated industry for which significant industry expertise is required.

C) The client company has a very complex IT system for which significant technical expertise is required.

D) The client company has a decentralized structure for providing management oversight.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following is least important to the auditor when investigating a potential new audit client?

A) The audit committee does not have the requisite number of independent members or financial experts.

B) The company has experienced recent operating losses and other financial difficulties.

C) The company has a highly decentralized organizational structure.

D) The company has experienced high turnover rates among management or members of the accounting, internal audit, or IT staff.

A) The audit committee does not have the requisite number of independent members or financial experts.

B) The company has experienced recent operating losses and other financial difficulties.

C) The company has a highly decentralized organizational structure.

D) The company has experienced high turnover rates among management or members of the accounting, internal audit, or IT staff.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Items documented in an engagement letter about which the auditor and client establish an understanding include:

A) management's responsibility for ensuring that the company complies with applicable laws and regulations.

B) management's responsibility for providing reasonable assurance about whether the financial statements are free of material misstatement.

C) the auditor's responsibility for maintaining effective ICFR throughout the audit engagement.

D) the auditor's responsibility for signing a management representation letter at the conclusion of the audit engagement.

A) management's responsibility for ensuring that the company complies with applicable laws and regulations.

B) management's responsibility for providing reasonable assurance about whether the financial statements are free of material misstatement.

C) the auditor's responsibility for maintaining effective ICFR throughout the audit engagement.

D) the auditor's responsibility for signing a management representation letter at the conclusion of the audit engagement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

The first section of an engagement letter addresses the terms of the services and related report, including the auditor's performance of a(n):

A) integrated audit of the financial statements and ICFR.

B) integrated audit of the financial statements and income tax returns.

C) integrated audit of the information contained in each Form 10-Q filed during the year.

D) review of the company's monthly financial information to be filed with the SEC

A) integrated audit of the financial statements and ICFR.

B) integrated audit of the financial statements and income tax returns.

C) integrated audit of the information contained in each Form 10-Q filed during the year.

D) review of the company's monthly financial information to be filed with the SEC

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following matters would not be included in the terms of an engagement letter?

A) Audit fees and billing arrangements.

B) Involvement of internal auditors and/or a predecessor auditor.

C) Additional services to be provided in connection with the engagement.

D) Conditions under which the auditor's independence requirement may be waived.

A) Audit fees and billing arrangements.

B) Involvement of internal auditors and/or a predecessor auditor.

C) Additional services to be provided in connection with the engagement.

D) Conditions under which the auditor's independence requirement may be waived.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

Auditors of public companies are required by SOX to communicate certain matters to the client company's audit committee, including:

A) significant audit findings and adjustments made to the financial statements.

B) identification of the auditor who will sign the SOX 302 certification.

C) identification of the auditor who will sign the management representation letter.

D) an explanation about whether the auditor chose to follow PCAOB or AICPA standards during the engagement.

A) significant audit findings and adjustments made to the financial statements.

B) identification of the auditor who will sign the SOX 302 certification.

C) identification of the auditor who will sign the management representation letter.

D) an explanation about whether the auditor chose to follow PCAOB or AICPA standards during the engagement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following items is not important with regard to an auditor's responsibilities for communicating with the audit committee?

A) Disagreements with management.

B) Difficulties encountered in the performance of audit testing.

C) Significant deficiencies and material weaknesses in ICFR.

D) New staff members included on the audit team.

A) Disagreements with management.

B) Difficulties encountered in the performance of audit testing.

C) Significant deficiencies and material weaknesses in ICFR.

D) New staff members included on the audit team.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

The absence of sufficiently documented evidence to support management's assessment of the operating effectiveness of ICFR is a(n):

A) material weakness that would require the auditor to withdraw from the audit engagement.

B) internal control deficiency that could preclude the issuance of an unqualified audit report.

C) matter of concern only to the company's audit committee, predecessor auditors, and internal auditors.

D) example of the effective operation of the company's document retention policy.

A) material weakness that would require the auditor to withdraw from the audit engagement.

B) internal control deficiency that could preclude the issuance of an unqualified audit report.

C) matter of concern only to the company's audit committee, predecessor auditors, and internal auditors.

