Deck 17: Advanced Issues in Revenue Recognition

Full screen (f)

Question

Question

Question

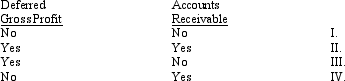

Net assets increase from cost to selling price when revenue is recognized

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

If revenue is not recognized at the time of sale, which of the following accounts may be affected at the time of sale?

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Question

Question

Question

Question

Question

Question

Question

Question

Question

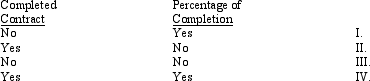

Anticipated losses are recognized immediately under which of the following methods of recognizing revenue?

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Question

Question

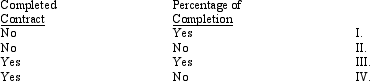

Which of the following revenue recognition methods can be used by long-term construction companies in most circumstances?

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Question

Question

Question

Question

Question

Question

Question

Question

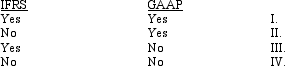

Specific industry guidance regarding revenue recognition is prevalent in

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Question

Under the percentage of completion method of revenue recognition, Partial Billings could be reported on the balance sheet as a

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Question

Question

Question

Exhibit 17-1 In 2014, Omega Construction began work on a contract with a price of $850,000 and estimated costs of $595,000. Data for each year of the contract are as follows:

- Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, gross profit in 2014 would be

A) $102,000

B) $260,000

C) $255,000

D) $425,000

- Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, gross profit in 2014 would be

A) $102,000

B) $260,000

C) $255,000

D) $425,000

Question

Question

Question

Question

Question

Question

Question

Question

Exhibit 17-2 The following information relates to a project of the Cumberland Construction Company:

The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2014?

A) $150,000

B) $ 28,571

C) $ 24,000

D) $ 20,400

The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2014?

A) $150,000

B) $ 28,571

C) $ 24,000

D) $ 20,400

Question

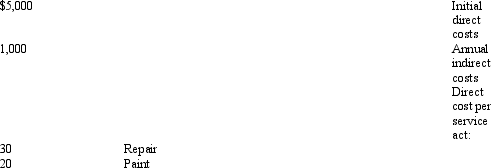

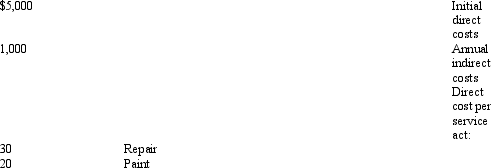

Exhibit 17-3 On January 1, 2014, Dundee Co. sold 100 contracts at $500 each. Each contract permitted the buyer to use a repair bay six times and a paint bay nine times.

Additional information: In 2014, the repair bay was used 180 times and the paint bay was used 162 times.

In 2014, the repair bay was used 180 times and the paint bay was used 162 times.

Refer to Exhibit 17-3. What net income (loss) should be recognized by Dundee in 2014?

A) $2,590 loss

B) $1,160 income

C) $1,210 income

D) $2,640 loss

Additional information:

In 2014, the repair bay was used 180 times and the paint bay was used 162 times.Refer to Exhibit 17-3. What net income (loss) should be recognized by Dundee in 2014?

A) $2,590 loss

B) $1,160 income

C) $1,210 income

D) $2,640 loss

Question

Exhibit 17-1 In 2014, Omega Construction began work on a contract with a price of $850,000 and estimated costs of $595,000. Data for each year of the contract are as follows:

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the balance in Construction in Progress at the end of 2015 would be

A) $557,600

B) $659,600

C) $680,000

D) $782,000

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the balance in Construction in Progress at the end of 2015 would be

A) $557,600

B) $659,600

C) $680,000

D) $782,000

Question

Question

Exhibit 17-1 In 2014, Omega Construction began work on a contract with a price of $850,000 and estimated costs of $595,000. Data for each year of the contract are as follows:

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the net amount reported for construction in progress inventory at the end of 2015 would be

A) $ 87,600

B) $189,600

C) $210,000

D) $312,000

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the net amount reported for construction in progress inventory at the end of 2015 would be

A) $ 87,600

B) $189,600

C) $210,000

D) $312,000

Question

Question

Question

Question

Question

Exhibit 17-2 The following information relates to a project of the Cumberland Construction Company:

The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2016?

A) $ 29,375

B) $ 50,000

C) $117,500

D) $150,000

The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2016?

A) $ 29,375

B) $ 50,000

C) $117,500

D) $150,000

Question

Exhibit 17-3 On January 1, 2014, Dundee Co. sold 100 contracts at $500 each. Each contract permitted the buyer to use a repair bay six times and a paint bay nine times.

Additional information: In 2014, the repair bay was used 180 times and the paint bay was used 162 times.

In 2014, the repair bay was used 180 times and the paint bay was used 162 times.

Refer to Exhibit 17-3. How much revenue should be recognized by Dundee in 2014?

A) $12,000

B) $17,100

C) $25,000

D) $50,000

Additional information:

In 2014, the repair bay was used 180 times and the paint bay was used 162 times.Refer to Exhibit 17-3. How much revenue should be recognized by Dundee in 2014?

A) $12,000

B) $17,100

C) $25,000

D) $50,000

Question

Question

Question

Question

Question

Question

Question

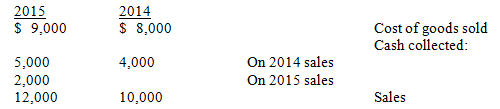

Exhibit 17-4 The following information is provided for Fort Myers Company:

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much gross profit did Fort Myers Company report in 2014?

A) $ 800

B) $2,000

C) $3,200

D) $4,000

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much gross profit did Fort Myers Company report in 2014?

A) $ 800

B) $2,000

C) $3,200

D) $4,000

Question

Question

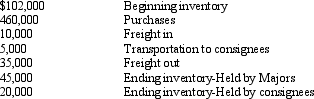

In 2014, Majors Company offered its goods to retailers on a consignment basis. The following information is provided regarding Majors Company's 2014 operations:

What is Majors' cost of goods sold for 2014?

A) $507,000

B) $512,000

C) $527,000

D) $547,000

What is Majors' cost of goods sold for 2014?

A) $507,000

B) $512,000

C) $527,000

D) $547,000

Question

Question

Exhibit 17-4 The following information is provided for Fort Myers Company:

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much deferred gross profit is still on the books at the end of 2015?

A) $ 0

B) $2,500

C) $2,700

D) $3,000

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much deferred gross profit is still on the books at the end of 2015?

A) $ 0

B) $2,500

C) $2,700

D) $3,000

Question

Question

Question

Question

Question

Question

Question

Question

Question

On January 1, 2014, Reids, Inc. sold a risky investment for $1,400 that had been purchased for $1,000. It was decided to use the cost recovery method of revenue recognition. Cash collections on accounts receivable related to the asset were as follows:  Which of the following represent the realized gross profit that Reids should recognize for each year?

Which of the following represent the realized gross profit that Reids should recognize for each year?

A) I

B) II

C) III

D) IV

Which of the following represent the realized gross profit that Reids should recognize for each year? A) I

B) II

C) III

D) IV

Question

Question

Question

Exhibit 17-4 The following information is provided for Fort Myers Company:

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much gross profit did Fort Myers Company report in 2015?

A) $1,300

B) $1,500

C) $1,700

D) $2,000

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much gross profit did Fort Myers Company report in 2015?

A) $1,300

B) $1,500

C) $1,700

D) $2,000

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/113

Play

Full screen (f)

Deck 17: Advanced Issues in Revenue Recognition

1

The installment and the cost recovery are methods that recognize revenue after the earnings process is complete and when realization occurs.

True

2

Which of the following situations would require the recognition of revenue to be deferred?

A) when the economic reality of a transaction represents a sale, even though title has not passed to the buyer

B) when the realizability of the receivable from a sale is not reasonably assured

C) when the risks of ownership have been transferred to the buyer

D) when the benefits of ownership have been transferred to the buyer

A) when the economic reality of a transaction represents a sale, even though title has not passed to the buyer

B) when the realizability of the receivable from a sale is not reasonably assured

C) when the risks of ownership have been transferred to the buyer

D) when the benefits of ownership have been transferred to the buyer

B

3

Net assets increase from cost to selling price when revenue is recognized

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

A

4

In selecting the appropriate method of recognizing revenue, which of the following qualitative characteristics of useful accounting information is paramount to the decision?