D) example of the effective operation of the company's document retention policy.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

The engagement letter includes provisions for the electronic filing of the client company's financial reports with the SEC. These provisions include consents which will authorize the:

A) use of the audit firm's logo on each page of the filing.

B) use of the audit firm's name in the electronic submission.

C) retention of audit evidence for a period of 10 years following the audit engagement.

D) dissemination of the audit report to the auditor's other clients.

A) use of the audit firm's logo on each page of the filing.

B) use of the audit firm's name in the electronic submission.

C) retention of audit evidence for a period of 10 years following the audit engagement.

D) dissemination of the audit report to the auditor's other clients.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following is not a responsibility of an audit committee?

A) Hiring, compensating, and overseeing the company's independent auditor relationship.

B) Receiving and addressing complaints about accounting, internal control, and auditing matters.

C) Resolving disagreements between management and the auditor regarding financial reporting.

D) Preparing the disclosures that accompany the financial statements in the company's annual report.

A) Hiring, compensating, and overseeing the company's independent auditor relationship.

B) Receiving and addressing complaints about accounting, internal control, and auditing matters.

C) Resolving disagreements between management and the auditor regarding financial reporting.

D) Preparing the disclosures that accompany the financial statements in the company's annual report.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

An audit engagement letter:

A) is prepared by the client company and signed by a representative of the audit firm.

B) provides a guarantee that the auditor will express an opinion as a result of the audit.

C) is signed by management at the conclusion of the audit engagement.

D) specifies that management is responsible for establishing and maintaining effective ICFR.

A) is prepared by the client company and signed by a representative of the audit firm.

B) provides a guarantee that the auditor will express an opinion as a result of the audit.

C) is signed by management at the conclusion of the audit engagement.

D) specifies that management is responsible for establishing and maintaining effective ICFR.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

An engagement letter states that a company should maintain documentation sufficient to support its assessment of ICFR for a period of:

A) ten years from the date of the audit report.

B) seven years from the date of the audit report.

C) five years from the date of the financial statements.

D) three years from the date of the financial statements.

A) ten years from the date of the audit report.

B) seven years from the date of the audit report.

C) five years from the date of the financial statements.

D) three years from the date of the financial statements.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

Which of the following is not an attribute of a financial expert?

A) An understanding of internal controls and procedures for financial reporting.

B) An affiliation with the company or its subsidiaries.

C) Education and experience as a financial officer, accountant, or auditor.

D) An understanding of GAAP.

A) An understanding of internal controls and procedures for financial reporting.

B) An affiliation with the company or its subsidiaries.

C) Education and experience as a financial officer, accountant, or auditor.

D) An understanding of GAAP.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

The limitations of an audit which are documented in an engagement letter pertain to each of the following except:

A) material errors or illegal activities having a direct and material financial statement impact may not be detected because of the judgmental nature of many audit areas and the fact that detailed tests are not performed for all types of transactions.

B) fraudulent activities having a direct and material financial statement impact may not be detected because of the nature of fraud, including the possibility of the perpetrator's concealment efforts and/or management's override of controls.

C) internal controls may change or deteriorate such that they may not be effective in the prevention or detection of future material misstatements in the financial statements.

D) under the standards established by the PCAOB, the auditor's responsibilities for communicating internal control weaknesses are limited to notification to the company's shareholders regarding material weaknesses.

A) material errors or illegal activities having a direct and material financial statement impact may not be detected because of the judgmental nature of many audit areas and the fact that detailed tests are not performed for all types of transactions.

B) fraudulent activities having a direct and material financial statement impact may not be detected because of the nature of fraud, including the possibility of the perpetrator's concealment efforts and/or management's override of controls.

C) internal controls may change or deteriorate such that they may not be effective in the prevention or detection of future material misstatements in the financial statements.

D) under the standards established by the PCAOB, the auditor's responsibilities for communicating internal control weaknesses are limited to notification to the company's shareholders regarding material weaknesses.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

The engagement letter states that auditors are responsible for informing the client's audit committee about certain matters related to the conduct of the audit, including any:

A) serious difficulties encountered in performing the audit.

B) disagreements among audit team members pertaining to conclusions reached during the audit.

C) revisions made in the nature of audit tests performed as a result of information discovered during the course of the audit.

D) changes in the company's operational procedures during the year.

A) serious difficulties encountered in performing the audit.