A) material

B) decision usefulness

C) relevance

D) reliability

A) material

B) decision usefulness

C) relevance

D) reliability

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

5

If a company has an agreement to deliver software that does not require significant production, modification, or customization of software then revenue is recognized based upon the percentage-of-completion method.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

6

Realization occurs when

A) revenues have been earned

B) noncash resources are converted to cash or rights to cash

C) an item is formally recorded in the books

D) an item is reported in a company's financial statements

A) revenues have been earned

B) noncash resources are converted to cash or rights to cash

C) an item is formally recorded in the books

D) an item is reported in a company's financial statements

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

7

SEC Staff Accounting Bulletin 106 summarizes the SEC's view of when recognition of revenue should occur.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

8

Theoretically, for revenue to be recognized the risks and benefits of ownership must have been transferred to the buyer. This refers to

A) expected cash flows being recognized

B) benefits being the expected net cash flows and the risks being the likelihood of another amount of cash being received

C) benefits being properly recorded revenue and the risks being the likelihood of expenses being greater than expected

D) expected revenue being realized

A) expected cash flows being recognized

B) benefits being the expected net cash flows and the risks being the likelihood of another amount of cash being received

C) benefits being properly recorded revenue and the risks being the likelihood of expenses being greater than expected

D) expected revenue being realized

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

9

Alternative methods of revenue recognition are used because these methods increase the

A) comparability of the financial statements

B) reliability of the financial statements

C) relevance of the financial statements

D) understandability of the financial statements

A) comparability of the financial statements

B) reliability of the financial statements

C) relevance of the financial statements

D) understandability of the financial statements

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

10

Revenue recognition is defined as the accomplishments of operating activities.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

11

When a long-term service contract requires similar services to be performed in more than one act, revenue is recognized by the percentage-of-performance method.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

12

The percentage-of-completion method and the proportional performance method are methods that recognize revenue at a point in the earnings process completed.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

13

If collectibility is reasonably certain or there is a reliable basis for estimating collectibility then the cost recovery method is appropriate.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

14

The importance the economic substance of an event taking precedence over the legal form refers to revenue being

A) earned and recognized

B) earned and realizable

C) earned and realized

D) realized and recognized

A) earned and recognized

B) earned and realizable

C) earned and realized

D) realized and recognized

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

15

Accrual method is usually associated with

A) revenue recognition in the period of sale

B) revenue recognition prior to the period of sale

C) revenue recognition after the period of sale

D) revenue recognition delayed until a future event occurs

A) revenue recognition in the period of sale

B) revenue recognition prior to the period of sale

C) revenue recognition after the period of sale

D) revenue recognition delayed until a future event occurs

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

16

If revenue is not recognized at the time of sale, which of the following accounts may be affected at the time of sale?

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

17

The period in which a company recognizes revenue is also the period in which it recognizes an increase in the

A) amount of net income

B) value of net assets

C) amount of owner's equity

D) amount of liabilities

A) amount of net income

B) value of net assets

C) amount of owner's equity

D) amount of liabilities

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

18

The operating-cycle concept is used to justify that the net amounts of Construction in Progress and Partial Billings be included as current assets or current liabilities.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

19

For retail land sales, revenue is recognized in full using the accrual method if it is earned and the receivable is realized or realizable.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

20

It is important to understand the difference between an installment sale and the installment method of revenue recognition, which a company recognizes revenue in full at the time of the sale if collectibility is reasonably assured.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

21

IFRS and GAAP will sometimes differ in the method of revenue recognition applied to construction contracts. Three different methods are involved: percentage of completion, cost recovery, and completed contract. The fastest to slowest revenue recognition among the methods is

A) percentage of completion; completed contract; cost recovery

B) completed contract; percentage of completion; cost recovery

C) percentage of completion; cost recovery; completed contract

D) cost recovery; percentage of completion; completed contract

A) percentage of completion; completed contract; cost recovery

B) completed contract; percentage of completion; cost recovery

C) percentage of completion; cost recovery; completed contract

D) cost recovery; percentage of completion; completed contract

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

22

When revenue is recognized in the period of the sale, generally

A) realization has occurred and revenue is earned.

B) recognition has occurred and revenue is earned.

C) recognition has occurred and cash has been received.

D) realization has occurred and cash has been received.

A) realization has occurred and revenue is earned.

B) recognition has occurred and revenue is earned.

C) recognition has occurred and cash has been received.

D) realization has occurred and cash has been received.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

23

When a sufficient transfer of the risks and benefits of ownership does not exist in a sales transaction, the preferred revenue recognition method is the

A) proportional performance method

B) installment method

C) percentage of completion

D) deferral method

A) proportional performance method

B) installment method

C) percentage of completion

D) deferral method

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

24

When a company uses the percentage-of-completion method for revenue recognition, the most difficult approach to determine the percentage completed is using

A) output measures

B) cost-to-cost method

C) efforts-expended method

D) input measures

A) output measures

B) cost-to-cost method

C) efforts-expended method

D) input measures

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

25

Anticipated losses are recognized immediately under which of the following methods of recognizing revenue?

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

26

Which method of revenue recognition do IFRS require for construction contracts when the percentage-of-completion method cannot be applied?

A) completed contract

B) installment sales

C) completed contract

D) cost recovery

A) completed contract

B) installment sales

C) completed contract

D) cost recovery

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following revenue recognition methods can be used by long-term construction companies in most circumstances?

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

28

When Partial Billings exceeds Construction in Progress, under the completed-contract method the two accounts are reported together on the balance sheet in the

A) current assets section

B) long-term assets section

C) current liabilities section

D) long-term liabilities section

A) current assets section

B) long-term assets section

C) current liabilities section

D) long-term liabilities section

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

29

Under the completed-contract method of revenue recognition, the partial billings account is closed out against the

A) construction in progress account

B) construction revenue account

C) income summary account

D) construction expense account

A) construction in progress account

B) construction revenue account

C) income summary account

D) construction expense account

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

30

Inventory is reported at cost plus gross profit recognized to date under which of the following revenue recognition methods?

A) completed contract method

B) installment method

C) cost recovery method

D) percentage of completion method

A) completed contract method

B) installment method

C) cost recovery method

D) percentage of completion method

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

31

When a down payment is received, the deposit from purchaser account used under the deferral method is reported on the balance sheet of the seller as a(n)

A) revenue

B) liability

C) asset

D) contra asset

A) revenue

B) liability

C) asset

D) contra asset

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

32

The deferral method is usually associated with

A) revenue recognition in the period of sale

B) revenue recognition prior to the period of sale

C) revenue recognition after the period of sale

D) revenue recognition delayed until a future event occurs

A) revenue recognition in the period of sale

B) revenue recognition prior to the period of sale

C) revenue recognition after the period of sale

D) revenue recognition delayed until a future event occurs

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

33

For long-term construction contracts, when there is not assurance that the buyer can be expected to satisfy its obligations under a contract, which of the following revenue recognition methods is preferable?

A) percentage-of-completion method

B) installment method

C) deferral method

D) completed-contract method

A) percentage-of-completion method

B) installment method

C) deferral method

D) completed-contract method

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

34

The installment method is usually associated with

A) revenue recognition in the period of sale

B) revenue recognition prior to the period of sale

C) revenue recognition after the period of sale

D) revenue recognition delayed until a future event occurs

A) revenue recognition in the period of sale

B) revenue recognition prior to the period of sale

C) revenue recognition after the period of sale

D) revenue recognition delayed until a future event occurs

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

35

Specific industry guidance regarding revenue recognition is prevalent in

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

36

Under the percentage of completion method of revenue recognition, Partial Billings could be reported on the balance sheet as a

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

37

A Provision for Loss on Contract is reported in the financial statements as a(n)

A) contra-asset account

B) asset account

C) liability account

D) contra-liability account

A) contra-asset account

B) asset account

C) liability account

D) contra-liability account

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

38

The proportional performance method is usually associated with

A) revenue recognition in the period of sale

B) revenue recognition prior to the period of sale

C) revenue recognition after the period of sale

D) revenue recognition delayed until a future event occurs

A) revenue recognition in the period of sale

B) revenue recognition prior to the period of sale

C) revenue recognition after the period of sale

D) revenue recognition delayed until a future event occurs

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

39

Exhibit 17-1 In 2014, Omega Construction began work on a contract with a price of $850,000 and estimated costs of $595,000. Data for each year of the contract are as follows:

- Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, gross profit in 2014 would be

A) $102,000

B) $260,000

C) $255,000

D) $425,000

- Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, gross profit in 2014 would be

A) $102,000

B) $260,000

C) $255,000

D) $425,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

40

Revenue recognition prior to period of sale is used to reflect

A) reliability of the financial information

B) economic substance instead of legal form

C) the inability of a producer to determine acquisition cost

D) the recognition of propositional performance

A) reliability of the financial information

B) economic substance instead of legal form

C) the inability of a producer to determine acquisition cost

D) the recognition of propositional performance

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

41

The Marathon Company uses the percentage-of-completion method to recognize profits on long-term contracts. At the end of the second year of the contract, a project was 70% complete and an overall loss of $100,000 was expected. A $25,000 profit had been recognized in the first year of the contract. The loss to be recognized in the second year is

A) $ 75,000

B) $ 85,000

C) $105,000

D) $125,000

A) $ 75,000

B) $ 85,000

C) $105,000

D) $125,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

42

Which one of the following entries would you probably not see if an entity used the percentage-of-completion method?