B) disagreements among audit team members pertaining to conclusions reached during the audit.

C) revisions made in the nature of audit tests performed as a result of information discovered during the course of the audit.

D) changes in the company's operational procedures during the year.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

An audit engagement letter sets forth the auditor's responsibility for confirming its responsibility to provide written communications to the client company for each of the following items except:

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

A management representation letter is prepared for the purpose of:

A) confirming management's acceptance of the audit fees.

B) setting forth the terms of the audit engagement.

C) confirming the honesty and validity of audit information provided by management.

D) establishing management's responsibility for making the company's financial records available to the auditor.

A) confirming management's acceptance of the audit fees.

B) setting forth the terms of the audit engagement.

C) confirming the honesty and validity of audit information provided by management.

D) establishing management's responsibility for making the company's financial records available to the auditor.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

An audit engagement letter specifies that management of the client company is responsible for all of the following except:

A) preparing the financial statements.

B) maintaining effective ICFR.

C) providing the company's financial records for the auditor.

D) performing the audit in accordance with PCAOB standards.

A) preparing the financial statements.

B) maintaining effective ICFR.

C) providing the company's financial records for the auditor.

D) performing the audit in accordance with PCAOB standards.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

The Blue Ribbon Committee on Improving the Effectiveness of Corporate Audit Committees is known for making recommendations to audit committees concerning:

A) composition of the committee, communication requirements, and oversight responsibilities.

B) qualifications of the committee, timing of their terms, and specific corrections in ICFR systems.

C) SEC filing deadlines, stock exchange requirements, and qualifications of membership.

D) liquidity of the capital markets, types of SEC affiliations and reporting forms, and compensation requirements.

A) composition of the committee, communication requirements, and oversight responsibilities.

B) qualifications of the committee, timing of their terms, and specific corrections in ICFR systems.

C) SEC filing deadlines, stock exchange requirements, and qualifications of membership.

D) liquidity of the capital markets, types of SEC affiliations and reporting forms, and compensation requirements.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following items is not one of management's responsibilities for communicating with the auditors?

A) Suspected fraudulent activities within the company.

B) Deficiencies in the design or operating effectiveness of ICFR.

C) Key accounts and transactions to be selected for testing.

D) Violations of regulations applicable to the company's activities.

A) Suspected fraudulent activities within the company.

B) Deficiencies in the design or operating effectiveness of ICFR.

C) Key accounts and transactions to be selected for testing.

D) Violations of regulations applicable to the company's activities.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

59

The New York Stock Exchange requirements regarding composition of the audit committee include each of the following except:

A) the audit committee must have at least three members who are financially sophisticated, and one of those members must be independent.

B) the audit committee must have at least three members who are independent, and one of those members must be financially sophisticated.

C) each member of the audit committee must not have participated in the preparation of the financial statements of the issuer at any time during the past three years.

D) each member of the audit committee must have the ability to read and understand fundamental financial statements.

A) the audit committee must have at least three members who are financially sophisticated, and one of those members must be independent.

B) the audit committee must have at least three members who are independent, and one of those members must be financially sophisticated.

C) each member of the audit committee must not have participated in the preparation of the financial statements of the issuer at any time during the past three years.

D) each member of the audit committee must have the ability to read and understand fundamental financial statements.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

The engagement letter states that an auditor's opinion on the financial statements and effectiveness of the company's ICFR will depend upon the following type of evidential matter:

A) results of audit testing.

B) responses to auditor inquiry.

C) management representation letter.

D) All of the above.

A) results of audit testing.

B) responses to auditor inquiry.

C) management representation letter.

D) All of the above.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

With respect to an integrated audit, describe the respective responsibilities of management and the auditor. Provide at least five responsibilities for each party that would be documented in an engagement letter.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

What are the characteristics of fraud, and how does the suspicion of fraud in a company affect an auditor's client acceptance or continuance decision?

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

When is an auditor considered a "rainmaker," and how is this label applicable to the client acceptance decision?

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

Kellen Electronics, Inc. (KEI), a public company, has been experiencing negative cash flows from operations and deteriorating profit margins. Recent press releases have been quite pessimistic, and the company's stock price is in a downward trend. How would an auditor interpret this negative information with regard to a potential audit client? How would your answer be different if this was a continuing client?

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

Match between columns

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.