A) Partial Billings XX

Construction Revenue XX

B) Construction Expense XX

Construction in Progress XX

Construction Revenue XX

C) Accounts Receivable XX

Partial Billings XX

D) Partial Billings XX

Construction in Progress XX

A) Partial Billings XX

Construction Revenue XX

B) Construction Expense XX

Construction in Progress XX

Construction Revenue XX

C) Accounts Receivable XX

Partial Billings XX

D) Partial Billings XX

Construction in Progress XX

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

43

A company may recognize revenue in full at the time of a sale if

A) the probability of collection is not reasonably assured

B) there is a very high degree of uncertainty about the collectibility of the sales price

C) the collection of the sales price is improbable

D) the collectibility of the sales price is not an issue

A) the probability of collection is not reasonably assured

B) there is a very high degree of uncertainty about the collectibility of the sales price

C) the collection of the sales price is improbable

D) the collectibility of the sales price is not an issue

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

44

When a long-term service contract requires services to be performed in more than one act, revenue is recognized by the

A) percentage-of-completion method

B) proportional performance method

C) completed contract method

D) All of these choices

A) percentage-of-completion method

B) proportional performance method

C) completed contract method

D) All of these choices

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

45

The percentage-of-completion method of revenue recognition is more

A) reliable

B) accurate

C) relevant

D) verifiable

A) reliable

B) accurate

C) relevant

D) verifiable

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

46

An excess of Construction in Progress over Partial Billings for long-term contracts accounted for on the percentage-of-completion method should be shown as a

A) current asset

B) current liability

C) long-term asset

D) long-term liability

A) current asset

B) current liability

C) long-term asset

D) long-term liability

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

47

Exhibit 17-2 The following information relates to a project of the Cumberland Construction Company:

The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2014?

A) $150,000

B) $ 28,571

C) $ 24,000

D) $ 20,400

The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2014?

A) $150,000

B) $ 28,571

C) $ 24,000

D) $ 20,400

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

48

Exhibit 17-3 On January 1, 2014, Dundee Co. sold 100 contracts at $500 each. Each contract permitted the buyer to use a repair bay six times and a paint bay nine times.

Additional information: In 2014, the repair bay was used 180 times and the paint bay was used 162 times.

Refer to Exhibit 17-3. What net income (loss) should be recognized by Dundee in 2014?

A) $2,590 loss

B) $1,160 income

C) $1,210 income

D) $2,640 loss

Additional information:

In 2014, the repair bay was used 180 times and the paint bay was used 162 times.Refer to Exhibit 17-3. What net income (loss) should be recognized by Dundee in 2014?

A) $2,590 loss

B) $1,160 income

C) $1,210 income

D) $2,640 loss

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

49

Exhibit 17-1 In 2014, Omega Construction began work on a contract with a price of $850,000 and estimated costs of $595,000. Data for each year of the contract are as follows:

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the balance in Construction in Progress at the end of 2015 would be

A) $557,600

B) $659,600

C) $680,000

D) $782,000

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the balance in Construction in Progress at the end of 2015 would be

A) $557,600

B) $659,600

C) $680,000

D) $782,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

50

The deferred gross profit on installment sales is reported on the balance sheet as a

A) current asset

B) current liability

C) contra-asset

D) long-term liability

A) current asset

B) current liability

C) contra-asset

D) long-term liability

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

51

Exhibit 17-1 In 2014, Omega Construction began work on a contract with a price of $850,000 and estimated costs of $595,000. Data for each year of the contract are as follows:

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the net amount reported for construction in progress inventory at the end of 2015 would be

A) $ 87,600

B) $189,600

C) $210,000

D) $312,000

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the net amount reported for construction in progress inventory at the end of 2015 would be

A) $ 87,600

B) $189,600

C) $210,000

D) $312,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

52

The Marco Company uses the percentage-of-completion method and the cost-to-cost method for its long-term construction contracts. On one such contract, Marco expects total revenues of $260,000 and total costs of $200,000. During the first year, Marco incurred costs of $50,000 and billed the customer $30,000 under the contract. At what net amount should Marco's Construction in Progress for this contract be reported at the end of the first year?

A) $30,000

B) $35,000

C) $50,000

D) $65,000

A) $30,000

B) $35,000

C) $50,000

D) $65,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

53

GAAP requires the completed-contract method to be used when the

A) company expects to perform its contractual obligations

B) buyer can be expected to satisfy its obligations under the contract

C) company can make reasonably dependable estimates of the extent of progress toward project completion

D) contract does not clearly specify the manner and terms of settlement

A) company expects to perform its contractual obligations

B) buyer can be expected to satisfy its obligations under the contract

C) company can make reasonably dependable estimates of the extent of progress toward project completion

D) contract does not clearly specify the manner and terms of settlement

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

54

In early 2014, the Key West Company signed a contract for construction of an industrial park to be completed in three years. At that time, estimated total costs were $2,250,000, and estimated total revenues were $4,000,000. During 2014, Key West incurred costs of $960,000 and collected $1,100,000. In December 2014, Key West recalculated total costs for the project to be $3,200,000 while estimated total revenues remained unchanged. What amount of profit (loss) should be recognized by Key West for 2014, using the percentage-of-completion method?

A) $266,667 profit

B) $ 55,000 loss

C) $240,000 profit

D) $285,000 loss

A) $266,667 profit

B) $ 55,000 loss

C) $240,000 profit

D) $285,000 loss

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

55

Which one of the following types of service costs are deferred and expensed only when the related service revenue is recognized?

A) initial indirect costs

B) direct costs

C) indirect costs

D) initial direct costs

A) initial indirect costs

B) direct costs

C) indirect costs

D) initial direct costs

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

56

Exhibit 17-2 The following information relates to a project of the Cumberland Construction Company:

The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2016?

A) $ 29,375

B) $ 50,000

C) $117,500

D) $150,000

The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2016?

A) $ 29,375

B) $ 50,000

C) $117,500

D) $150,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

57

Exhibit 17-3 On January 1, 2014, Dundee Co. sold 100 contracts at $500 each. Each contract permitted the buyer to use a repair bay six times and a paint bay nine times.

Additional information: In 2014, the repair bay was used 180 times and the paint bay was used 162 times.

Refer to Exhibit 17-3. How much revenue should be recognized by Dundee in 2014?

A) $12,000

B) $17,100

C) $25,000

D) $50,000

Additional information:

In 2014, the repair bay was used 180 times and the paint bay was used 162 times.Refer to Exhibit 17-3. How much revenue should be recognized by Dundee in 2014?

A) $12,000

B) $17,100

C) $25,000

D) $50,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

58

The percentage-of-completion method does not

A) recognize profit each period during the life of the contract in proportion to the portion of the contract completed during the period

B) value the inventory at cost less any partial billings

C) give precedence to economic substance over legal form

D) value the inventory at the costs incurred plus the profit recognized to date less any partial billings

A) recognize profit each period during the life of the contract in proportion to the portion of the contract completed during the period

B) value the inventory at cost less any partial billings

C) give precedence to economic substance over legal form

D) value the inventory at the costs incurred plus the profit recognized to date less any partial billings

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

59

When merchandise previously sold under an installment contract is repossessed, it is recorded at

A) cost

B) fair value

C) net realizable value

D) cost plus deferred gross profit

A) cost

B) fair value

C) net realizable value

D) cost plus deferred gross profit

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

60

Which one of the following types of cost is not a typical service cost involved with long-term service contracts?

A) initial direct costs

B) direct costs

C) initial indirect costs

D) indirect costs

A) initial direct costs

B) direct costs

C) initial indirect costs

D) indirect costs

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

61

If a company had an agreement to deliver software that requires significant production, modification, or customization, which method of revenue recognition should it use?

A) percentage-of-completion method

B) deferral method

C) installment method

D) cost recovery method

A) percentage-of-completion method

B) deferral method

C) installment method

D) cost recovery method

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

62

Which one of the following statements is false?

A) The use of the installment method of recognizing revenue is generally unacceptable.

B) When the installment method of recognizing revenue is in use, operating expenses are not deferred and recognized in the future.

C) Deferred gross profit should be disclosed as a current liability on the balance sheet.

D) A company may use the installment method of revenue recognition for a sales transaction that is not an installment sale.

A) The use of the installment method of recognizing revenue is generally unacceptable.

B) When the installment method of recognizing revenue is in use, operating expenses are not deferred and recognized in the future.

C) Deferred gross profit should be disclosed as a current liability on the balance sheet.

D) A company may use the installment method of revenue recognition for a sales transaction that is not an installment sale.

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

63

Forest Hill, Inc. repossessed an item it sold in 2014 with a gross profit of 40%. The fair value of the repossessed item was $140. The remaining receivable amounted to $400. What account had the smallest amount debited to it?

A) Allowance for Doubtful Installment Accounts Receivable

B) Accounts Receivable

C) Repossessed Inventory

D) Deferred Gross Profit

A) Allowance for Doubtful Installment Accounts Receivable

B) Accounts Receivable

C) Repossessed Inventory

D) Deferred Gross Profit

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

64

Exhibit 17-4 The following information is provided for Fort Myers Company:

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much gross profit did Fort Myers Company report in 2014?

A) $ 800

B) $2,000

C) $3,200

D) $4,000

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much gross profit did Fort Myers Company report in 2014?

A) $ 800

B) $2,000

C) $3,200

D) $4,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

65

The installment method should be used if

A) collectibility is extremely uncertain

B) collectibility is not reasonably assured

C) there is no reliable basis for estimating the collectibility

D) there is significant uncertainty about the profitability of a new venture or product

A) collectibility is extremely uncertain

B) collectibility is not reasonably assured

C) there is no reliable basis for estimating the collectibility

D) there is significant uncertainty about the profitability of a new venture or product

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

66

In 2014, Majors Company offered its goods to retailers on a consignment basis. The following information is provided regarding Majors Company's 2014 operations:

What is Majors' cost of goods sold for 2014?

A) $507,000

B) $512,000

C) $527,000

D) $547,000

What is Majors' cost of goods sold for 2014?

A) $507,000

B) $512,000

C) $527,000

D) $547,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

67

If Consignment-out has a debit balance, the account should be disclosed on the balance sheet as a(n)

A) expense account

B) contra-receivable account

C) inventory account

D) liability account

A) expense account

B) contra-receivable account

C) inventory account

D) liability account

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

68

Exhibit 17-4 The following information is provided for Fort Myers Company:

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much deferred gross profit is still on the books at the end of 2015?

A) $ 0

B) $2,500

C) $2,700

D) $3,000

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much deferred gross profit is still on the books at the end of 2015?

A) $ 0

B) $2,500

C) $2,700

D) $3,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

69

In real estate sales, what method of revenue recognition must be used if the sale is not consummated?

A) deferral method

B) cost recovery method

C) installment method

D) completed-contract method

A) deferral method

B) cost recovery method

C) installment method

D) completed-contract method

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following methods could not be used to recognize revenue on a real estate sale?

A) completed contract

B) deferral method

C) installment method

D) cost recovery method

A) completed contract

B) deferral method

C) installment method

D) cost recovery method

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

71

If the consignee uses a consignment-in account and has a debit balance, the

A) consignor has an obligation for that amount to the consignee

B) consignee has an obligation for that amount to the consignor

C) consignee reports the amount as a contra-asset account on the balance sheet

D) consignor reports the amount as a contra-asset account on the balance sheet

A) consignor has an obligation for that amount to the consignee

B) consignee has an obligation for that amount to the consignor

C) consignee reports the amount as a contra-asset account on the balance sheet

D) consignor reports the amount as a contra-asset account on the balance sheet

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

72

When there is a very high degree of uncertainty about the collectibility of the sales price in a sale, the preferred method of revenue recognition is the

A) cost recovery method

B) installment method

C) deferral method

D) proportional performance method

A) cost recovery method

B) installment method

C) deferral method

D) proportional performance method

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

73

A company may not use the installment method of revenue recognition for a sales transaction that

A) is an installment sale

B) is not an installment sale

C) has a legal contract

D) has a probable likelihood of collectibility

A) is an installment sale

B) is not an installment sale

C) has a legal contract

D) has a probable likelihood of collectibility

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

74

The cost recovery method

A) is generally not acceptable

B) recognizes gross profit before it has recovered all of the cost of the item sold

C) is less conservative than the installment method

D) is the preferred method under GAAP

A) is generally not acceptable

B) recognizes gross profit before it has recovered all of the cost of the item sold

C) is less conservative than the installment method

D) is the preferred method under GAAP

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

75

If material, the gross profit from installment sales should be

A) reported in the statement of stockholders' equity

B) reported in other comprehensive income on the balance sheet

C) reported in other income on the income statement

D) recognized separately from the gross profit on other sales in the income statement

A) reported in the statement of stockholders' equity

B) reported in other comprehensive income on the balance sheet

C) reported in other income on the income statement

D) recognized separately from the gross profit on other sales in the income statement

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

76

If the consignment-in account has a credit balance, it is reported on the consignee's balance sheet as a(n)

A) contra-asset account

B) revenue account

C) liability account

D) equity account

A) contra-asset account

B) revenue account

C) liability account

D) equity account

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

77

On January 1, 2014, Reids, Inc. sold a risky investment for $1,400 that had been purchased for $1,000. It was decided to use the cost recovery method of revenue recognition. Cash collections on accounts receivable related to the asset were as follows: Which of the following represent the realized gross profit that Reids should recognize for each year?

A) I

B) II

C) III

D) IV

Which of the following represent the realized gross profit that Reids should recognize for each year? A) I

B) II

C) III

D) IV

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

78

Exhibit 17-5 Kusick Co. sold a franchise at an initial franchise fee of $15,000. A down payment of $4,800 was received with the balance covered by the issuance of a $10,200, 6% note payable by the franchisee in four equal annual installments. The refund period has expired and the collectibility of the note is reasonably assured.

-Refer to Exhibit 17-5. If all material services have been substantially performed, which entry to record the franchise is correct?

A) Cash 4,800

Notes Receivable 10,200

Franchise Revenue 15,000

B) Cash 4,800

Notes Receivable 10,200

Unearned Franchise Fees 10,200

Franchise Revenue 4,800

C) Cash 4,800

Unearned Franchise Fees 4,800

D) Cash 4,800

Notes Receivable 10,200

Unearned Franchise Fees 15,000

-Refer to Exhibit 17-5. If all material services have been substantially performed, which entry to record the franchise is correct?

A) Cash 4,800

Notes Receivable 10,200

Franchise Revenue 15,000

B) Cash 4,800

Notes Receivable 10,200

Unearned Franchise Fees 10,200

Franchise Revenue 4,800

C) Cash 4,800

Unearned Franchise Fees 4,800

D) Cash 4,800

Notes Receivable 10,200

Unearned Franchise Fees 15,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

79

Exhibit 17-5 Kusick Co. sold a franchise at an initial franchise fee of $15,000. A down payment of $4,800 was received with the balance covered by the issuance of a $10,200, 6% note payable by the franchisee in four equal annual installments. The refund period has expired and the collectibility of the note is reasonably assured.

-Refer to Exhibit 17-5. If all material services have not been substantially performed, which entry to record the franchise is correct?

A) Cash 4,800

Notes Receivable 10,200

Unearned Franchise Fees 15,000

B) Cash 4,800

Notes Receivable 10,200

Unearned Franchise Fees 10,200

Franchise Revenue 4,800

C) Cash 4,800

Unearned Franchise Fees 4,800

D) Cash 4,800

Notes Receivable 10,200

Franchise Revenue 15,000

-Refer to Exhibit 17-5. If all material services have not been substantially performed, which entry to record the franchise is correct?

A) Cash 4,800

Notes Receivable 10,200

Unearned Franchise Fees 15,000

B) Cash 4,800

Notes Receivable 10,200

Unearned Franchise Fees 10,200

Franchise Revenue 4,800

C) Cash 4,800

Unearned Franchise Fees 4,800

D) Cash 4,800

Notes Receivable 10,200

Franchise Revenue 15,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

80

Exhibit 17-4 The following information is provided for Fort Myers Company:

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much gross profit did Fort Myers Company report in 2015?

A) $1,300

B) $1,500

C) $1,700

D) $2,000

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much gross profit did Fort Myers Company report in 2015?

A) $1,300

B) $1,500

C) $1,700

D) $2,000

Unlock Deck

Unlock for access to all 113 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 113 flashcards in this deck.